Amazon (AMZN) and the phrase “cheap stock” have historically not been associated with each other. For the better part of two decades, Amazon has traded at meaningful premiums as it has grown its dominant e-commerce empire.

Now, it’s building another empire in a different space: cloud computing. It has been pouring major resources into expanding its artificial intelligence computing footprint, and plans to lay out a jaw-dropping $200 billion on data center capital expenditures in 2026.

The market isn’t enthusiastic about that level of spending, which is why the stock isn’t trading at its usual premium valuation. As a result, I think now is the perfect time to load up on Amazon shares, as this weaker short-term sentiment is exactly what long-term investors need to gain an upper hand.

AWS is a major part of the Amazon investment thesis

Amazon’s commerce growth in North America has maxed out, and the result of that is that its revenue growth has become lackluster. However, its cloud computing division, Amazon Web Services (AWS), is arguably a more important part of its business anyway.

During Q1, AWS accounted for 59% of Amazon’s operating profits despite only making up 21% of revenue. That’s because the operating margin in this segment is far higher than in e-commerce.

Market cap calculated using publicly traded shares outstanding only. Does not include unlisted, private, or dual-class non-traded shares. Implied market cap may vary. Market cap calculated using publicly traded shares outstanding only. Does not include unlisted, private, or dual-class non-traded shares. Implied market cap may vary.

However, AWS is also the fastest-growing segment within Amazon, so this produces double the effect. During Q1, AWS grew at a 28% rate — the best in nearly four years. But that growth rate is expected to continue ramping up, as Amazon is spending big on new data centers.

However, AWS is also the fastest-growing segment within Amazon, so this produces double the effect. During Q1, AWS grew at a 28% rate — the best in nearly four years. But that growth rate is expected to continue ramping up, as Amazon is spending big on new data centers.

CEO Andy Jassy discussed this effect in his Q1 shareholder letter, noting that the faster AWS grows, the higher its capital expenditures must be to support that growth. AWS has already experienced record-setting growth, and it’s clear that more strong growth is on the horizon. Furthermore, AWS already has several customers lined up to use a large chunk of that $200 billion in new capacity it’s building, making it a less risky proposition.

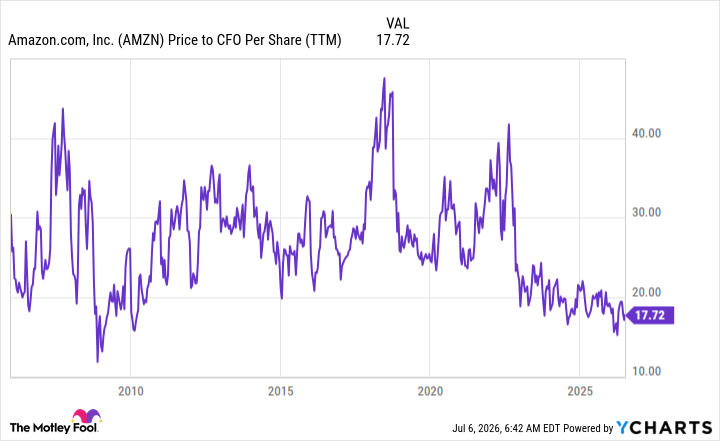

As for valuation, there are several ways to value a stock, but when looking at a company where earnings are often heavily affected by one-time costs or changes in the values of investments, using a cash flow-based metric is smart.

Because of Amazon’s high capex, gauging the stock in relation to cash from operations makes the most sense, as that metric (unlike free cash flow) ignores capital expenditures. From this standpoint, Amazon’s stock is near the cheapest level it has been over the past two decades.

With all that in mind, this looks like a perfect time to load up on Amazon shares.

With all that in mind, this looks like a perfect time to load up on Amazon shares.

— Keithen Drury

Motley Fool Stock Advisor's average stock pick is up over 350%*, beating the market by an incredible 4-1 margin. Here’s what you get if you join up with us today: Two new stock recommendations each month. A short list of Best Buys Now. Stocks we feel present the most timely buying opportunity, so you know what to focus on today. There's so much more, including a membership-fee-back guarantee. New members can join today for only $99/year.

Source: The Motley Fool