Visa (V) has underperformed broader equities over the past year. The financial services specialist has dealt with regulatory hurdles and perceived economic headwinds. Specifically, investors feared that a slowdown in consumer spending would lead to lower payment volume and revenue.

However, Visa recently soared after releasing its latest update on April 28 for the second quarter of its fiscal year 2026, which ended on March 31. Still, Visa’s stock remains down 6% over the trailing-12-month period. And at current levels, there is plenty of upside left for the company. Here are three reasons why.

1. Economic concerns may be overstated

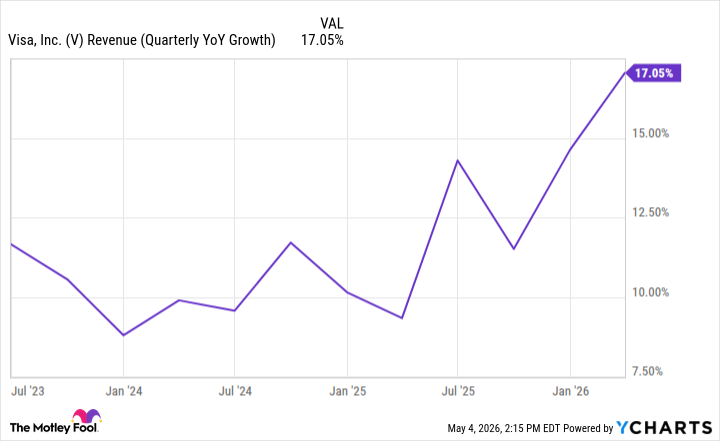

Between inflation and the possibility of a recession, some may have thought that Visa would be struggling. The company’s latest earnings helped assuage those fears. Net revenue jumped 17% year over year to $11.2 billion, while adjusted earnings per share came in at $3.31, 20% higher than the year-ago period. Visa’s results came in ahead of analyst estimates. And it’s worth noting that Visa just recorded its fastest revenue growth rate in over three years.

There may still be economic problems on the horizon, but Visa is reasonably well-positioned to navigate them. Consider inflation, which may actually benefit the company, since it makes money by charging fees on transactions it helps facilitate through its payment network (as a percentage of the transaction amount).

There may still be economic problems on the horizon, but Visa is reasonably well-positioned to navigate them. Consider inflation, which may actually benefit the company, since it makes money by charging fees on transactions it helps facilitate through its payment network (as a percentage of the transaction amount).

Higher prices mean higher fees, all else being equal. While inflation and a recession can cool spending somewhat and offset the gains it earns from higher fees, Visa should perform relatively well in the kind of economic environment we might be headed toward.

Visa’s dividend program is another reason it’s a great pick in the current environment. The company has increased its payouts every year since it initiated them in 2008. That means Visa has rewarded shareholders with higher dividends through several challenging economic periods. It is likely to do so again in the future.

2. Visa still has a massive opportunity

2. Visa still has a massive opportunity

While digital payment methods seem ubiquitous, Visa’s addressable market remains vast. Credit and debit card penetration rates may be high in some places, like the U.S., but they are lower in many other countries. Visa will also benefit from the continued growth of the e-commerce industry.

Further, the company boasts attractive opportunities beyond its core business. Consider just one of them: Visa’s issuer processing solutions, which provide card issuers (like fintech companies or banks) with the infrastructure to process transactions, along with other services such as fraud detection, analytics, and dispute management.

Visa sees a massive opportunity in this area, as management said, calling the total addressable market here “enormous.” Visa has other potential growth avenues it could ride through the next decade (and beyond). Meanwhile, the company still has a wide moat.

Not only does its brand name inspire confidence among financial institutions and individuals, but it also benefits from the network effect. As its ecosystem grows, it becomes more attractive to merchants and consumers from the outside looking in. Visa’s moat and growth opportunities could allow it to deliver outstanding returns over the long run.

3. The price is (still) right

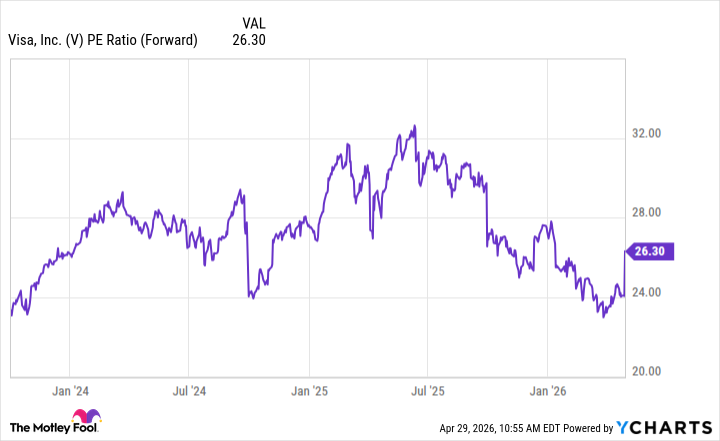

Visa has historically traded at a premium, and that isn’t surprising. Given the company’s excellent financial results, wide moat, outstanding margins, and attractive long-term opportunities, it makes perfect sense that investors are willing to pay more for the financial services leader.

However, after the poor performances it has had recently, and even after its post-earnings surge, Visa is still trading at fairly reasonable levels by its lofty standards. For context, the average forward price-to-earnings for financial stocks is currently 14.8.

Some might feel that Visa is no longer worth the premium, given potential regulatory roadblocks and other factors. But my view is that Visa’s outlook remains outstanding, and its shares are still attractive at current levels. Those who purchase them today may be glad they did so in a decade.

Some might feel that Visa is no longer worth the premium, given potential regulatory roadblocks and other factors. But my view is that Visa’s outlook remains outstanding, and its shares are still attractive at current levels. Those who purchase them today may be glad they did so in a decade.

— Prosper Junior Bakiny

Motley Fool Stock Advisor's average stock pick is up over 350%*, beating the market by an incredible 4-1 margin. Here’s what you get if you join up with us today: Two new stock recommendations each month. A short list of Best Buys Now. Stocks we feel present the most timely buying opportunity, so you know what to focus on today. There's so much more, including a membership-fee-back guarantee. New members can join today for only $99/year.

Source: The Motley Fool