Life just keeps getting more expensive.

Whatever you’re spending on a broad range of goods and services today, you will be spending much more than this 10 years from today.

This is inevitable.

How do we protect ourselves?

I think the best way to defend against this inevitability is to overcome it with another inevitability.

I’m talking about the inevitability of terrific businesses being larger, more profitable, and able to pay out more passive income to shareholders over time.

This thinking is at the heart of the dividend growth investing strategy, which is a long-term investment strategy that involves buying and holding shares in high-quality companies which pay safe, growing dividends to shareholders.

After all, if the price of goods and services is going up over time, that naturally and obviously means more revenue and profit to the companies selling all of those goods and services.

It’s awfully difficult to keep selling more stuff at higher prices without making more money in the process.

You can see the outcome of this kind of process by pulling up the Dividend Champions, Contenders, and Challengers list.

This list has data on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Many of these companies have been raising their dividends for decades.

Many of these companies have been raising their dividends for decades.

It just makes sense.

Higher prices feed through to higher profits, and higher profits feed through to larger dividends.

Why not take advantage of this chain of events by collecting more passive dividend income and fending off those higher prices on everything?

That’s been my attitude as I’ve gone about building the FIRE Fund over the last 15 years.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

Indeed, this has been enough since I put myself in a position to retire in my early 30s.

If you’re interested in putting yourself in a similar position, make sure to read my Early Retirement Blueprint.

Owning shares in great businesses benefiting from the natural rise in prices is a fantastic idea, but making sure that you pay attention to valuation at the time of investment is critical.

That’s because price only tells you what you pay, but value tells you what you get.

That’s because price only tells you what you pay, but value tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Defending yourself against the inevitable rise in prices with the inevitable nature of higher prices begetting higher profits and larger dividends is an ingenious way to approach life and money, and buying undervalued high-quality dividend growth stocks is, arguably, the very best way to implement this plan.

The whole concept of valuation, however, does seem to invite confusion.

But this confusion is unnecessary.

Lesson 11: Valuation, penned by fellow contributor Dave Van Knapp demystifies valuation by explaining how valuation works and providing an easy-to-use valuation template to take with you.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Jack Henry & Associates, Inc. (JKHY)

Jack Henry & Associates, Inc. (JKHY)

Jack Henry & Associates, Inc. (JKHY) is a financial technology company that provides a range of services to various financial financial firms.

Founded in 1976, Jack Henry is now a $13 billion (by market cap) fintech player that employs approximately 7,000 people.

The company operates across three business segments: Payments, 37% of FY 2024 revenue; Core, 31%; and Complementary, 28%. Corporate accounts for the remainder.

What Jack Henry does is, it provides various fintech services mainly for small and midsized US banks and credit unions.

Services include the likes of electronic funds transfer, payment processing, and loan processing.

Jack Henry works with nearly 2,000 banks/credit unions.

Jack Henry’s services are essential to its clients, as they’re integral to the business models.

By handling critical, nuts-and-bolts processes for banks and credit unions through proprietary technology, Jack Henry becomes a vital part of the value chain.

Furthermore, once a relationship is established and the technology is installed, this becomes a very “sticky” setup that simply makes sense to keep around.

After all, the services are both necessary for function and relatively low in cost as a percentage of an institution’s total overhead.

This explains why client retention for Jack Henry hovers around the 100% mark.

Acting as the “chef’s kiss” that seals the deal for the investment case, Jack Henry signs its customers to multiyear contracts.

A combination of essentiality, low costs, sticky services, and long-term contracts results in 90%+ recurring revenue, giving Jack Henry an incredible degree of resiliency, durability, and long-term visibility.

But wait.

There’s more.

Even while existing customers are locked in through contracts and essential services, Jack Henry is a serial acquirer which continues to expand its client base through bolt-on acquisitions,

On top of that, Jack Henry builds out its client base through new new offerings (R&D spending is roughly 15% of revenue), taking market share (organic growth has outpaced peers), and signing new clients organically (such as Triangle Credit Union, which was brought on earlier this year).

This company has so many levers to pull and ways to win, and it’s nearly impossible for the firm to do poorly over time.

To the contrary, all Jack Henry seems to do is ring up higher revenue and profit, leading to larger dividends for its shareholders.

Dividend Growth, Growth Rate, Payout Ratio and Yield

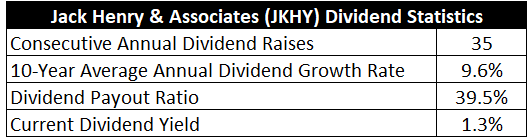

Already, Jack Henry has increased its dividend for 35 consecutive years.

That’s per the CCC list, although the company itself registers 22 consecutive years of dividend growth.

Either way, this is very impressive and just goes to show how consistent and resilient the business truly is.

No matter what the economic cycle is up to, Jack Henry just keeps steadily plowing ahead.

No matter what the economic cycle is up to, Jack Henry just keeps steadily plowing ahead.

The 10-year dividend growth rate of 9.6% is strong, although more recent dividend raises have been in a mid-single-digit range.

Jack Henry doesn’t hand out massive dividend increases; instead, it’s all about consistency and reliability here.

For those who like sleeping well at night more than explosive changes (which can sometimes be to the downside), Jack Henry has been an easy long-term hold.

The stock’s current yield of only 1.3% is not super high, and this is because the market never really allows the stock’s yield to get very high (partially due to the stock’s stability and desirability).

Still, this yield is 10 basis points higher than its own five-year average.

And with a payout ratio of only 39.5%, the well-covered dividend appears to be extremely safe.

This is obviously not suitable for income investors, but those looking for high-quality compounders to hold for the long haul (and who do not expect lots of current income) will have a very viable candidate here.

Revenue and Earnings Growth

As viable as it may be, though, many of these dividend metrics are based on what’s happened in the past.

However, investors must always have the future in mind, as today’s capital ultimately gets risked for tomorrow’s rewards.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will come in handy when estimating fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this way should give us the information we need to roughly gauge where the business could be going from here.

Jack Henry grew its revenue from $1.3 billion in FY 2015 to $2.2 billion in FY 2014.

That’s a compound annual growth rate of 6%.

Very solid top-line growth here out of Jack Henry.

Meanwhile, earnings per share increased from $2.59 to $5.23 over this period, which is a CAGR of 8.1%.

Again, this is just solid stuff out of Jack Henry.

An ~11% reduction in the outstanding share count via buybacks helps to explain the excess bottom-line growth.

What’s remarkable here is less the rate of the growth and more the secular nature of the growth.

Even the pandemic didn’t dent Jack Henry, with the firm growing its EPS straight through that period as if there were no global issue occurring.

The ceiling might not be as high as some faster-growing companies out there, but Jack Henry has a tight floor underpinning it.

It’s hard to overstate the consistency here, and that consistency has a certain value and allure to it.

Looking forward, CFRA believes that Jack Henry will compound its EPS at an annual rate of 8% over the next three years.

This is almost exactly in line with what Jack Henry put together over the last decade, speaking further on just how consistent this company is.

It’s clockwork-like reliability is almost legendary.

CFRA notes (but underplays, in my opinion) this: “We believe [Jack Henry]’s recurring-revenue-focused model offers stability for investors.”

You can say that again!

In an effort to bolster the “stickiness” of its services, as well as the company’s long-term growth prospects, Jack Henry has been rolling out a private cloud platform.

CFRA touches on the progress of cloud and the possibilities therein: “[Jack Henry] booked 11 core with financial institutions totaling $30B in assets and closed seven cloud migration deals during Mar-Q. Currently, 76% of [Jack Henry]’s clients are in the private cloud environment”.

What this private cloud does is, it reinforces the strength of Jack Henry’s ecosystem.

And that ecosystem, with is ~100% client retention, was already extremely strong to begin with.

Once a client is entrenched in that ecosystem with installed services, it’s neither easy nor necessarily beneficial to exit.

Simply put, everything that Jack Henry offers plays right into banks’ and credit unions’ digital transformation needs.

If you want sky-high growth and/or yield, look elsewhere.

If, however, you desire some of the most consistent and reliable business results out there, driven by near-100% recurring revenue, this is probably right up your alley.

Jack Henry’s impeccable management, prudent capital allocation, steady market share gains, intelligent bolt-on acquisitions, and low-cost necessity across its suite of services easily lines the firm up to meet this 8% EPS growth expectation, which also lines up the dividend for similar (or better, due to the low payout ratio) growth over the coming years.

It’s not shooting the lights out, but high-single-digit growth on top of the yield sets up the stock for a high-single-digit to low-double-digit total return over the years to come (compared to its ~12% level over the last decade).

And that would be coming in a very steady, drama-free way.

Tough to beat.

Financial Position

Moving over to the balance sheet, Jack Henry has a stellar financial position.

The long-term debt/equity ratio is less than 0.1, while the interest coverage ratio is nearly 50.

Jack Henry has a minuscule amount of long-term debt, in spite of its acquisitive nature and spending on internal development.

It just generates so much cash that it’s able to maintain a fortress balance sheet.

Profitability is outstanding.

Return on equity has averaged 23% over the last five years, while net margin has averaged 17.7%.

ROIC is usually coming in at 20%.

Jack Henry routinely generates high returns on capital.

Overall, this is one of the more impressive businesses I’ve run across.

And with economies of scale, switching costs, barriers to entry, R&D, and IP, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Competition, regulation, and litigation are omnipresent risks in every industry.

The company operates in a fairly mature US banking market that is also consolidating, limiting Jack Henry’s TAM and client base expansion potential.

The serial acquirer model introduces execution and integration risk, although Jack Henry has historically been a prudent allocator of capital.

Any kind of large-scale economic slowdown, especially a recession, could hurt Jack Henry, as banks are liable to feel the brunt of such a slowdown and may reduce IT spending as a result.

Major changes across the banking sector, although not currently on the horizon, could impact Jack Henry.

The company’s levering to tech means it must continue to innovate and stay ahead of the tech curve in order to stay relevant, retain clients, and sign new clients.

There are risks present, but I see Jack Henry’s risk profile as being relatively limited.

The easy-to-accept risk profile, along with a proven track record of extraordinary consistency, opens up room for a high valuation, but this stock’s valuation is lower than I’d expect it to be…

Valuation

The stock is trading hands for a P/E ratio of 30.6.

This is on the high end of the stocks that I tend to cover, but I believe Jack Henry’s quality and visibility warrant high multiples.

As high as this may initially seem to be, though, it’s actually quite a bit lower than the stock’s own five-year average P/E ratio of 36.

This is a stock that almost always commands high multiples, but they are currently not as high as they usually are.

The sales multiple of 5.7, which is well off of its own five-year average of 6.4, is a good example of this.

And the yield, as noted earlier, is slightly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, an 11% dividend growth rate for the next 15 years, and a long-term dividend growth rate of 8%.

All I’m doing here is, I’m extrapolating out the last decade of dividend growth into the next 10+ years.

Seeing as how Jack Henry is so tightly locked in, I don’t see anything unrealistic about this kind of growth expectation over the near term.

And I’m then thereafter dropping the growth rate down into a high-single-digit range over the long term, which is, in my view, easily achievable for Jack Henry.

It takes a special kind of business to confidently model out elevated growth over an extended time horizon, but this business (with its long-term contracts, ~100% retention rate, and 90%+ recurring revenue) is special.

The DDM analysis gives me a fair value of $180.94.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

While this stock is not optically cheap, I think this is a case of getting what you pay for.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates JKHY as a 3-star stock, with a fair value estimate of $191.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates JKHY as a 3-star “HOLD”, with a 12-month target price of $185.00.

I came out the lowest this time around, but we’re all pretty close to one another. Averaging the three numbers out gives us a final valuation of $185.65, which would indicate the stock is possibly 3% undervalued.

Bottom line: Jack Henry & Associates, Inc. (JKHY) is a high-quality fintech firm with near-100% client retention and 90%+ recurring revenue. It generates high returns on capital, operates with almost no debt, and employs the serial acquirer model with precision. Fundamentally, it’s superb. With a market-like yield, a low payout ratio, double-digit dividend growth, 30+ consecutive years of dividend raises, and the potential that shares are 3% undervalued, this is a top-shelf dividend growth stock worth paying up for.

Bottom line: Jack Henry & Associates, Inc. (JKHY) is a high-quality fintech firm with near-100% client retention and 90%+ recurring revenue. It generates high returns on capital, operates with almost no debt, and employs the serial acquirer model with precision. Fundamentally, it’s superb. With a market-like yield, a low payout ratio, double-digit dividend growth, 30+ consecutive years of dividend raises, and the potential that shares are 3% undervalued, this is a top-shelf dividend growth stock worth paying up for.

-Jason Fieber

Note from D&I: How safe is JKHY’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 99. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, JKHY’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Dividends & Income

Disclosure: I’m long JKHY.