Just in case you missed it, Wednesday, Feb. 14, was arguably the most important day of the first quarter for investors. It marked the deadline for institutional investors with at least $100 million in assets under management to file Form 13F with the Securities and Exchange Commission.

In simple terms, a 13F allows investors to see what Wall Street’s smartest and most-successful money managers purchased and sold in the most recent quarter. In this instance, I’m talking about buying and selling activity that would have occurred during the December-ended quarter.

While there are dozens of top-tier asset managers, none draw interest on Wall Street quite like Berkshire Hathaway (BRK.A) (BRK.B) CEO Warren Buffett.

Warren Buffett and his team remain net-sellers of equities

Since the Oracle of Omaha became CEO in the mid-1960s, Berkshire Hathaway’s Class A shares (BRK.A) have returned an aggregate of 4,848,215%, as of the closing bell on Feb. 14, and practically doubled up the annualized total return, including dividends, of the S&P 500. Suffice it to say, professional and everyday investors eagerly await the lifting of Berkshire Hathaway’s proverbial hood on a quarterly basis.

What Berkshire Hathaway’s recently released 13F revealed was, unfortunately, more of the same for Warren Buffett and his top investing aides, Todd Combs and Ted Weschler. Namely, Berkshire’s dynamic trio continues to sell more stock than they’re purchasing.

Whereas Berkshire’s 13F suggests equity purchases were likely in the neighborhood of $2.2 billion to $2.3 billion during the fourth quarter, aggregate selling activity looks to have doubled this amount. All told, Buffett and his team added to two existing stakes while reducing Berkshire’s position in three holdings and completely selling out of four others.

In the 12-month period between Oct. 1, 2022 and Sept. 30, 2023, the Oracle of Omaha and his aides were net-sellers of $38.3 billion in equities. Though Buffett would never bet against America, he is a stickler for value — and Wall Street is historically pricey at the moment.

Based on data back-tested to 1870, the S&P 500’s Shiller price-to-earnings (P/E) ratio (also known as the cyclically adjusted price-to-earnings ratio, or CAPE ratio) has surpassed 30 only six times. The Shiller P/E ratio examines inflation-adjusted earnings over the previous 10 years.

The five previous times the S&P 500’s Shiller P/E ratio lifted above 30 during a bull market rally eventually resulted in the broad-based index shedding at least 20% of its value. Warren Buffett is more than willing to wait for wonderful companies to come down to what he deems to be a fair price.

However, the rare value stock can still be uncovered.

Say hello to the value stock Buffett can’t stop piling into

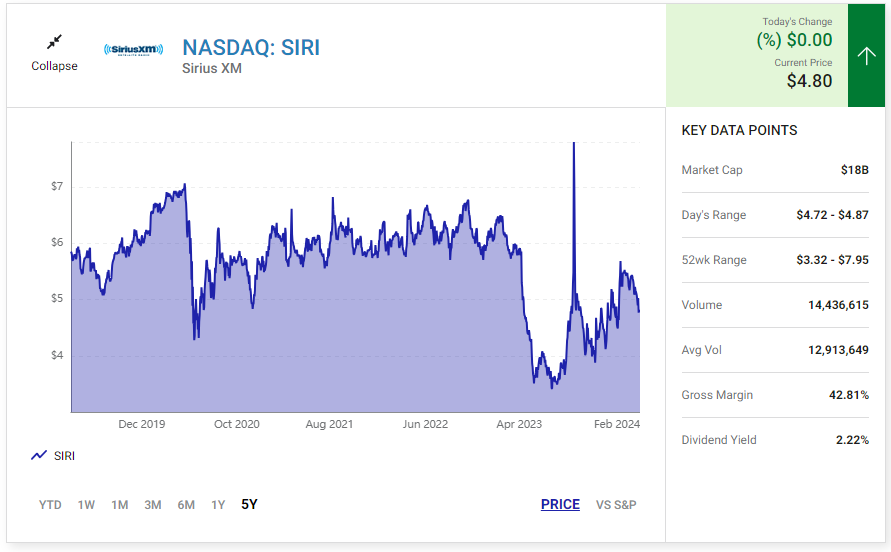

Although the Oracle of Omaha and his team added more than 15.8 million shares to their existing position in energy giant Chevron during the fourth quarter (Q4), it’s historically cheap value stock Sirius XM Holdings (SIRI) that stole the show. After initiating a nearly 9.7-million-share stake in Sirius XM during the third quarter, Buffett oversaw a more-than-quadrupling in this position to 40.24 million shares in Q4.

In addition to loving wonderful companies at a fair price, Warren Buffett tends to gravitate to businesses with untouchable moats and/or sustained competitive advantages. That’s precisely what satellite-radio operator Sirius XM Holdings provides.

To begin with, it’s the only licensed satellite-radio operator. While it does still have competition for listeners with terrestrial and online radio, being the lone approved satellite-radio provider affords the company exceptionally strong pricing power. The ability to increase subscription prices has helped it easily outpace the inflationary curve.

Furthermore, Sirius XM Holdings generates revenue quite differently than traditional radio companies. While terrestrial and online providers are heavily reliant on advertising to keep the lights on, Sirius XM generated less than 20% of its net sales in 2023 from advertising.

Furthermore, Sirius XM Holdings generates revenue quite differently than traditional radio companies. While terrestrial and online providers are heavily reliant on advertising to keep the lights on, Sirius XM generated less than 20% of its net sales in 2023 from advertising.

Close to 77% of the company’s revenue comes from aforementioned subscriptions to its service. Subscription revenue tends to be far more predictable than ad revenue, and it’s more likely to generate juicier margins. Additionally, a subscription-driven model should hold up better during economic downturns, relative to ad-driven platforms.

The Oracle of Omaha is also a big fan of cyclical businesses. Berkshire Hathaway’s portfolio is packed with dozens of investments and owned businesses that ebb and flow with the health of the U.S. economy. Buffett and his team understand that recessions tend to be short-lived, while periods of growth can endure for multiple years, if not a decade.

Although Sirius XM stock is susceptible to weakness during recessions — e.g., fewer vehicles sold means less chance of converting promotional subscriptions into self-pay accounts — it’s going to disproportionately benefit from long-winded expansions. In short, investors who have time on their side are well-positioned to succeed with a stock like Sirius XM.

Sirius XM offers a shareholder-friendly capital-return program, as well. It’s repurchased and retired $921 million worth of its common stock over the previous two years — fewer shares outstanding should lift earnings per share — and its 2.2% yield surpasses the yield of the S&P 500.

Sirius XM offers a shareholder-friendly capital-return program, as well. It’s repurchased and retired $921 million worth of its common stock over the previous two years — fewer shares outstanding should lift earnings per share — and its 2.2% yield surpasses the yield of the S&P 500.

Lastly, Sirius XM provides the value that Warren Buffett seeks. As of the closing bell on Feb. 14, shares of Sirius XM could be purchased for a multiple 14.6 times Wall Street’s consensus earnings per share in 2025. Not only is this markedly lower than the forward P/E ratio for the S&P 500, but it’s a 31% discount to the company’s average forward P/E ratio over the trailing-five-year period.

No matter how pricey the stock market is, there’s a good chance Warren Buffett can find a plain-as-day value hiding in plain sight.

— Sean Williams

Motley Fool Stock Advisor's average stock pick is up over 350%*, beating the market by an incredible 4-1 margin. Here’s what you get if you join up with us today: Two new stock recommendations each month. A short list of Best Buys Now. Stocks we feel present the most timely buying opportunity, so you know what to focus on today. There's so much more, including a membership-fee-back guarantee. New members can join today for only $99/year.

Source: The Motley Fool