Money.

Easy to spend.

Hard to acquire.

This is why I’m such a fan of investing.

It allows money to make more money.

But it’s even better than that.

Through compounding, money can make ever-more money… ad infinitum.

And this is something that can approached quite simply through the dividend growth investing strategy.

This is a strategy that advocates buying and holding shares in high-quality businesses that pay safe, growing dividends to shareholders.

You can find hundreds of examples by perusing the Dividend Champions, Contenders, and Challengers list.

That list has compiled data on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Generally speaking, only great businesses can consistently increase cash payouts to shareholders.

Generally speaking, only great businesses can consistently increase cash payouts to shareholders.

Why?

Well, it takes a great business to produce the consistently growing profit necessary to afford consistently growing dividends.

What this means is, this strategy almost automatically funnels you right into great businesses that are demonstrably skilled at compounding money – i.e., money making more money.

This is why I’ve been personally using the strategy for more than a decade now, allowing it to guide me as I’ve gone about building the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

Indeed, dividend income has been able to cover my bills since I quit my job and retired in my early 30s.

My Early Retirement Blueprint explains how I was able to accomplish that feat.

While dividend growth investing can funnel you well, valuation at the time of investment is always critical.

While price is what you pay, value is what you end up getting.

While price is what you pay, value is what you end up getting.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying undervalued high-quality dividend growth stocks can allow you to tap into the powerful process of compounding where money makes more money for you.

Of course, that does require one to have a have a basic understanding of how to go about valuing a business.

No worries.

My colleague Dave Van Knapp put together Lesson 11: Valuation in order to help build that understanding.

Part of an overarching series of “lessons” designed to teach the dividend growth investing strategy, it lays out a simple-to-follow valuation technique that can be applied to almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

NextEra Energy Inc. (NEE)

NextEra Energy Inc. (NEE)

NextEra Energy Inc. (NEE) is an American energy company.

Founded in 1925, NextEra Energy is now a $116 billion (by market cap) power utility giant that employs more than 15,000 people.

By market cap, this is the largest utility holding company in the US.

NextEra Energy reports results across three segments: Florida Power & Light, 65% of FY 2023 revenue; NextEra Energy Resources, 34%; and Corporate and Other, 1%.

FPL operates the largest electric utility business in Florida, providing electricity to over 12 million people across the state of Florida.

FPL’s energy mix is: 71% natural gas, 21% nuclear, 5% solar, and 3% other.

Based on electricity sales, FPL is the largest utility in the US.

NEER is the world’s largest generator of renewable energy from the wind and sun, and it’s also a world leader in battery storage.

This is a very unique business that offers something to like for both traditional utility fans and investors who want to be exposed to the future of renewable energy production.

NextEra Energy is successfully operating an orthodox electric utility business and a renewable energy business at unmatched scale.

In my view, this is the best of both the old and the new.

NextEra Energy is aptly named, as it’s preparing for the next era of energy via its investments in and usage of solar and wind power generation, along with battery storage.

The world is slowly moving toward newer forms of energy that are, rightly or wrongly, perceived to be cleaner and more sustainable for society.

What this means is, utility companies that can adapt to this change will be the best positioned to not only survive but thrive.

At the same time, the company is firmly grounded in reality, using proven resources such as natural gas to generate electricity for customers who count on having access to reliable power 24/7.

The all-of-the-above approach has proven itself to be a winning strategy for NextEra Energy and its shareholders.

After all, the whole thesis of investing in a power utility company revolves around the fact that we cannot live in a modern-day society without reliable access to electricity.

Since electricity is a non-negotiable need, a power utility is naturally blessed with captive customers and highly recurring/visible revenue.

On top of all of this, NextEra Energy’s FPL unit is favorably situated in Florida.

Florida has, for years, been one of the fastest-growing states in the US, and it’s also a jurisdiction that has historically had a constructive regulatory framework.

That puts FPL in a very advantageous spot for continued growth through both customer acquisitions and rate increases.

NextEra Energy is a rare case of a dependable utility with growth characteristics – a best-of-both-worlds setup.

This passage from Morningstar homes in on this: “NextEra Energy’s high-quality regulated utility in Florida and fast-growing renewable energy business give investors the best of both worlds: a secure dividend and industry-leading renewable energy growth potential.”

This unparalleled combination has led to, and should continue to lead to, consistent revenue, profit, and dividend growth.

Dividend Growth, Growth Rate, Payout Ratio and Yield

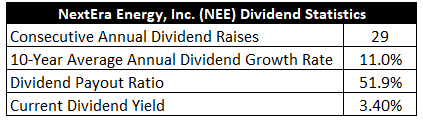

To that point, NextEra Energy has increased its dividend for 29 consecutive years.

This makes NextEra Energy a vaunted Dividend Aristocrat – one of only three power utility companies that have achieved such status.

You get rare consistency here.

You get rare consistency here.

And you also get rare growth.

Indeed, the 10-year dividend growth rate is 11%.

A double-digit dividend growth rate is nearly unheard of for a utility.

Thanks to the growth engines I already outlined, NextEra Energy has been able to hand out generous dividend raises for years.

And the crazy thing is, you don’t even need to sacrifice much yield here.

The stock yields 3.4%.

Sure, that’s not as high as some other power utilities out there (almost all of which are growing much slower than NextEra Energy).

But it does easily beat the broader market.

It’s also 130 basis points higher than its own five-year average.

And with a payout ratio of 51.9%, which is nearly perfectly balanced, the dividend is very healthy and poised for more growth ahead.

I see nothing to dislike here.

You get yield, growth, safety, and consistency.

It’s a very compelling package.

Revenue and Earnings Growth

As compelling as these metrics may be, though, many of them are looking into the past.

However, investors must always be looking into the future, as today’s capital gets risked for the rewards of tomorrow.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will be highly useful when the time comes later to estimate intrinsic value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this manner should give us the information we need to make an educated call on where the business might be going from here.

NextEra Energy moved its revenue from $17 billion in FY 2014 to $28.1 billion in FY 2023.

That’s a compound annual growth rate of 5.7%.

I’m looking for mid-single-digit top-line growth from a fairly mature business like this.

NextEra Energy delivered.

Meanwhile, earnings per share grew from $1.40 to $3.60 over this 10-year period, which is a CAGR of 11.1%.

So we can see how EPS growth is almost precisely in line with dividend growth over the last decade, showing extremely tight control from management.

Looking forward, CFRA is projecting an 8% CAGR for NextEra Energy’s EPS over the next three years.

This may turn out to be a touch high, but it’s really not that far off from what NextEra Energy’s management is guiding for over the near term.

Here’s an excerpt from the company’s most recent earnings release: “For 2025 and 2026, NextEra Energy expects to grow 6% to 8%, off the 2024 adjusted earnings per share range. This translates to a range of $3.45 to $3.70 for 2025 and $3.63 to $4.00 for 2026. NextEra Energy also continues to expect to grow its dividends per share at a roughly 10% rate per year through at least 2024, off a 2022 base.”

Seeing as how NextEra Energy has been consistently hitting its marks for years now, I see no reason to start doubting management now.

It’s been a well-run operation for as long as I’ve been investing (going back more than 10 years).

In my view, NextEra Energy is set up very nicely for both the near term and the long term.

Worth pointing out is this passage from CFRA: “Longer term, we have a positive outlook on the growing Florida economy and low customer rate uncertainty through 2026. We also note tailwinds for NEER’s renewables backlog and FPL’s Real Zero 2045 emissions target from IRA clean energy tax credits.”

It’s this one-two punch that is serving NextEra Energy uniquely well.

This is, arguably, the best power utility business in the US.

If we take management’s word to heart, the next few years should see ~10% dividend growth.

And you’re getting a near-3.5% yield to start with.

Very challenging to find a better combination of growth and yield than that.

Financial Position

Moving over to the balance sheet, NextEra Energy has a good, but not excellent, financial position.

The long-term debt/equity ratio is 1.1, while the interest coverage ratio is slightly over 3.

These are pretty common numbers for a utility, and I’d say the balance sheet is the one area in which NextEra Energy looks like just about every other power utility out there.

That said, it’s unsurprising to see this.

After all, building out energy infrastructure requires a lot of spending – funded largely by debt – and NextEra Energy is nearly guaranteed by regulators to earn a return on its investments (through higher power rates).

Profitability is robust.

Return on equity has averaged 11% over the last five years, while net margin has averaged 20.6%.

NextEra Energy’s returns on capital aren’t super high in absolute terms, but it does beat most of the other energy utilities I follow.

Fundamentally speaking, NextEra Energy is probably the best power utility business in the US.

And the company does benefit from durable competitive advantages, including economies of scale, a geographic monopoly, a unique structure, a favorable geographic footprint, and a constructive regulatory structure that just about guarantees some level of profit.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

Regulation is a double-edged sword.

Regulators allow for utilities to make a reasonable profit, where profit scales with costs, putting a profit floor in place.

On the flip side, because electricity is necessary and there’s often only one power provider in any one geographic area, regulators install a profit ceiling by limiting the rates a utility can charge.

This is a rare industry in which competition at a local level doesn’t exist, as NextEra Energy runs local monopolies across its territory.

However, customers could become future competitors by generating power at the site of consumption (via solar).

NextEra Energy’s FPL is captive to the regulatory structure and population growth of Florida, but Florida is currently one of the best possible states to run a regulated utility.

Illustrating this point, Morningstar states: “The company’s below-average retail rates have garnered comparatively favorable treatment in the already-constructive Florida regulatory jurisdiction. [FPL] enjoys above-average returns on equity, forward-looking rate adjustments, and automatic general base-rate adjustments for investments upon completion. We expect future returns to be lower but still be above most other utilities.”

Exposure to nuclear is present.

Natural disaster risk is also present, especially since Florida is vulnerable to hurricanes.

The economics surrounding renewables are still questionable, and it remains to be seen how economically successful NEER will ultimately be.

Overall, most of these risks are pretty ordinary for a power utility business.

And the valuation also seems to be pretty ordinary, despite the fact that NextEra Energy is, in many ways, extraordinary…

Valuation

The P/E ratio of 15.6 is roughly in line with many of the US power utilities out there.

But I’d argue that NextEra Energy should get a premium.

Indeed, it typically does get a premium.

Its own five-year average P/E ratio is 40.5, although that’s clouded by volatile GAAP earnings.

If we look at the cash flow multiple of 10.1, that is seven turns lower than its own five-year average of 17.1.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7.5%.

That growth rate is on the higher end of what I allow for when working with a utility, but NextEra Energy’s eminence qualifies it.

This is quite a bit lower than where the near-term dividend growth expectation is at, but I wouldn’t anticipate that 10% dividend growth rate to persist indefinitely.

It will almost certainly slow in coming years, and that explains the short-term nature of that high guidance.

I’m not predicting any kind of growth collapse.

Rather, a gradual slowdown, culminating into a few percentage points per year does seem likely from my vantage point.

But with the recent compression in multiples, which drove the yield higher, that slowing is more than priced in.

The DDM analysis gives me a fair value of $80.41.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

Despite what I think was a cautious take on valuation, the stock still looks very cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates NEE as a 4-star stock, with a fair value estimate of $74.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates NEE as a 4-star “BUY”, with a 12-month target price of $69.00.

I came out on the high end this time around, which surprises me. Averaging the three numbers out gives us a final valuation of $74.47, which would indicate the stock is possibly 25% undervalued.

Bottom line: NextEra Energy Inc. (NEE) is, arguably, the best power utility business in the US. It has a lock on one of the best geographic areas in the US, and its renewables side of the house is the largest in the world. With a market-beating yield, a moderate payout ratio, a double-digit long-term dividend growth rate, nearly 30 consecutive years of dividend increases, and the potential that shares are 25% undervalued, this Dividend Aristocrat could be one of the best long-term investment candidates in the market for dividend growth investors.

Bottom line: NextEra Energy Inc. (NEE) is, arguably, the best power utility business in the US. It has a lock on one of the best geographic areas in the US, and its renewables side of the house is the largest in the world. With a market-beating yield, a moderate payout ratio, a double-digit long-term dividend growth rate, nearly 30 consecutive years of dividend increases, and the potential that shares are 25% undervalued, this Dividend Aristocrat could be one of the best long-term investment candidates in the market for dividend growth investors.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is NEE’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 90. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, NEE’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I’m long NEE.