Some people like to overcomplicate investing.

When you boil it down, it’s actually pretty simple.

You want to invest in great businesses.

You should not pay too much for the shares.

And you should plan to hold for the long term.

There are nuances, no doubt about it, but those three steps comprise a very large chunk of what it means to invest successfully.

But how do we find great businesses to invest in?

Well, the Dividend Champions, Contenders, and Challengers list would be a great place to look.

This list contains invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Every stock on the list qualifies for the dividend growth investing strategy.

That’s a strategy whereby one buys and holds shares in high-quality businesses that pay reliable, rising dividends to shareholders.

This strategy almost automatically funnels one right into great businesses, by virtue of rising dividends funded by rising profits.

So you get great businesses, and you get steadily rising passive income.

So you get great businesses, and you get steadily rising passive income.

Not bad!

I’ve been using this strategy for more than a decade now.

It’s guided me as I’ve gone about building the FIRE Fund.

That’s my real-life, real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

Indeed, I’ve been able to live off of dividend income for a number of years now, even using this income to supplant my paycheck when I quit my job and retired in my early 30s.

My Early Retirement Blueprint shares how I was able to do such a thing.

Of course, a pillar of my success has been investing in great businesses.

But not paying too much for shares has also been key.

But not paying too much for shares has also been key.

And that leads me to right to the concept of valuation.

Whereas price is what you pay, it’s value that you ultimately get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

The idea of buying undervalued high-quality dividend growth stocks is a simple one, but there’s no need to overcomplicate investing.

Now, that idea does require one to have at least a basic understanding of valuation.

No worries.

My colleague Dave Van Knapp put together Lesson 11: Valuation in order to help anyone out there who needs it.

Part and parcel of a comprehensive series of “lessons” designed to teach the A-Z of DGI, it lays out a valuation system that can be easily applied toward just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Hershey Co. (HSY)

Hershey Co. (HSY)

Hershey Co. (HSY) is an American multinational confectionery and snack food company.

Founded in 1894, Hershey is now a $37 billion (by market cap) confectionary leader that employs almost 19,000 people.

The company reports results across three segments: North America Confectionery, 82% of FY 2022 sales; North America Salty Snacks, 10%; and International, 8%.

Hershey has spent the last 100+ years constructing a confectionary empire.

The company now controls approximately 100 different brands, including the likes of Kit Kat and Reese’s.

These beloved candies have allowed Hershey to build a commanding lead in the US confectionary market.

These beloved candies have allowed Hershey to build a commanding lead in the US confectionary market.

It’s estimated by IRI that Hershey has a 45% share of this market, which is incredible.

And since chocolate is a low-cost, high-value occasional treat for many people, paying up for the consistent, familiar, and distinctive flavor of Hershey’s candies makes a lot of sense for many consumers.

This makes it difficult for private label products to compete, so the dominant players already in place are entrenched with very strong competitive positions.

The brand power here is immense.

But that’s not all there is to this story.

Management has recently broadened the business by acquiring a range of salty snack products to complement the core confectionary business, giving Hershey a sweet-and-salty one-two punch.

Hershey acquired Amplify Snack Brands, which makes Skinny Pop ready-to-eat popcorn, for $1.6 billion in 2018.

The 2021 acquisition of Dot’s Pretzels for $1.2 billion further bolstered Hershey’s salty snack offerings.

The last decade has been very kind to this business.

If past is prologue, shareholders of Hershey have a lot to look forward to.

That should include plenty of growth across revenue, profit, and the dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

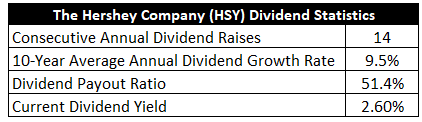

To date, Hershey has increased its dividend for 14 consecutive years.

The 10-year dividend growth rate is 9.5%.

While that’s great in and of itself, Hershey has been growing its dividend at an even higher rate in recent years.

The most recent dividend raise, for example, was 15.1%.

Very nice acceleration in dividend growth.

Very nice acceleration in dividend growth.

Along with this high rate of dividend growth, the stock offers a yield of 2.6%.

This is a fantastic combination of yield and growth.

Assuming a static valuation, the sum of yield and growth should roughly equal one’s annualized total return.

If you can get a near-3% yield and growth in the 10% range, that’s setting you up for low-double-digit annualized total return.

Nothing wrong with that at all.

Also, this 2.6% yield is 60 basis points higher than its own five-year average.

A payout ratio of 51.4%, which is almost perfectly balanced, shows us a healthy dividend with room to head higher over the coming years.

Lovely dividend metrics here.

Revenue and Earnings Growth

As lovely as they might be, though, many of these numbers are looking backward.

However, investors must always be looking forward and realizing that today’s capital is being risked for tomorrow’s rewards.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be highly useful when the time comes later to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast like this should give us the information we need to roughly gauge what the future growth path of the business could look like.

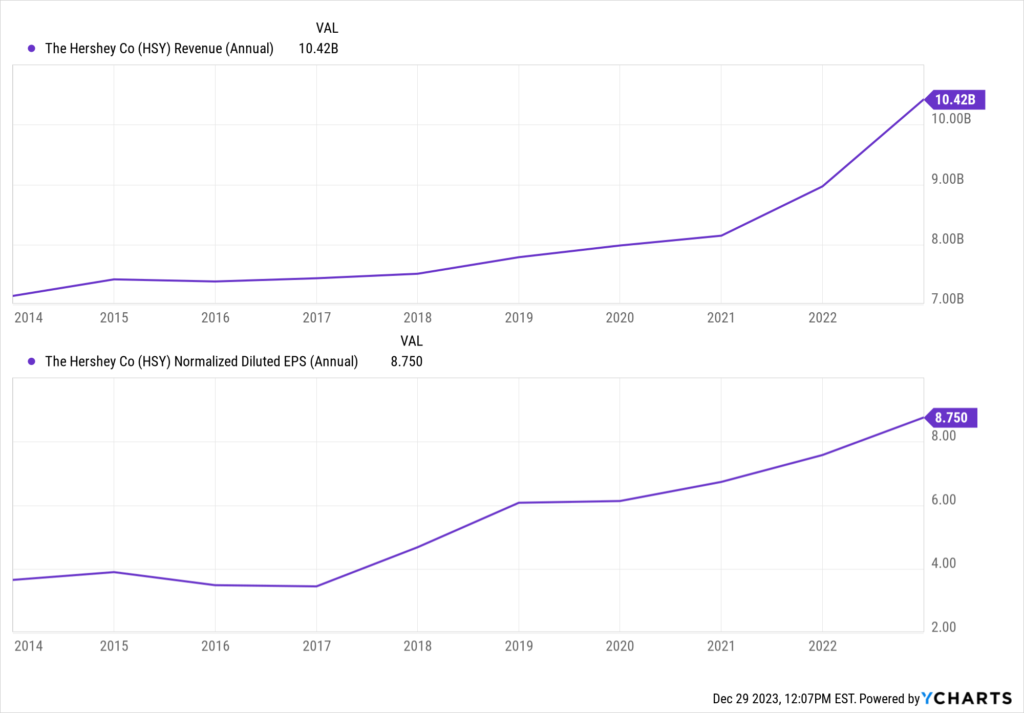

Hershey increased its revenue from $7.1 billion in FY 2013 to $10.4 billion in FY 2022.

That’s a compound annual growth rate of 4.3%.

I usually look for a mid-single-digit top-line growth rate from a mature business, and Hershey pretty much delivered.

Meantime, earnings per share grew from $3.61 to $7.96 over this period, which is a CAGR of 9.2%.

Excellent.

Excellent.

Always nice to see a high-single-digit bottom-line growth rate from a large, established business like this.

It just goes to show that there are multiple levers a business like this can pull in order to drive excess bottom-line growth.

One such lever is buybacks, and Hershey did reduce its outstanding share count by approximately 9% over the last decade.

It’s also nice to see how well bottom-line and dividend growth match up – almost the same exact growth rates over the last 10 years.

Management has clearly been running a tight ship.

Looking forward, CFRA believes that Hershey will compound its EPS at an annual rate of 11% over the next three years.

I like this call.

Seems realistic to me.

It gels with Hershey’s recent gathering of speed across the business, which shows up in the aforementioned dividend growth acceleration.

For some perspective on this, Hershey itself is guiding for 13% to 15% YOY growth in EPS for FY 2023.

Moreover, recent quarters have consistently shown double-digit YOY EPS growth for the business.

There’s nothing to indicate that Hershey will do anything but grow its EPS at a low-double-digit rate for the foreseeable future.

It’s just too good of a business to do otherwise.

In my view, only some kind of major, unforeseen macro event could throw things off.

If we take CFRA’s forecast as the base case, this sets Hershey up to grow its dividend at a similar level.

The balanced payout ratio would easily allow for this.

That translates to a good possibility of low-double-digit dividend growth over at least the next few years, and you’re getting a near-3% yield to kick things off with.

That is highly, highly appealing to me.

Financial Position

Moving over to the balance sheet, Hershey has a rock-solid financial position.

The long-term debt/equity ratio is 1, while the interest coverage ratio is approximately 15.

I’ll also note that Hershey’s long-term debt load has been reduced by nearly 20% after peaking in FY 2020, and that’s while both revenue and net income are both up healthily since then.

I like the deleveraging story playing out, which gives Hershey future firepower for more bolt-on acquisitions.

Profitability is outstanding.

Return on equity has averaged 68.5% over the last five years, while net margin has averaged 15.7%.

Hershey is producing very high returns on capital, and the margins are fat.

This is a world-class operation.

And the company does benefit from durable competitive advantages that include economies of scale, brand/pricing power, and a dominant share of its core market.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

The rise of new weight-loss drugs could reduce demand for Hershey’s indulgent products.

Input costs can be volatile.

Hershey’s long-term growth profile is largely tied to the US confectionary market, which is mature.

Hershey’s small international segment does expose the company to currency exchange rates and different markets with different rules and tastes.

The company has long been reliant on sales channels such as gas stations and convenience stores, which may see unfavorable changes as more commerce moves online.

Overall, I don’t see the business model as having an elevated amount of risk.

But the quality is elevated, and the valuation looks appealing after the stock’s 20%+ drop in price over the last year…

Stock Price Valuation

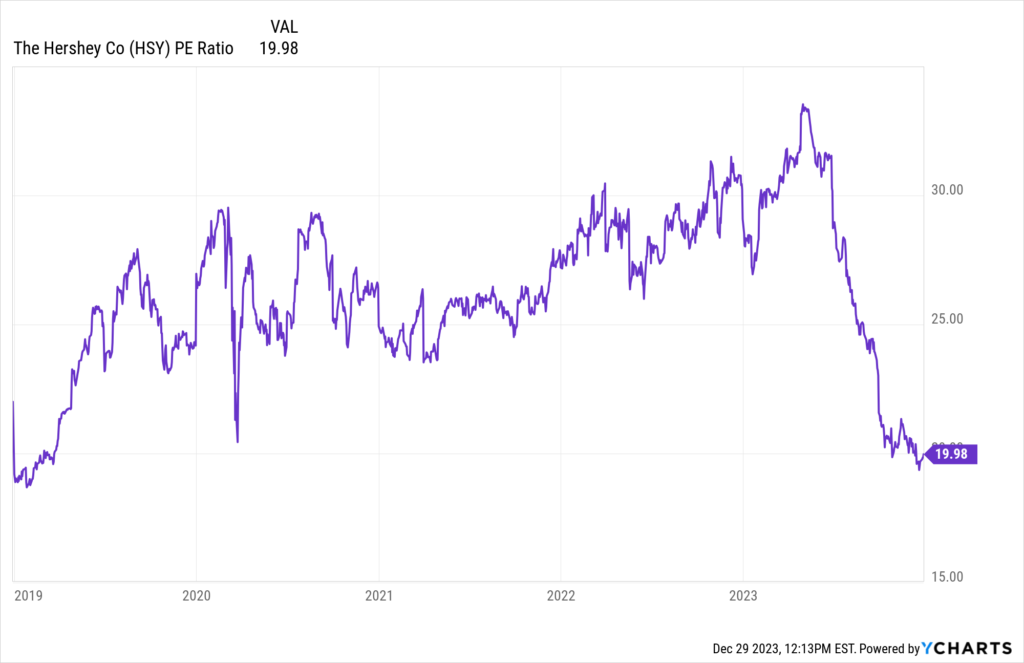

The stock is trading hands for a P/E ratio of 19.8.

I think that’s downright low for a business of this stature.

For the sake of comparison, the stock’s own five-year average P/E ratio is 26.4.

Even that average earnings multiple isn’t terribly high, in my view, but we are well below that now.

The current sales multiple of 3.4 is also quite a bit lower than its own five-year average of 4.2.

The current sales multiple of 3.4 is also quite a bit lower than its own five-year average of 4.2.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 8%.

That dividend growth rate is as high as I’ll go with the model.

However, if there’s any business that deserves the benefit of the doubt, it’s this one.

This is a world-class business that dominates its market with well-known, beloved brands.

Hershey has grown its EPS and dividend at rates in excess of what I’m modeling in, and both growth rates have recently accelerated.

I just don’t see anything to indicate that Hershey can’t grow its dividend at a high-single-digit level over the foreseeable future.

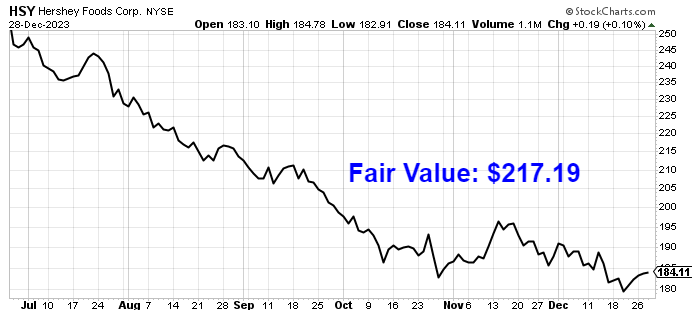

The DDM analysis gives me a fair value of $257.58.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

From my point of view, this stock is too cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates HSY as a 4-star stock, with a fair value estimate of $197.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates HSY as a 3-star “HOLD”, with a 12-month target price of $197.00.

I came out high, which does surprise me. Averaging the three numbers out gives us a final valuation of $217.19, which would indicate the stock is possibly 15% undervalued.

Bottom line: Hershey Co. (HSY) is a world-class business that dominates its market, producing high returns on capital and fat margins in the process. Recent progress suggests it’s getting broader and better, giving shareholders much to be excited about. With a market-beating yield, high-single-digit dividend growth, a balanced payout ratio, nearly 15 consecutive years of dividend increases, and the potential that shares are 15% undervalued, long-term dividend growth investors appear to have a great long-term investment opportunity on their hands right now.

Bottom line: Hershey Co. (HSY) is a world-class business that dominates its market, producing high returns on capital and fat margins in the process. Recent progress suggests it’s getting broader and better, giving shareholders much to be excited about. With a market-beating yield, high-single-digit dividend growth, a balanced payout ratio, nearly 15 consecutive years of dividend increases, and the potential that shares are 15% undervalued, long-term dividend growth investors appear to have a great long-term investment opportunity on their hands right now.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is HSY’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 93. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, HSY’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Disclosure: I’m long HSY.

Source: Dividends & Income