Uber Technologies’ (UBER) platform provides access to transportation and food delivery services. In addition, the company’s network also connects shippers and carriers in the freight industry, offering transportation management and other additional logistics services.

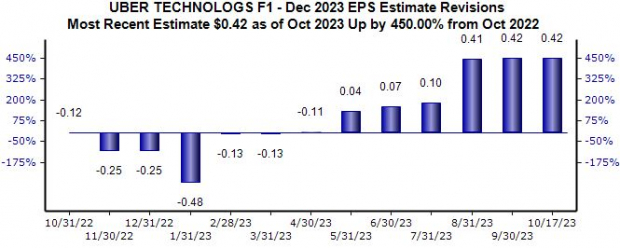

Analysts have taken a favorable stance on the company’s earnings outlook, helping land the stock into the highly-coveted Zacks Rank #1 (Strong Buy). The revisions trend has been particularly notable for its current fiscal year, with the Zacks Consensus EPS Estimate of $0.42 up 450% since October of last year.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Uber resides in the Zacks Internet – Services industry, which is currently ranked in the top 38% of all Zacks industries. Aside from the favorable earnings outlook and industry standing, let’s take a closer look at a few other characteristics of the company.

Uber Technologies

Uber shares could be a target among growth-focused investors, further reflected by its Style Score of “A” for Growth. The company’s earnings are forecasted to see 110% growth on 18% higher revenues in its current year, with expectations for FY24 suggesting 160% earnings growth paired with an 18% sales bump.

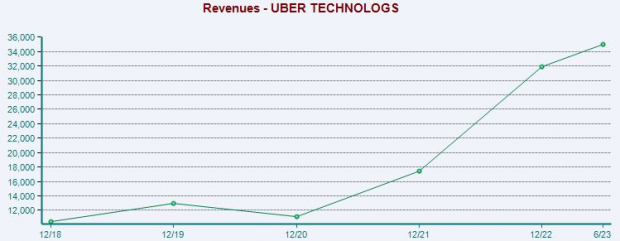

The company’s revenue growth has been robust, as illustrated below. FY22 revenue of $31.9 billion reflects a +200% increase from FY18 sales of $10.4 billion. Please note that the current value for 2023 is on a trailing twelve-month basis.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

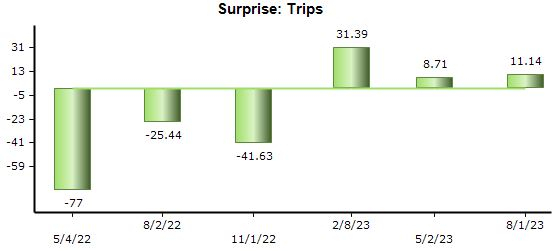

Uber’s latest quarterly results were aided by continued business momentum, with Trips growing 22% year-over-year to 2.3 billion and Gross Bookings improving 16% from the year-ago period. Impressively, the company posted record quarterly free cash flow of $1.1 billion.

As shown below, the company has consistently exceeded the Zacks Consensus Estimate for quarterly Trips as of late. Regarding the upcoming release expected on November 7th, we currently expect Uber to post Trips of 2.4 billion, reflecting a change of +21% from the same period last year. As reflected by these expectations, business momentum looks set to continue.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

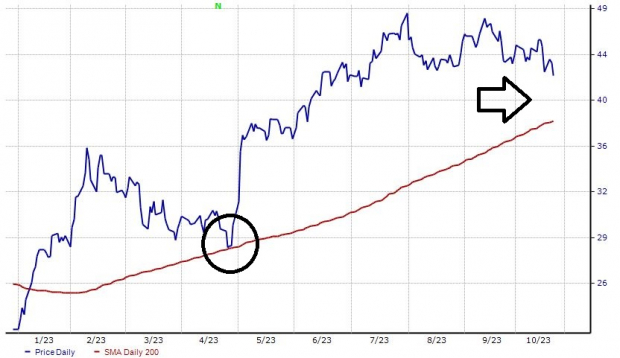

It’s also worth noting that shares have respected their 200-day daily moving average, finding buyers at the level in late April. Given the recent volatility in the market and sideways action of shares over the last several months, this level could potentially be re-tested in the coming periods.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

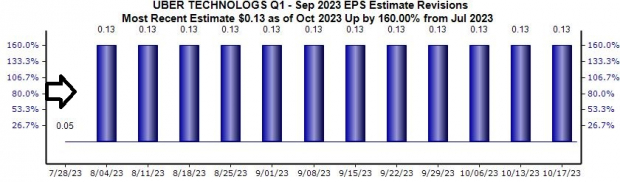

To touch further on the release expected on November 7th, the Zacks Consensus EPS Estimate of $0.13 reflects a change of +120% from the year-ago period. Analysts raised their expectations notably for the print following Uber’s latest release in early August and have remained unchanged since.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Bottom Line

Investors can implement a stellar strategy to find expected winners by taking advantage of the Zacks Rank – one of the most powerful market tools that provides a massive edge.

The top 5% of all stocks receive the highly coveted Zacks Rank #1 (Strong Buy). These stocks should outperform the market more than any other rank.

Uber Technologies (UBER) would be an excellent stock for investors to consider, as displayed by its Zack Rank #1 (Strong Buy).

— Derek Lewis

Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report.

Source: Zacks