Most investors love a bargain. Finding sound long-term stocks trading on the cheap can be a great way to juice your portfolio gains. But stocks typically trade cheaply for a reason, and we’ve all heard this warning: “Don’t catch a falling knife.”

However, Ferrari (RACE) is trading far below its historical valuations in part due to uncertainty surrounding its first full-electric vehicle (EV). And Stellantis (STLA) has plunged for the past three years amid waning market share and a lack of compelling products.

The good news is Ferrari still has plenty to offer investors, and Stellantis has a $70 billion turnaround plan. Let’s take a closer look.

Ferrari is rarely “cheap”

Ferrari is rarely “cheap”

Let’s get one thing out of the way immediately: Ferrari is a unicorn of an automotive stock. There simply aren’t many companies that can replicate the brand power or racing heritage — or even the technology that drips from its racing team to its retail supercar business.

Ferrari is unique in far more ways than just its brand and heritage, including the fact that the company keeps a lid on the volume of sales to ensure exclusivity remains a cornerstone for the automaker. The strict exclusivity — remember, it’s a lengthy and complicated process to even purchase a Ferrari — helps drive pricing power and ensures there’s never a surplus of available Ferrari vehicles.

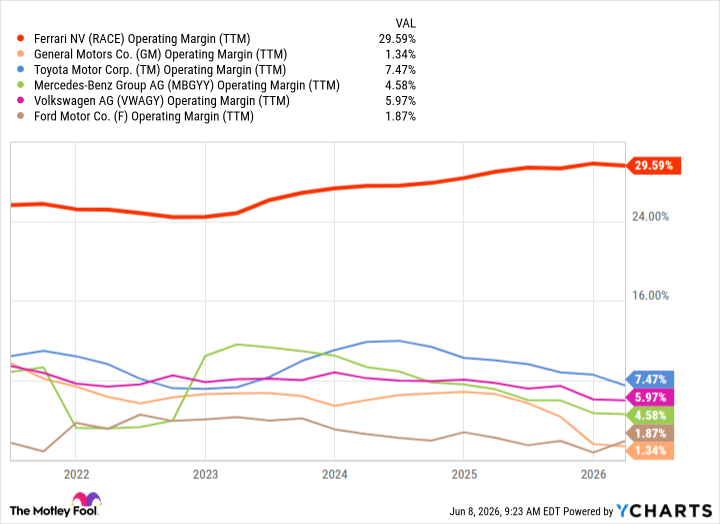

That exclusivity, pricing power, and control over sales volume all help the automaker drive margins sky-high compared to mainstream automakers. In an industry known for razor-thin margins and for being capital-intensive, Ferrari shatters the stereotype, as you can see below.

Another bonus with Ferrari is that its consumer base is simply in a different world than mainstream automakers’ target market. As such, Ferrari’s ultra-wealthy consumer base is largely immune to mainstream economic downturns, which makes the stock and business more resilient during recessions.

Another bonus with Ferrari is that its consumer base is simply in a different world than mainstream automakers’ target market. As such, Ferrari’s ultra-wealthy consumer base is largely immune to mainstream economic downturns, which makes the stock and business more resilient during recessions.

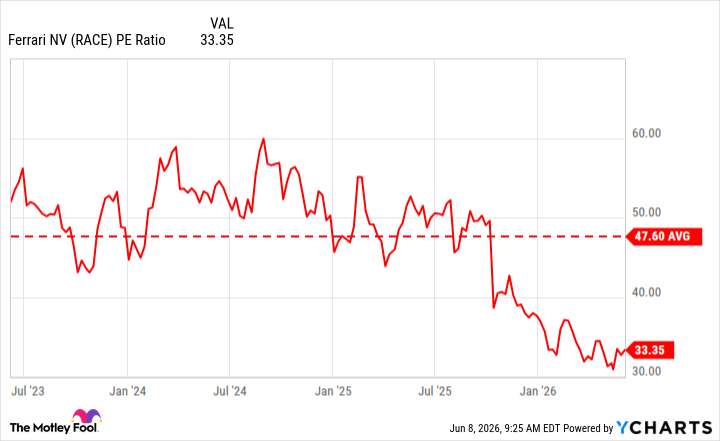

For these reasons, among many more, Ferrari rarely trades at a cheap valuation. But the stock is at an interesting point in time, when last year’s guidance through 2030 disappointed analysts — we should keep in mind Ferrari has previously low-balled guidance only to outshine it — and the recently unveiled electric vehicle, named Luce, made investors anxious with its design departure from traditional Ferrari designs. For those reasons, Ferrari is trading far below its usual valuation levels, as you can see below, giving investors a rare opportunity to scoop up shares more cheaply.

A turnaround plan with teeth

A turnaround plan with teeth

Stellantis CEO, Antonio Filosa, hasn’t taken long to make an impression on investors. On May 21, Stellantis launched a $70 billion five-year turnaround plan, with a new identity focusing 70% of that global investment on a handful of core brands: Jeep, Ram, Peugeot, Fiat, and Pro One (commercial business).

There are many components to the massive turnaround plan, but one of the simplest might be the most effective and noticeable. As many following the auto industry understand, there’s an affordability crisis as the average price of a new vehicle hovers around $50,000. It’s a part of the market you could certainly argue is vastly underserved at the moment, and Stellantis sees opportunity.

More specifically, Stellantis plans to launch nine vehicles priced less than $40,000 in North America by the end of this decade. Not only that, but two of those will check in under $30,000. While these lower average transaction prices (ATPs) likely come with slimmer margins, Stellantis also has a strong need to regain lost market share, improve sales volume, and increase its production capacity utilization.

On the back of these new launches, Stellantis is targeting adjusted operating income margins of 8% to 10% in North America by the end of 2030. It also targets growing sales volume in the region by 35%, and revenue by 25%, over the same time frame. Stellantis expects production capacity utilization to reach 80% by the end of the decade; focusing on affordability will be a huge boost to all those efforts.

Should investors buy now?

Should investors buy now?

While Stellantis and Ferrari are both automakers, they’re on very different ends of the spectrum — or really, Ferrari is in a world of its own. As both stocks have declined recently, Stellantis more steeply than Ferrari, there’s an opportunity to scoop up shares of perhaps one of the largest turnarounds in recent automotive history in Stellantis, and/or shares of Ferrari at a rare discount due to uncertainty around its first full-electric vehicle.

Both are compelling opportunities and warrant being on investors’ watch list for further research.

— Daniel Miller

Motley Fool Stock Advisor's average stock pick is up over 350%*, beating the market by an incredible 4-1 margin. Here’s what you get if you join up with us today: Two new stock recommendations each month. A short list of Best Buys Now. Stocks we feel present the most timely buying opportunity, so you know what to focus on today. There's so much more, including a membership-fee-back guarantee. New members can join today for only $99/year.

Source: The Motley Fool