Making money is hard, right?

But spending it?

Well, that’s a lot easier.

However, if you can scale back on the spending just a bit and instead invest that money, it can radically change your life over time.

This is especially true if you use the right long-term investment strategy.

So what is the right strategy?

Well, that depends quite a bit on who you are and what you’re looking to accomplish with your money.

But I’d argue that dividend growth investing is right up there with the best strategies.

This strategy is all about buying and holding shares in world-class enterprises that pay reliable, rising cash dividends to their shareholders.

There are many businesses out there selling the products and/or services that we all need and use every single day.

In doing so, these businesses make a lot of money.

So much money, in fact, that these businesses can’t always effectively use it all, leading some of that cash to flow right back to shareholders.

So much money, in fact, that these businesses can’t always effectively use it all, leading some of that cash to flow right back to shareholders.

You can find hundreds of these businesses by perusing the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Quite a few of these businesses have raised their dividends for more than 25 consecutive years.

When used correctly, the dividend growth investing strategy can be a powerful way to grow your wealth and passive income.

I’ve personally been using this strategy for more than a decade now, using it to build my FIRE Fund.

That’s my real-money portfolio, and it produces enough five-figure passive dividend income for me to live off of.

Indeed, I’ve been in the fortunate position to be able to live off of dividends for years now.

Indeed, I’ve been in the fortunate position to be able to live off of dividends for years now.

It’s been that way since I retired in my early 30s, something my Early Retirement Blueprint lays out in detail.

Now, as much as dividend growth investing can do for you, it’s important to pay attention to valuation at the time of investment.

Price only tells you what you pay, but it’s value that tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Abstaining from spending your money and instead investing that capital into undervalued high-quality dividend growth stocks can radically alter your life for the better.

Of course, spotting undervaluation at all first requires one to understand valuation.

No worries.

Fellow contributor Dave Van Knapp’s Lesson 11: Valuation is here to help you.

One of many “lessons” that are designed to teach the A-Z of DGI, it provides a simple-to-follow valuation template that can be applied toward just about any dividend growth stock you’ll find.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Robert Half Inc. (RHI)

Robert Half Inc. (RHI)

Robert Half Inc. (RHI) is a global staffing and consulting company.

Founded in 1948, Robert Half is now an $8 billion (by market cap) HR player that employs more than 16,000 people.

The company reports results across three different business segments: Contract Talent Solutions, 63% of FY 2022 revenue; Protiviti, 28%; and Permanent Placement Talent Solutions, 9%.

Approximately 80% of the company’s revenue is generated in the US, while the remaining 20% is internationally derived.

There are many business models out there that are quietly minting money, flying way under the radar.

Staffing/consulting, which is what Robert Half does, is a great example one such business model.

Here’s how Morningstar describes Robert Half: “Robert Half is a leading global staffing firms in a highly fragmented industry. The firm’s pricing power should persist, given its deep penetration into the small-midsize-business market. Local and regional staffers can win business on the fringes, but Robert Half’s decades of industry knowledge and well-established client relationships are hefty barriers that should keep smaller competitors at bay.”

That short description says so much with so few words.

The firm benefits from pricing power, consolidation opportunities, industry expertise, and barriers to entry.

If all of that isn’t good enough already, Robert Half is getting better.

Morningstar points this out: “Robert Half has been shifting to a higher-margin business mix. For one, we expect Protiviti’s contribution to continue increasing over the next decade and exceed one third of total revenue. Concurrently, the contract staffing segment (the lowest-margin business) will decrease in proportion.”

We’re now talking about an upshift in margins.

I like the sound of that.

Put simply, providing talent and consulting solutions is an effective, high-margin method for making a lot of money.

Robert Half is great at doing this, and it’s only becoming greater.

That’s what sets the firm up for being able to grow its revenue, profit, and dividend for years to come.

Dividend Growth, Growth Rate, Payout Ratio and Yield

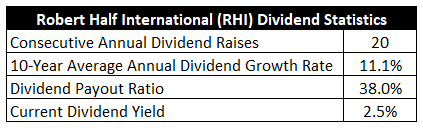

To date, the company has increased its dividend for 20 consecutive years.

That’s impressive.

It’s a better track record than one might initially expect, and it’s better than quite a few higher-profile names out there.

The 10-year dividend growth rate is 11.1%.

The 10-year dividend growth rate is 11.1%.

Strong.

Better yet, there’s been noticeable linearity here – even the most recent dividend raise was 11.6%.

And you get to layer that consistent double-digit dividend growth on top of the stock’s market-beating yield of 2.5%.

That’s a pretty nice combination of yield and growth.

By the way, this yield is 40 basis points higher than its own five-year average.

With a payout ratio of 38%, this is a well-covered, safe dividend.

Yield, growth, safety, consistency.

Robert Half checks the boxes.

A lot to like here, no matter what kind of dividend growth investor you are.

Revenue and Earnings Growth

As likable as these metrics may be, this data is mostly looking backward.

But investors must always be looking forward, as today’s capital is being put on the line for the rewards of tomorrow.

That’s why I’ll now build out a forward-looking growth trajectory for the business, which will be helpful when later estimating fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this manner should allow us to make an informed decision on where the business could be going from here.

Robert Half moved its revenue from $4.2 billion in FY 2013 to $7.2 billion in FY 2022.

That’s a compound annual growth rate of 6.2%.

Good stuff.

I usually look for a mid-single-digit top-line growth from a fairly mature business, and Robert Half is exceeding my expectations.

Meantime, earnings per share grew from $1.83 to $6.03 over this period, which is a CAGR of 14.2%.

Incredible bottom-line growth from an under-the-radar business.

A combination of extensive share buybacks and mild margin expansion propelled excess bottom-line growth.

For perspective on the former, the outstanding share count has been reduced by 21% over the last decade.

We can now see that double-digit dividend growth has been fueled by double-digit EPS growth.

However, I’d point out that the last two fiscal years were unusually strong for Robert Half.

EPS doubled between FY 2020 and FY 2022.

The business had been steadily growing before the pandemic hit, but pre-2020 EPS growth appeared to have been in a high-single-digit range.

Still great, but not so breathtaking.

Looking forward, CFRA is forecasting a 1% CAGR for Robert Half’s EPS over the next three years.

Honestly, this is strange.

I last looked at CFRA’s three-year EPS CAGR projection for Robert Half back in April.

What was it at that time?

It was 8%.

Moving from 8% to 1% in only a few months – on what’s supposed to be a multiyear call – seems inappropriate to me, and I suppose that’s why some investors don’t put much value on analyst forecasts.

To be fair to CFRA, I think they do a good job of summing up the current situation for Robert Half with this passage: “We think staffing placement volume is experiencing a headwind from rising interest rates bringing about recession fears, which cause [Robert Half] clients to pull back on hiring even if current business conditions are healthy, which we believe they are.”

Indeed, the US economy is humming along, unemployment remains low, and demand for labor is high.

All of that bodes well for Robert Half.

Okay, moving past the lack of conviction from CFRA, how do we think about the 1% number?

Well, beyond issues relating to rising interest rates and employer fears about the economy (unfounded or not), the main thing working against Robert Half, in my view, is the fact that the business is coming off of abnormally high results, and so the comps will be difficult.

From that standpoint, I can see a case for near-term pessimism.

Indeed, the company’s Q2 report – its most recent – showed a 37.5% YOY drop in EPS.

Robert Half is going through a painful period that will “reset” numbers back to normal levels.

This adjustment will be painful over the near term.

Once this normalization process is complete, however, Robert Half should be able to get back to business.

Based on what the business has been doing for many years now under regular circumstances, that implies something akin to high-single-digit EPS growth and, perhaps, slightly higher dividend growth.

Keep in mind, TTM EPS, which is what I based the payout ratio upon, already factors in recent dips in Robert Half’s business.

Even with the dips, the payout ratio, which is below 40%, indicates a healthy dividend.

It’s entirely possible, and even likely, that the next dividend raise or two could break from Robert Half’s linear divided growth history and be lower than what long-term shareholders are accustomed to, but I just find it hard to believe that the business is permanently impaired in any way.

And so my long-term view here is that Robert Half will remain capable – and is already clearly willing – to grow its dividend at a high-single-digit rate (or higher).

When you’re already collecting a 2.5% yield, that sets up investors for a very nice total return over the coming years, much of which will stem from plenty of cumulative dividend income.

Financial Position

Moving over to the balance sheet, Robert Half has a fantastic financial position.

The company has no long-term debt.

In an environment where interest rates are rising and debt is becoming more expensive to roll over, Robert Half is sitting pretty.

Moreover, whereas a lot of companies have been gorging on debt over the last decade, Robert Half ended FY 2022 with a cash position that was more than twice as high as it was 10 years ago.

This fortress balance sheet is a huge edge for Robert Half as the business moves through some turbulence.

Profitability is excellent.

Net margin has averaged 7.8% over the last five years, while return on equity has averaged 39.1%.

The margin expansion story is worth touching on, as Robert Half’s net margin was routinely in the 6% area in the first half of the prior 10-year period.

The returns on capital here are very high, and I’d also point out that ROE hasn’t been juiced by debt.

It’s all pretty remarkable.

Fundamentally speaking, this is a terrific business.

And with brand strength, a network effect, entrenched relationships, and a built-up database, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Robert Half is highly exposed to economic cycles, as a healthy economy supports demand for workers and hiring activity (and vice versa).

Any broad changes in work and/or the workforce could impact the industry and company.

Less outsourcing of HR needs would have a negative effect on Robert Half.

Technological innovation, such as networking sites and AI, could disrupt the business model.

Most of the company’s revenue is derived from the US, but Robert Half does have some modest exposure to currency exchange rates and foreign lands.

These risks should be carefully thought over, but the quality of the business has to be part of that thought process.

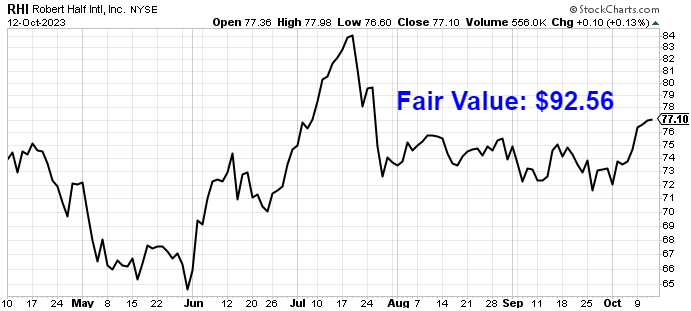

In addition, with the stock down 14% from its recent high, the valuation looks attractive…

Stock Price Valuation

The P/E ratio is 15.3.

Keep in mind, the E in this ratio is based on TTM EPS and has already absorbed recent drops in earnings, and yet it’s still this low.

This is well below the broader market’s earnings multiple.

It’s also way off of the stock’s own five-year average P/E ratio of 17.9.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 8%.

Now, this growth rate is at the high end of what I allow for.

But I think Robert Half deserves it.

After all, the company has delivered consistent double-digit dividend growth for two straight decades – a time period that stretches across both the GFC and the pandemic.

And the balance sheet is as clean as it gets.

Plus, the payout ratio is low, even after some normalization in earnings.

Again, it’s quite possible, even likely, that the next dividend raise or two is modest.

Management may choose to be conservative in this environment, and I think that’d be just fine.

However, the long-term, go-forward setup for Robert Half’s dividend growth doesn’t seem all that different from what’s already taken place over the last twenty years.

The DDM analysis gives me a fair value of $103.68.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

I don’t see how my valuation model was overly aggressive, yet the stock comes out looking rather cheap.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates RHI as a 4-star stock, with a fair value estimate of $94.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates RHI as a 3-star “HOLD”, with a 12-month target price of $80.00.

I came out on the high end this time around, but we all see attractiveness here. Averaging the three numbers out gives us a final valuation of $92.56, which would indicate the stock is possibly 17% undervalued.

Bottom line: Robert Half Inc. (RHI) is an under-the-radar name that is growing rapidly and putting up high returns on capital, all while running without any long-term debt. It’s a terrific business. With a market-beating yield, double-digit long-term dividend growth, a low payout ratio, 20 consecutive years of dividend increases, and the potential that shares are 17% undervalued, dividend growth investors looking for an outside-the-box idea could have something very interesting here.

Bottom line: Robert Half Inc. (RHI) is an under-the-radar name that is growing rapidly and putting up high returns on capital, all while running without any long-term debt. It’s a terrific business. With a market-beating yield, double-digit long-term dividend growth, a low payout ratio, 20 consecutive years of dividend increases, and the potential that shares are 17% undervalued, dividend growth investors looking for an outside-the-box idea could have something very interesting here.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is RHI’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 96. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, RHI’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income