Growing up my Grandma didn’t have a cookie jar.

She had something even better…

A Twinkie drawer.

And at family gatherings, she loved telling the story about the night little Brad snuck downstairs and ate an entire box of those delicious pastries.

It’s no wonder Twinkies still hold a special place in my heart.

So when the news broke last week that J.M. Smucker Company (SJM) was buying Hostess Brands (the maker of Twinkies) for a cool $5.6 billion… my first thought was, “Good for Twinkies.”

And my second thought was, “I need to take a look at Smucker’s.”

So today I am going to share with you my findings and why you want to buy J.M. Smucker along with all its iconic American brands like Twinkies, Ding Dongs, Zingers, or HoHos. Not only will you own a little piece of your childhood, you’ll also receive an attractive dividend and appealing valuation after its post-merger selloff.

The American Brands You Know and Love

I have to admit, it’s been years since I’ve eaten a Twinkie.

These days I try to be more disciplined when it comes to my diet and exercise.

But, as it turns out, my health food trend and “no snacking” policy is not the norm. So Twinkies, Hostess, and Smucker’s have a long profitable road ahead.

A recent report by Circana shows that in 2023 snacking is more popular than ever.

49% of Americans snack at least 3 times per day. And this trend is up 8% in the last 2 years alone.

Source: Circana: The Snacking Supernova)

Source: Circana: The Snacking Supernova)

People can’t get enough of their favorite sweet and salty indulgences.

And J.M. Smucker is set to gain, owning lead market share positions in several major food categories.

Not only do they own the Smucker’s jelly brand, but they also own Jif Peanut Butter.

You heard that right.

J.M. Smucker owns the most brand-recognizable ingredients to the most iconic American sandwich. And one of the most popular childhood snacks.

They also own Folgers coffee, Dunkin’ at Home, Cafe Bustelo, Milk Bone, Meow Mix, and Pup-Peroni.

So even if you haven’t eaten that classic PB&J sandwich in quite a bit, chances are you’ve still been buying one or more J.M. Smucker brands on the regular.

So how will the popularity of these brands and J.M. Smucker’s massive portfolio put money in your wallet?

An Attractive Dividend and Appealing Valuation Despite Market Sentiment

J.M. Smucker is set to bring in an additional $1.5 billion in annual sales with their purchase of Hostess Brands.

And this recent announcement was met with a 10% drop in share price since the start of the month.

Why?

Because of the risks associated with cash leaving and debt entering the balance sheet.

To fund its Hostess purchase, J.M. Smucker raised $5.2 billion in debt.

And overall, they expect their total debt after closing the deal to be about $8.6 billion.

This is scaring investors… but they are ignoring the fact that Hostess Brands will boost J.M. Smucker’s sales and grow its cash flows significantly. An additional $1.5 billion a year in annual sales is no joke.

Smucker also expects to save $100 million a year – in the first two years – after the merger.

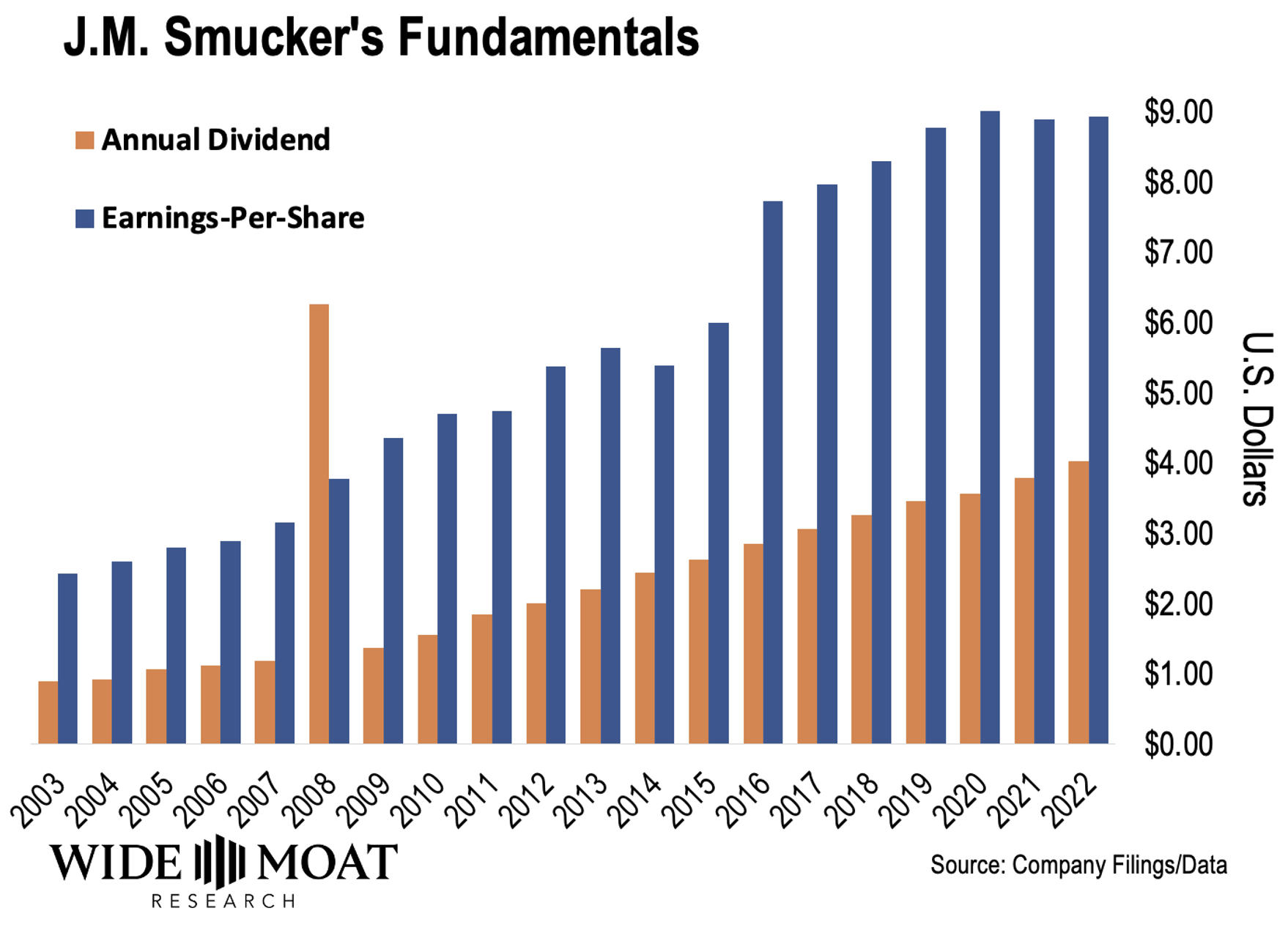

So the company should be able to use its increased cash flows to quickly pay down the debt. And continue paying and increasing their dividend… one they’ve been increasing for 22 years in a row.

Right now, J.M. Smucker’s dividend payout ratio is 73%, and it’s 5-year dividend growth rate of 5.25% is quite impressive.

And this is before the benefits of Hostess Brands kicks in…

So where does that leave you?

With a great opportunity…

SJM shares currently yield 3.33%.

And that 10% selloff in J.M. Smucker shares, has pushed their forward price-to-earnings (P/E) multiple down to just 13x.

For a stock like this, investors are usually willing to pay more for next year’s profits.

But its trading at well below its 5, 10, and 20-year average P/E multiples of 14.7x, 16.7x, and 16.7x, respectively.

So it’s trading at a 22% discount in comparison to its usual valuation.

J.M. Smucker has also grown its earnings-per-share during 18 out of the last 20 years.

*2008 dividend includes a $5.00/share special dividend

*2008 dividend includes a $5.00/share special dividend

And I am expecting to see 5+% earnings-per-share growth over the next couple of years regardless of the debt investors are worried about.

So what you’re left with is a profitable powerhouse trading at a discount. And the market will catch on eventually…

But before it does, make sure you take advantage of this opportunity.

Happy SWAN (sleep well at night) investing,

Brad Thomas

Editor, Intelligent Income Daily

Source: Wide Moat Research