Price is what you pay. But value is what you get. A well-known phrase.

Perhaps one I use too often. But it’s so instructional, despite how pithy it is.

Whereas we all like to focus on price, it’s value that ultimately matters most. And in the stock market, a share of a business is something that’s constantly fluctuating in price.

However, the underlying value of that same business – it’s not fluctuating very much at all. Buying when there’s a favorable gap between price and value, that can make a tremendous difference over the long run. Plus, because price and yield are inversely correlated, lower prices will result in higher yields, all else equal. All of this can happen when a sudden and severe drop in pricing occurs.

Today, I want to tell you about 5 dividend growth stocks that are down more than 20% from their recent highs.

Ready? Let’s dig in.

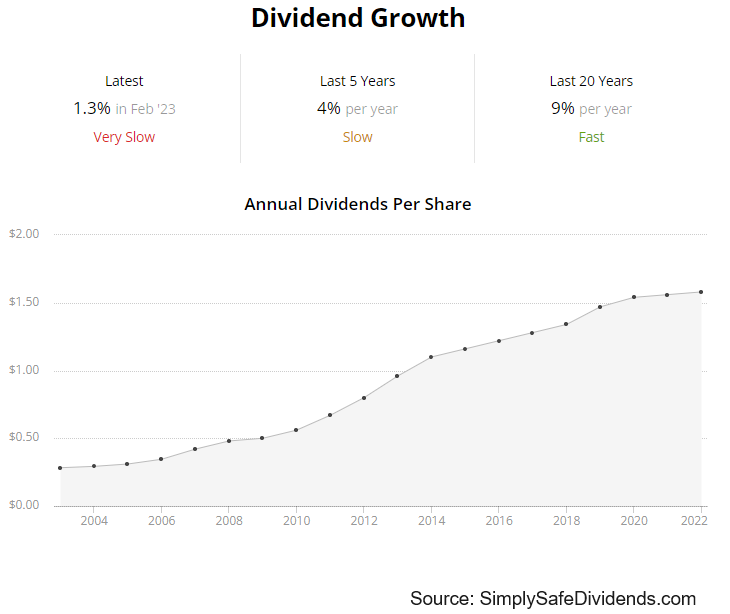

The first dividend growth stock I have to highlight today is Albemarle Corporation (ALB). Albemarle is a specialty chemicals manufacturing company.

This isn’t your run-of-the-mill chemicals company. No, Albemarle is the world’s largest producer of lithium. You know, the stuff that’s starting to power the next wave of energy and transportation. EVs, for example, need batteries. And what do those batteries need? Lithium. Investing in Albemarle today could be similar to what you’d experience by going back in time and investing in oil & gas companies at the dawn of the automobile. But you’re not gambling on some unproven player going hard on new technologies. Albemarle already has a great track record for revenue, profit, and dividend growth.

The chemicals company has increased its dividend for 29 consecutive years. Yes, this is a Dividend Aristocrat. What makes Albemarle so unique as an investment idea for long-term dividend growth investors is that you’re taking what’s already a Dividend Aristocrat and then bolting on exciting growth from rising lithium demand. The 10-year DGR is 7.3%, although recent dividend raises have been in a low-single-digit range. And that’s because Albemarle has been heavily investing in capacity.

The stock’s yield of 0.9% isn’t super high, but this isn’t a yield play. A yield of somewhere around 1% is pretty common for high-growth, high-quality compounders. With a payout ratio of only 5.9%, based on midpoint guidance for this year’s adjusted EPS, this is obviously a very secure dividend. That’s one of the lowest payout ratios I know of.

The stock’s yield of 0.9% isn’t super high, but this isn’t a yield play. A yield of somewhere around 1% is pretty common for high-growth, high-quality compounders. With a payout ratio of only 5.9%, based on midpoint guidance for this year’s adjusted EPS, this is obviously a very secure dividend. That’s one of the lowest payout ratios I know of.

Despite all of this, the stock is down a jaw-dropping 45% from its 52-week high. The 52-week high of $334.55 is long gone, as the stock’s price is now bumping around the $184 mark. Of course, like I said earlier, price can and will fluctuate often. Value? Not so much. Indeed, every basic valuation metric is now substantially off of its respective recent historical average. EPS of late has been all over the place. But if we drill down into sales, the current P/S ratio of 2.2 is less than half of its own five-year average of 4.5.

Now, as much as I like Albemarle, you have to remember that you’re getting a lot of commodity exposure here. And commodities can be very volatile in terms of pricing. So I would expect a lot of volatility in the price of Albemarle’s stock. Is that worth dealing with in order to get a Dividend Aristocrat that’s leading the charge on lithium? Hard to argue against it.

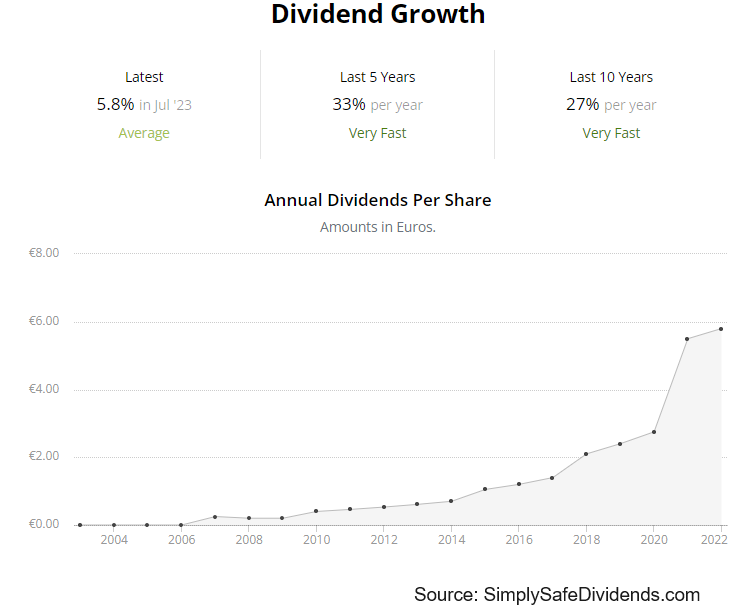

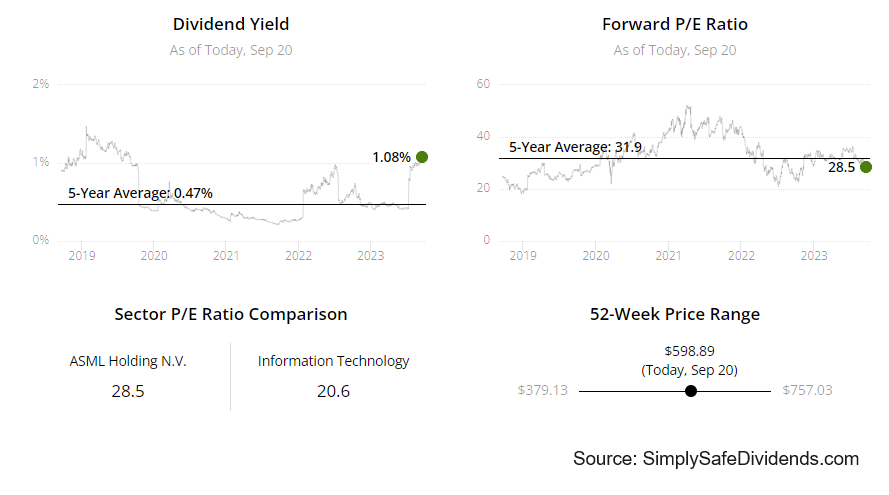

The second dividend growth stock I want to bring up today is ASML Holding (ASML). ASML is a provider of advanced semiconductor equipment systems.

This is one of the best businesses I’ve ever seen. Double-digit top-line and bottom-line growth over the last decade. High returns on capital. Fat margins. Stellar balance sheet. Huge backlog of orders. And one of the widest economic moats out there. I mean, it’s nearly impossible to compete, as ASML has a virtual monopoly when it comes to EUV lithography machines. I would be shocked if ASML doesn’t do extremely well over the next decade, which bodes well for the dividend. The semi cap equipment company has increased its dividend for 13 consecutive years.

That’s in its native currency. ASML pays its dividend in euros. The dividend more than doubled between FY 2019 and FY 2022. That’s good for a CAGR of 34.2%. Just amazing growth out of ASML. A payout ratio of 41%, based on FY 2022 numbers, leaves plenty of room for future dividend raises. It’s one of the healthiest and fastest-growing dividends out there. And you really do want to see a lot of growth here, as the stock’s yield is only 1.1%.

This has historically been a very strong long-term performer, but it’s 23% lower than its recent high. The current price of $597 compares very favorably to its 52-week high of $771.98. That’s without question. But that’s not the right comparison. It’s not price against price. It’s price against value, remember? So we know the price we’re paying, but do we know the value we’re getting?

This has historically been a very strong long-term performer, but it’s 23% lower than its recent high. The current price of $597 compares very favorably to its 52-week high of $771.98. That’s without question. But that’s not the right comparison. It’s not price against price. It’s price against value, remember? So we know the price we’re paying, but do we know the value we’re getting?

Well, I already put together a full analysis and valuation piece on this business, and the estimate for fair value came out to $791.37/share. That video should be live soon, if it’s not already. Despite the recent drop, this stock is still up nearly 220% over the last five years. In my view, this is a very high-quality business that’s available for an attractive valuation. Take a look.

Well, I already put together a full analysis and valuation piece on this business, and the estimate for fair value came out to $791.37/share. That video should be live soon, if it’s not already. Despite the recent drop, this stock is still up nearly 220% over the last five years. In my view, this is a very high-quality business that’s available for an attractive valuation. Take a look.

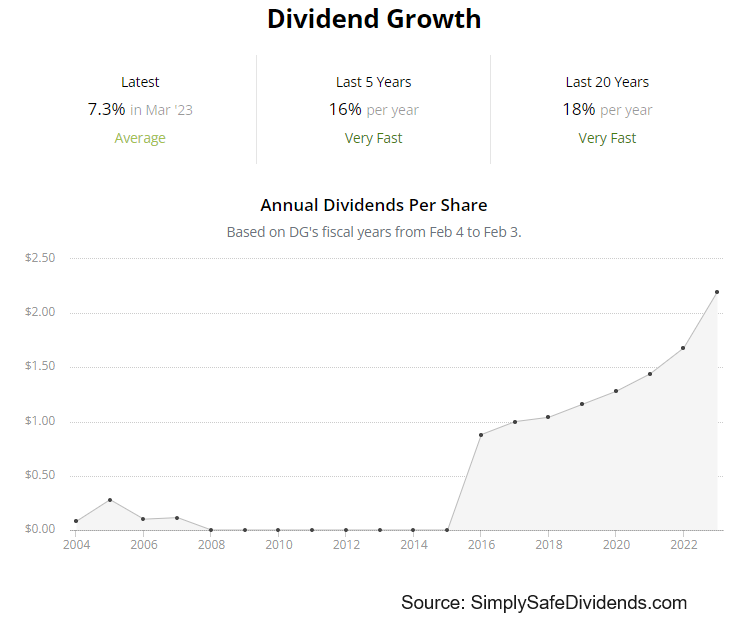

The third dividend growth stock we should talk about is Dollar General (DG). Dollar General is an American chain of neighborhood general stores that focus on low-cost merchandise.

This is a business that has done very well over a very long time by perusing a very simple model of installing stores full of low-cost merchandise in rural locations that have consumers with lower purchasing power and limited competing options.

If you don’t have a super high income, and if there aren’t a lot of other options out there, Dollar General and its cheaper merchandise starts to become a pretty good shopping option. That’s why it’s grown a lot faster than many other retailers out there, with an EPS CAGR of nearly 15% over the last decade. And that’s supported very nice dividend growth along the way. The retailer has increased its dividend for nine consecutive years.

The five-year DGR of 15% matches up very nicely with EPS growth. And you even get a 2% yield here, which is a stunning 110 basis points higher than its own five-year average. This has typically been a lower-yielding compounder, but recent stumbles, due to reasons ranging from shrink to merchandising, have caused the market to reprice the stock down. And we know that price and yield are inversely correlated, which explains the jump in yield. Still, even with lowered midpoint earnings guidance for this year, the payout ratio, on a forward-looking basis, is only 30.1%. That’s not cumbersome at all.

The five-year DGR of 15% matches up very nicely with EPS growth. And you even get a 2% yield here, which is a stunning 110 basis points higher than its own five-year average. This has typically been a lower-yielding compounder, but recent stumbles, due to reasons ranging from shrink to merchandising, have caused the market to reprice the stock down. And we know that price and yield are inversely correlated, which explains the jump in yield. Still, even with lowered midpoint earnings guidance for this year, the payout ratio, on a forward-looking basis, is only 30.1%. That’s not cumbersome at all.

This stock has been obliterated, now down 56% from its 52-week high. What a drop for what’s long been a bit of a retail stalwart. Did the 52-week high of $261.59 get ahead of itself? I think so. That kind of price level seemed unwarranted. It was just way too expensive for what you were getting. However, is the current pricing of $116 unwarranted on the other side? Has the pendulum swung too far to the other way?

It seems so. Our recent analysis and valuation video on the retailer estimated fair value for the business at $188.90/share. There’s a lot of pessimism baked in here. If you’re looking for a deep discount on a discount retailer, this could be right up your avenue.

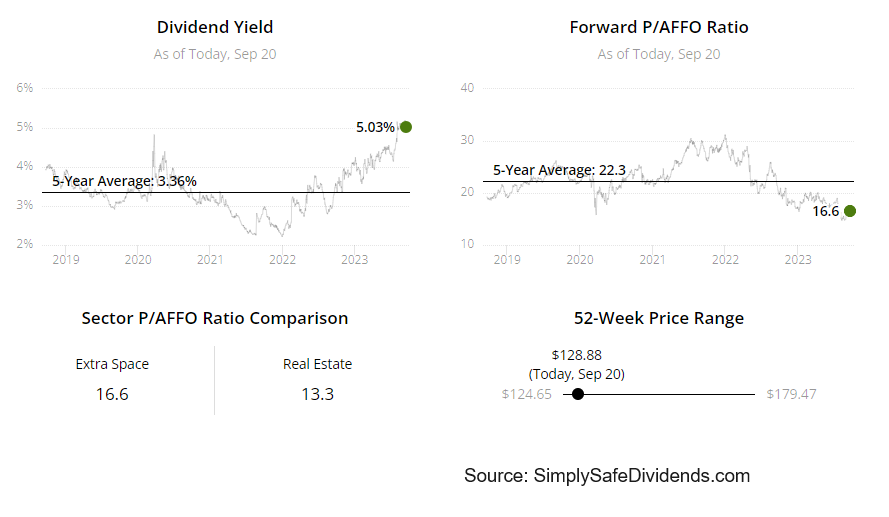

The fourth dividend growth stock that deserves a mention today is Extra Space Storage (EXR). Extra Space Storage is a real estate investment trust that invests in self-storage facilities. This REIT is very interesting. What we have here is a business model catering to Americans’ seemingly limitless craving for stuff. And when houses get too full of stuff, that leads people to getting a storage unit for the leftovers.

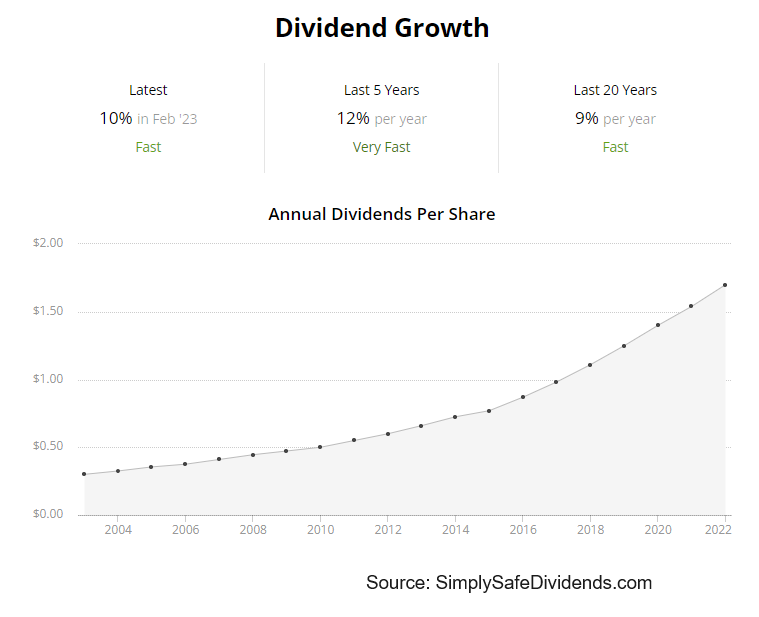

What’s great about self-storage real estate is that there are very little operating costs, it’s easy to scale, and the opportunity to right-size pricing is constantly there because of the way in which leases tend to be shorter term. All of this has led to strong operating metrics for years, which has then led to strong dividend growth for years. The REIT has increased its dividend for 14 consecutive years.

This is a rare REIT that offers both yield and growth. Most REITs are simple yield plays. But Extra Space Storage kicks things up a notch with its five-year DGR of 14%. Now, that’s not something that one should expect to persist forever. However, even the most recent dividend raise came in at 8%. That’s uncommon for a REIT. Yet the stock still yields a REIT-like 5.1%. So you get to have your cake and eat it, too. The payout ratio is 78.5%, based on midpoint guidance for this year’s FFO/share. Elevated. But not at all uncommon for a REIT.

Is this stock’s 31% decline from its 52-week high a buying opportunity?

It looks like it, assuming you’re in it for the long term. The 52-week high of $183.49 was simply too high a price to pay for shares in the business. But now at about $127/share, this REIT looks a lot more interesting. Same business. But two totally different prices.

It looks like it, assuming you’re in it for the long term. The 52-week high of $183.49 was simply too high a price to pay for shares in the business. But now at about $127/share, this REIT looks a lot more interesting. Same business. But two totally different prices.

Based on that aforementioned guidance, the forward multiple of FFO/share is 15.4. That’s somewhat analogous to a P/E ratio on a normal stock, giving you an idea of how undemanding the valuation has become. Also, the P/CF ratio of 14.7 is significantly lower than its own five-year average of 21.9. This name is far cheaper, in valuation terms, than it usually is. Might be time to seriously consider it.

The fifth dividend growth stock we have to talk about is NextEra Energy (NEE). NextEra Energy is an American energy company.

By market cap, this is the largest utility holding company in the US. NextEra Energy provides electricity to over 12 million people across the state of Florida. Since people can’t realistically live without electricity in a modern-day society, investing in a successful utility is appealing for long-term investors who desire recurring cash flows.

However, NextEra Energy is also the world’s largest generator of renewable energy from the wind and sun, and it’s also a world leader in battery storage. So it offers something to like for both old-line utility fans and those who are clamoring for exposure to renewables. This is a rare growth utility, which also shows up in the dividend. The energy company has increased its dividend for 29 consecutive years.

Yep. This is a Dividend Aristocrat. One of only three utilities that can claim that elite status. On one hand, you have the comfort of a proven winner. On the other hand, you have that future-oriented side of the business. That’s a compelling mix. Also compelling is the 10-year DGR of 11%, which is absurdly high and almost unheard of for a utility.

Now, at 2.7%, the yield here isn’t quite as high as what you see with other utilities. But I think the growth more than makes up for that slight shortcoming. A 60.9% payout ratio, based on midpoint guidance for this year’s adjusted EPS, gives NextEra Energy plenty of leeway for continued dividend growth.

Now, at 2.7%, the yield here isn’t quite as high as what you see with other utilities. But I think the growth more than makes up for that slight shortcoming. A 60.9% payout ratio, based on midpoint guidance for this year’s adjusted EPS, gives NextEra Energy plenty of leeway for continued dividend growth.

I think this stock’s 23% decline from its recent high has created an attractive valuation. At the 52-week high of $88.61, the stock looked overvalued. At the current pricing of about $68, the stock looks undervalued. A 23% price swing in one direction can move something from overvalued to undervalued. And that’s why you always want to anchor yourself to value, not price.

We recently put together a full analysis and valuation piece on NextEra Energy, and the video should be live soon. The estimate for NextEra Energy’s fair value came out to $81.47/share. So I think we’re looking at a decent amount of undervaluation on what is probably the best utility business in the US.

We recently put together a full analysis and valuation piece on NextEra Energy, and the video should be live soon. The estimate for NextEra Energy’s fair value came out to $81.47/share. So I think we’re looking at a decent amount of undervaluation on what is probably the best utility business in the US.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income