Live below your means. Intelligently invest your capital for the long run. It’s such a simple recipe for financial success. But it just plain works.

So what is intelligent investing? Well, dividend growth investing comes to mind right away.

This is a strategy whereby you buy and hold shares in high-quality businesses that pay safe, growing dividends to shareholders. You buy these shares when undervaluation is present. And then you hold for decades, reinvesting those growing dividends along the way.

High-quality dividend growth stocks are some of the best stocks in the world. That’s because they represent equity in some of the best businesses in the world.

After all, the only way to fund ever-rising dividends is to produce the ever-rising profits necessary to afford that behavior. And only truly great businesses can produce ever-rising profits.

That said, you should be considering your age. Investing in your 30s isn’t exactly like investing in your 60s or 70s.

There are differences in aspects like time horizon, risk tolerance, income needs, etc. If you’re in your 30s, the word that comes to mind is “balance”. A decent amount of passive dividend income coming in now, which offers optionality, is nice. But you also have to balance that against the growth of the assets, which will favor the older version of yourself. And that balance between yield and growth is what we’re diving into.

Today, I want to tell you about three dividend growth stocks to consider buying if you’re in your 30s.

Ready? Let’s dig in.

The first dividend growth stock I want to talk about is Johnson & Johnson (JNJ). Johnson & Johnson is a multinational healthcare conglomerate.

This company has been around since 1886. Think about that. Nearly 140 years of corporate history. How has Johnson & Johnson managed to be so relevant for so long? By focusing on healthcare, which has been in, and will continue to be in, secular growth mode. Part of the human condition is aging and slow decay, which filters you right into needing healthcare.

No human being is immortal. We are all slowly aging, which, over time, increases the risk of all kinds of health issues. And what do we know about our species? There’s more than ever of us walking around. We’re living longer than ever before. And we’re, on average, richer than we’ve ever been. That trifecta naturally puts upward pressure on demand for quality healthcare, which plays right into the hands of Johnson & Johnson.

This company exudes quality in almost every way. It’s one of only two companies in the world with a AAA credit rating from S&P. The balance sheet is solid as a rock. Top-line and bottom-line growth are clockwork-like, with both up about 50% over the last decade.

The stock performs. We’re talking about a stock that’s up 5,400% over the last 40 years, before dividends. The company’s diversification, with exposure to pharmaceuticals, medical devices, and consumer products, has insulated it from economic and product cycles. Want more evidence of quality?

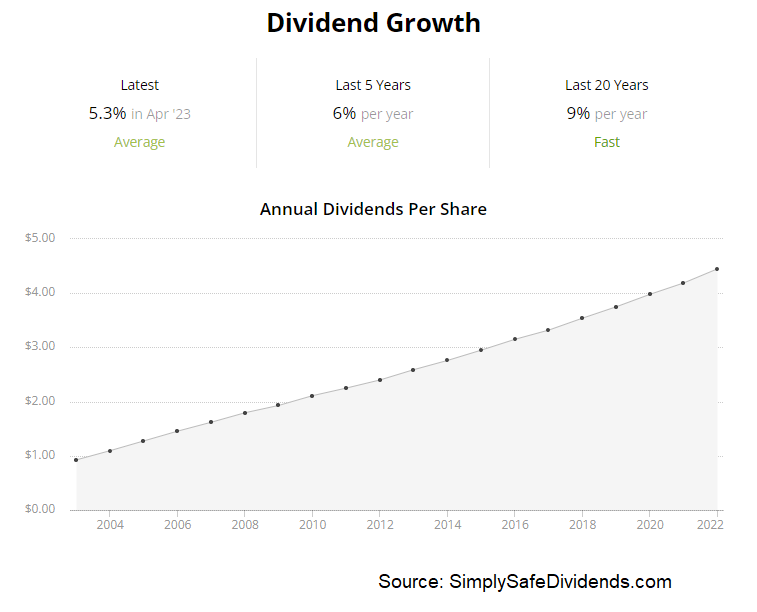

This dividend is the epitome of quality. Johnson & Johnson has increased its dividend for 61 consecutive years. It’s a Dividend Aristocrat. Not only that. It’s a Dividend King. If there were another, even higher category than Dividend King, Johnson & Johnson would be in it. The 10-year DGR is 6.4%, which lines up pretty well with business growth.

Not lightning fast, no. But there’s a nice balance here, which you can see with the stock’s yield of 3%. Nice yield. Nice dividend growth. And the payout ratio is only 44.7%, based on midpoint guidance for this year’s adjusted EPS. That payout ratio balances retaining earnings for growth against returning capital back to shareholders. Quality and balance. Johnson & Johnson.

Not lightning fast, no. But there’s a nice balance here, which you can see with the stock’s yield of 3%. Nice yield. Nice dividend growth. And the payout ratio is only 44.7%, based on midpoint guidance for this year’s adjusted EPS. That payout ratio balances retaining earnings for growth against returning capital back to shareholders. Quality and balance. Johnson & Johnson.

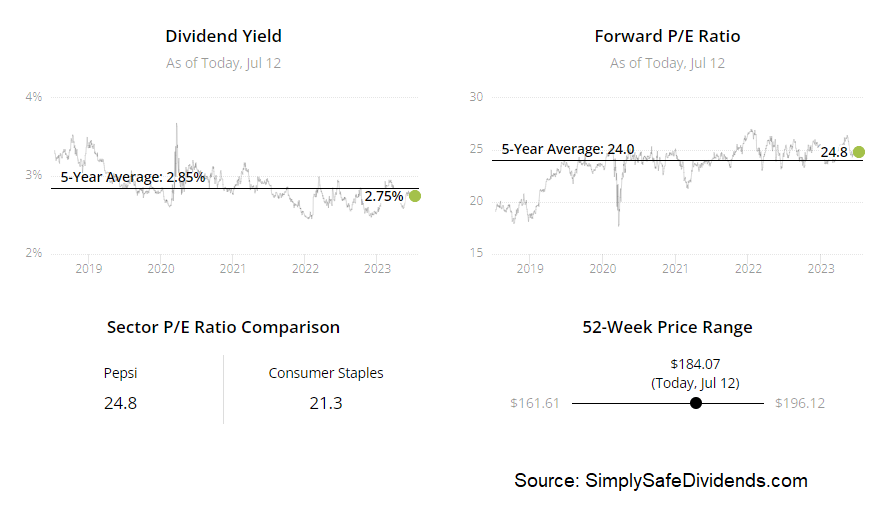

Speaking of balance, I think the valuation is fair and balanced. Based on that aforementioned guidance, the forward P/E ratio is 15. Is an earnings multiple of 15 too much for a world-class business like Johnson & Johnson? I really don’t think so.

Another way to look at it is the sales multiple, which is currently 4.4. Its own five-year average is 4.8. Relative to itself, it’s cheaper than usual. I’ll admit that this company isn’t quite as desirable as it used to be. Growth over the last few years has been underwhelming. And litigation has been a thorny issue. But the three main businesses within Johnson & Johnson are world-class operations. It’s been a winner for decades. And I don’t see that changing drastically, moving forward.

The second dividend growth stock that I want to highlight is PepsiCo (PEP). PepsiCo is a multinational food, snack, and beverage corporation.

We’ve all gotta eat, right? But there’s more to it than basic necessity. We want to enjoy our food and beverages. That’s where PepsiCo comes in, which provides some of the most popular and in-demand beverages and snacks in the world. Are human beings going to suddenly stop wanting to eat snacks tomorrow, a year from now, or 10 years from now? Highly, highly unlikely.

PepsiCo owns some of the world’s most iconic brands. Pepsi, Gatorade, Doritos, and Lay’s are but a few. In total, PepsiCo has 23 different billion-dollar brands, or brands that do more than $1 billion in sales per year.

Many companies would love to have just one brand that does something like that. PepsiCo has more than 20. The company’s foundation is built upon, and strengthened by, these brands, which has helped it to generate steady growth for decades.

Many companies would love to have just one brand that does something like that. PepsiCo has more than 20. The company’s foundation is built upon, and strengthened by, these brands, which has helped it to generate steady growth for decades.

How much growth? You’d be surprised. The stock price is up almost 10,000% over the last 40 years, and that’s been fueled by underlying business growth. To call PepsiCo a winner is underselling it. It’s been a fantastic long-term investment.

If we zoom into more recent performance, the stock has a CAGR of 11.3% over the last decade, including reinvested dividends. That’s a heck of a total return profile from a well-known snack and beverage company. The S&P 500 has an annualized total return of close to 10% over the long run. That’s basically my benchmark. Beating that in a low-risk way is always going to be compelling to me.

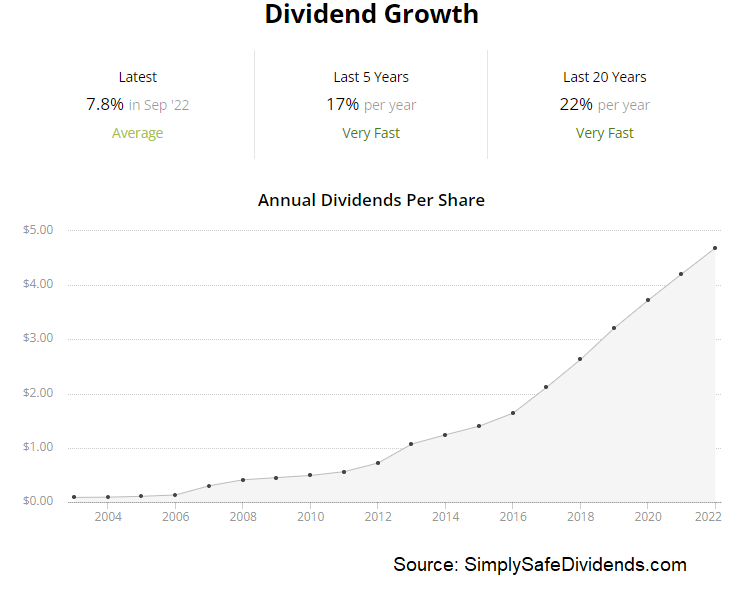

You know what else is compelling? The dividend and the growth of it. That’s right. PepsiCo has increased its dividend for 51 consecutive years. Another Dividend Aristocrat and Dividend King here. The 10-year DGR of 7.8% gets paired with the stock’s 2.8% yield.

So you get a market-beating yield. And you get inflation-beating dividend growth.

Furthermore, this is just a great balance between yield and growth. Assuming a static valuation, the sum of yield and growth should get you to your annualized total return. Indeed, this sum of 10.6 lines up pretty nicely with the stock’s actual 10-year CAGR. With the payout ratio sitting at 69.6%, based on Core EPS guidance for this fiscal year, I don’t see any issues with the health of this dividend.

This stock isn’t super cheap, nor should it be. But if you’re an investor in your 30s and investing for decades to come, I wouldn’t get too stressed about it.

Yes, of course, valuation is important. Don’t get me wrong You should never egregiously overpay, even for a high-quality business like PepsiCo. But way too many people take valuation way too seriously. Over the course of 40 years, it’s business performance, not valuation at the time of investment, that will matter most.

You want to invest in great businesses, not buy cheap stocks. The forward P/E ratio, using that aforementioned guidance, is 25.4. I don’t think that’s egregious for a business like PepsiCo. It’s P/S ratio of 2.9 is barely ahead of its own five-year average of 2.8.

A pullback would be nice. However, buying this stock at 5% lower than this level will be effectively meaningless 40 years from now. PepsiCo should definitely be considered right here, right now for long-term dividend growth investors.

A pullback would be nice. However, buying this stock at 5% lower than this level will be effectively meaningless 40 years from now. PepsiCo should definitely be considered right here, right now for long-term dividend growth investors.

The third dividend growth stock I have to bring up today is Texas Instruments (TXN). Texas Instruments is an American technology company.

Texas Instruments designs and manufactures semiconductors and various integrated circuits. The company is heavily involved in analog semiconductors, which are crucial to data conversion. Analog sensors measure things like temperature, sound, and movement. Many modern-day devices, like smartphones, don’t really operate without analog sensors. The world is becoming more digital, more technological, and more reliant on semiconductors of all kinds.

If you’re in your 30s, you want to be invested in secular trends that have decades of runway ahead. I already discussed healthcare and food. The world will almost certainly not be demanding less of either 40 years from now. Well, the same goes for high-tech products like those that Texas Instruments produces and sells. This is a story that’s been playing out for decades already. And I think it’s just getting started.

This story has a long way to go. And what a beautiful story it is. If you tend to buy high-yield junk stocks that perform terribly over the long term, you might want to look away. Because Texas Instruments is the opposite of that. And it might break your heart to see, yet again, that chasing yield is the wrong way to go.

This stock is up almost 7,000% over the last 40 years. Over the last decade alone, it’s compounded at an annual rate of 19.9%. Using the Rule of 72, that doubles your money every 3.5 years. It’s a monster. All this company does is routinely grow its revenue, profit, and free cash flow, buy back its own shares hand over fist, run a tight balance sheet, and prudently expand capacity.

Texas Instruments is a prototypical dividend growth stock. It shines in every way. The dividend has been increased for 19 consecutive years. The 10-year DGR is 20.8%. You’ll notice how well that lines up with the stock’s 10-year CAGR.

The stock also offers a 2.8% yield, which is 20 basis points higher than its own five-year average. If every stock I ever bought gave me this kind of yield and this kind of dividend growth, I’d be a very happy investor. More recent dividend raises have been a bit modest, but that’s mostly because of the CapEx cycle.

The stock also offers a 2.8% yield, which is 20 basis points higher than its own five-year average. If every stock I ever bought gave me this kind of yield and this kind of dividend growth, I’d be a very happy investor. More recent dividend raises have been a bit modest, but that’s mostly because of the CapEx cycle.

Texas Instruments is expanding for the next decade or two of growth. Music to the ears of a younger dividend growth investor. The payout ratio of 55.7% gives the company plenty of dividend headroom during this cycle.

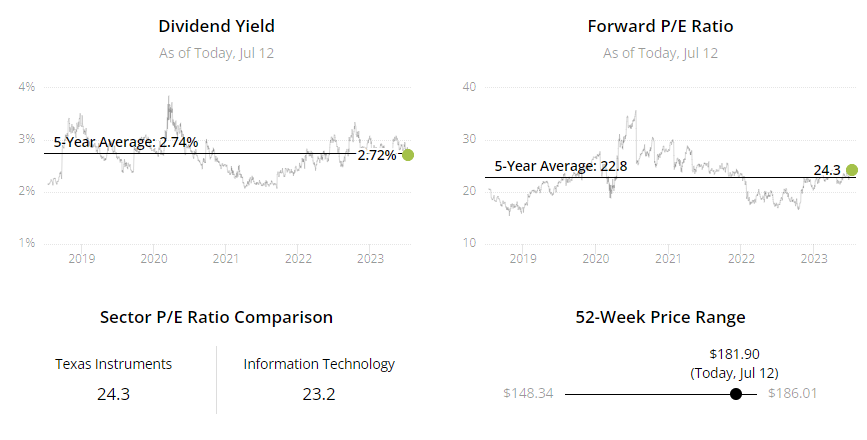

This stock is almost never cheap. But, right now, it’s about as reasonably valued as it ever gets. Its own five-year average P/E ratio is 22.8. So you can see how it’s usually in that elevated zone. Right now, though, the P/E ratio is 20.1.

Why? Well, I think it’s a combination of traders chasing momentum in more exciting areas of tech that have to do with AI, as well as the fact that the business is in the middle of expanding capacity. That will weigh on near-term results. But if you’re in your 30s, you’re not concerned about near-term results. You’re concerned about compounding over the next 30 or 40 years. And when it comes to that, Texas Instruments is a class act.

Why? Well, I think it’s a combination of traders chasing momentum in more exciting areas of tech that have to do with AI, as well as the fact that the business is in the middle of expanding capacity. That will weigh on near-term results. But if you’re in your 30s, you’re not concerned about near-term results. You’re concerned about compounding over the next 30 or 40 years. And when it comes to that, Texas Instruments is a class act.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income