Warren Buffett is undoubtedly one of the greatest investors to ever live, if not the greatest. We’re talking about compounding money at a 20% annual rate over decades.

Nobody has done it better for longer. And that’s why he’s worth about $110 billion, even after giving away tens of billions of dollars to charity.

So when Buffett’s firm makes moves, the rest of us tend to notice. Now, I do not advocate blindly copying what someone else does.

We all have different situations, goals, etc. But it can’t hurt to take a look at where Buffett’s capital is going, and whether or not that might make sense for you.

Today, I want to tell you about a financial stock that Buffett’s firm loaded up on in the first quarter of 2023.

Ready? Let’s dig in.

First, let’s be clear about what we’re talking about. Warren Buffett oversees a common stock portfolio worth over $300 billion for his conglomerate, Berkshire Hathaway (BRK.B). Berkshire Hathaway is the company he’s controlled as CEO for more than 50 years. While Buffett has two lieutenants – Todd Combs and Ted Weschler – assisting him with the portfolio, Buffett is still the CIO and main capital allocator by a long shot.

![]() That said, we can never be exactly sure who bought what. Just something to keep in mind.

That said, we can never be exactly sure who bought what. Just something to keep in mind.

So which financial stock has Warren Buffett’s firm recently been loading up on?

It’s Capital One Financial (COF).

Berkshire Hathaway opened up a new position in Capital One, picking up 9,922,000 shares.

This position is worth almost $1 billion. This position was opened during Q1 2023, and we know this after Buffett’s firm’s 13F filing just came out. The 13F filing covers all transactions for the prior quarter, and it generally gets released 45 days after quarter end.

The position isn’t super large by Berkshire Hathaway standards, but $1 billion is no small chunk of change.

Everything is relative. $1 billion for Berkshire Hathaway is almost a rounding error, but it would basically be unlimited money for the rest of us. Still, there’s value to be had here. And while it’s certainly possible, even likely, that Combs or Weschler was behind the move, Buffett’s own capital is at risk, regardless. That’s because as Berkshire Hathaway goes, so goes Buffett. He’s the largest single shareholder of Berkshire Hathaway. No matter who made the move, Berkshire Hathaway shareholders are impacted all the same.

Let’s talk about this business.

Capital One is a bank holding company that specializes in credit cards, auto loans, banking, and savings accounts. It has a market cap of $36 billion. While you might initially think of Capital One as a commercial bank, it’s mostly a credit card issuer. When looking at revenue for the most recent quarter – Q1 2023 – the Credit Card business segment generated seven times more revenue than the Commercial Banking business segment.

Capital One is a bank holding company that specializes in credit cards, auto loans, banking, and savings accounts. It has a market cap of $36 billion. While you might initially think of Capital One as a commercial bank, it’s mostly a credit card issuer. When looking at revenue for the most recent quarter – Q1 2023 – the Credit Card business segment generated seven times more revenue than the Commercial Banking business segment.

Credit cards? Classic Warren Buffett.

Why do I say that? Well, American Express (AXP) – is one of the oldest and largest positions in Berkshire Hathaway’s common stock portfolio, and there’s no doubt that Buffett was behind that one. American Express is, of course, a very large credit card issuer.

Buffett has long loved this business model. And why not?

It’s highly lucrative. Consider this: The average credit card interest rate in the US right now is nearly 24% – about as high as it’s ever been. Think about that for a second. 24%?! Imagine if you could make a 24% annual rate of return on your investments. You’d be a multimillionaire pretty quickly.

To put that in perspective, it’s higher than Buffett’s annualized rate of return over his legendary career.

That number is right about 20%. Now, it’s not an apples-to-apples comparison. Also, Capital One doesn’t make 24%/year on everything. Some balances get paid off before interest is applied. Some borrowers go into default. Etc. Still, it’s a fat pitch when it does come down the plate. You know what else is a fat pitch here? The low valuation.

This stock is uber-cheap.

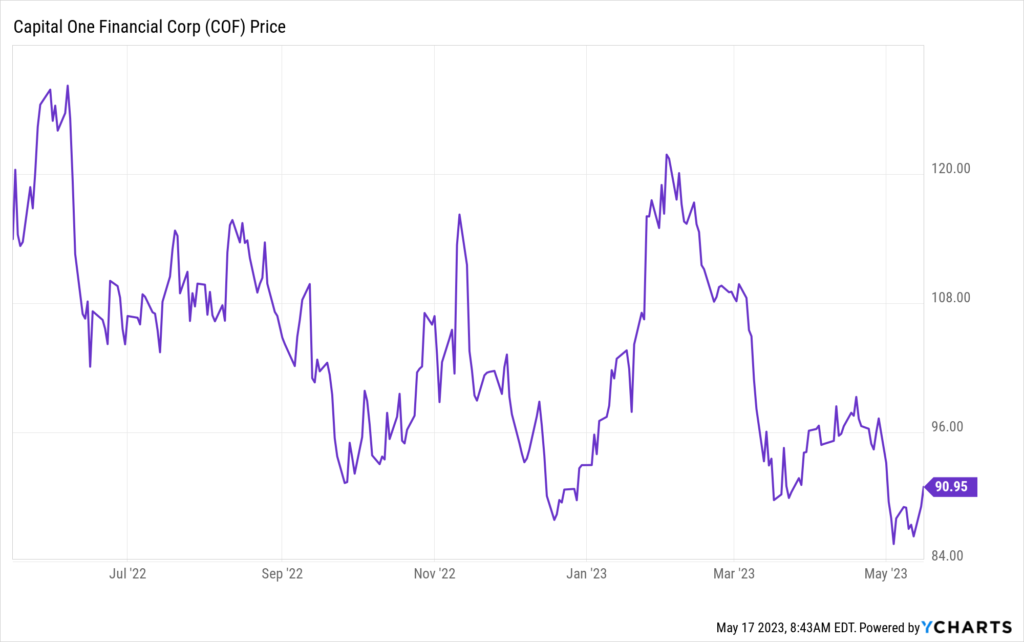

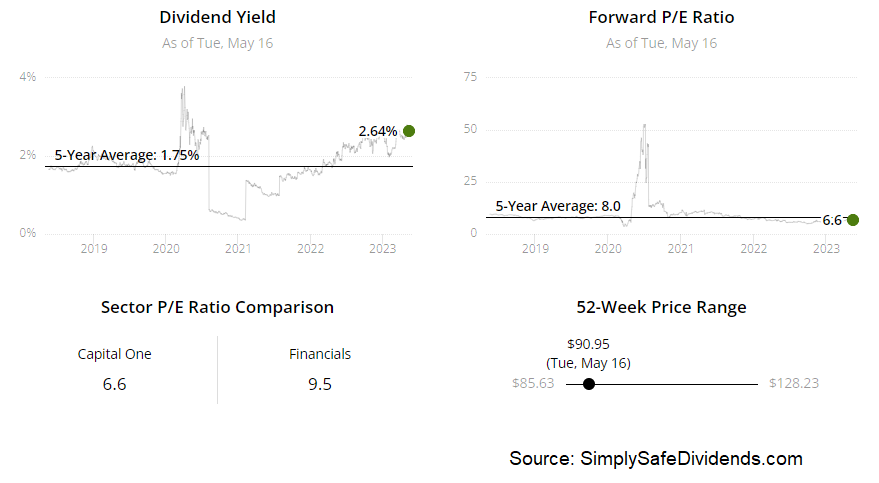

The stock’s stunning 30% drop from its 52-week high has created a noticeable amount of cheapness. Take the P/E ratio, for example. It’s 6.1. Single-digit P/E ratios are always going to catch one’s eye, but this is an especially eye-catching number – it’s closer to 5 than 10. Incredible.

The stock’s stunning 30% drop from its 52-week high has created a noticeable amount of cheapness. Take the P/E ratio, for example. It’s 6.1. Single-digit P/E ratios are always going to catch one’s eye, but this is an especially eye-catching number – it’s closer to 5 than 10. Incredible.

Since this is a bank holding company, another way to quickly get an idea of the valuation here is to use the P/B ratio. The stock’s own five-year average P/B ratio is 0.8, which is pretty low in and of itself. Yet it’s currently 0.6. Capital One is, quite frankly, priced for dismal business performance.

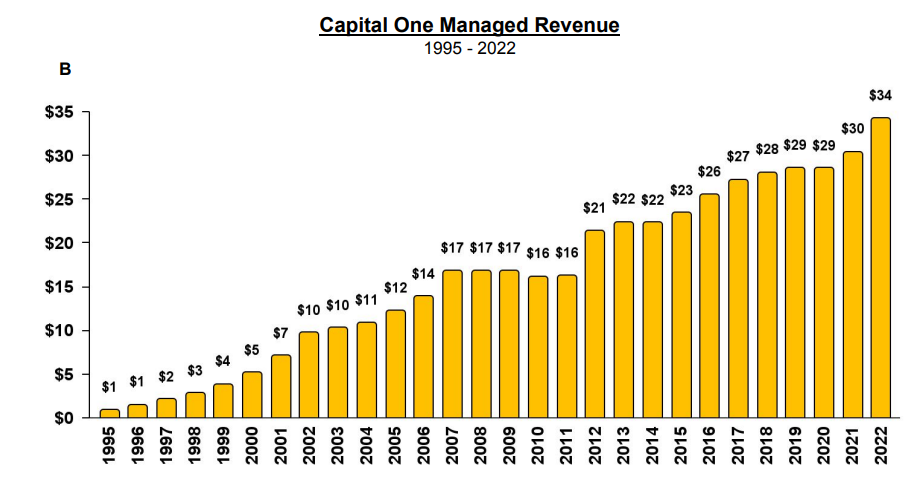

But the business hasn’t been performing dismally at all. Capital One was able to compound its revenue at an annual rate of 5.3% over the last decade. EPS sports a CAGR of 11.2% over that time frame. Pretty solid stuff, really. Not lighting the world on fire or anything. But relative to the valuation, which almost seems to imply there’s no growth at all, these are impressive numbers.

Huge buybacks have definitely helped to spur some of that excess bottom-line growth. What do we know about Buffett? He loves buybacks.

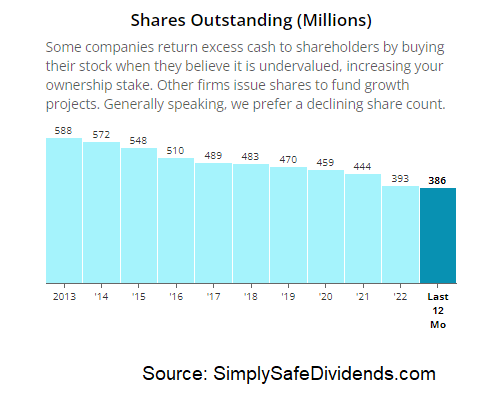

All else equal, it’s an effective way for a shareholder to gain more equity in a business without spending any more of their own capital. This is another box checked for Berkshire Hathaway, as Capital One has been a prolific repurchaser of its own shares. The company has just been cannibalizing itself. The outstanding share count is down by approximately 34% over the last 10 years. That is huge.

All else equal, it’s an effective way for a shareholder to gain more equity in a business without spending any more of their own capital. This is another box checked for Berkshire Hathaway, as Capital One has been a prolific repurchaser of its own shares. The company has just been cannibalizing itself. The outstanding share count is down by approximately 34% over the last 10 years. That is huge.

Of course, we invest in where a business is going, not where it’s been. The last 10 years have been great for Capital One, and the last few years were supercharged by so much free money sloshing around. However, the last year or so has unsurprisingly shown a reversal in some growth.

EPS for the most recent quarter came in nearly 24% lower YOY. But, while we don’t invest in the past, we also don’t invest for today. We’re investing for the long term. Concerning that, I don’t see Americans using less credit cards five or ten years from now, which sets up Capital One for a pretty bright future.

And you get paid a good-sized dividend along the way.

This is yet another way in which Capital One is classic Buffett. Buffett loves his dividends. While Berkshire Hathaway doesn’t pay a dividend, Buffett himself almost exclusively buys stocks that pay dividends -and not just dividends, but growing dividends. Gotta love being able to collect dividends, but then not pay them out. Sweet deal, right?

Capital One’s stock currently offers a 2.7% yield right now, which is 100 basis points higher than its own five-year average. The payout ratio is only 16.4%. That’s very low, and it provides a nice cushion in the face of economic softening.

Unfortunately, Capital One has been stingy with the dividend raises. The company has gone on long stretches without changing the size of the dividend. There just hasn’t been the consistent dividend raises that I, as a dividend growth investor, want to see.

Unfortunately, Capital One has been stingy with the dividend raises. The company has gone on long stretches without changing the size of the dividend. There just hasn’t been the consistent dividend raises that I, as a dividend growth investor, want to see.

Quite frankly, I wouldn’t be surprised if Buffett is disappointed with this, too, as he is pretty much a dividend growth investor himself. Based on that, along with the fact that the position is just under $1 billion, it does lead me to believe that Combs or Weschler made this move. Nonetheless, with all of that out of the way, the current $0.60/share quarterly dividend is twice as high as it was a decade ago. A doubled dividend is nothing to sneeze at.

One thing I don’t like about Capital One?

The unimpressive net charge-off rates, which tend to be higher than a lot of competing credit card issuers. I’ll give you numbers here. The net charge-off rate for April 2023 came in at 4.3% which rose from 4.2% in March.

This is actually pretty high when you look at all of the other banks and issuers. Take American Express, for example, which Berkshire Hathaway is heavily invested in. American Express came in with a 1.1% rate for April, which actually declined from the 1.7% reported in March. I’m just not a big fan of the credit quality here.

Should you follow Buffett and his team into Capital One? Well, that’s ultimately up to you.

However, there is a lot to like about the business. The extremely, extremely low valuation comes to mind very quickly, which builds in a nice margin of safety in the face of a potential upcoming recession. You also get a nice yield. And the buybacks are incredible.

However, the lack of consistent dividend raises is a black eye for me. And I’m leery of the charge-off rates. But it’s hard to deny the appeal of being invested alongside Warren Buffett. At the very least, it’d be a good idea to take a close look at Capital One here.

— Jason Fieber

P.S. Would you like to see my entire stock portfolio — the portfolio that’s generating enough safe and growing passive dividend income to fund my financial freedom? Want to get an alert every time I make a new stock purchase or sale? Get EXCLUSIVE access here.

Source: Dividends & Income