There are thousands of publicly-traded stocks in the US.

Many will likely turn out to be great long-term investments.

On the other hand, many will turn out terribly.

How should one go about separating the wheat from the chaff?

I’d argue that high-quality dividend growth stocks are the wheat.

These stocks represent equity in businesses paying reliable, rising dividends to their shareholders.

You can find hundreds of examples by perusing the Dividend Champions, Contenders, and Challengers list.

This list has carefully compiled invaluable information on US-listed stocks that have raised dividends each year for at least the last five consecutive years.

A lengthy track record of growing dividends acts as a quality filter.

After all, it requires growing profit in order to sustain a growing dividend.

And only great businesses can produce ever-more profit.

And only great businesses can produce ever-more profit.

It strikes me as common sense.

And I’ve implemented this approach myself, routinely investing my hard-earned cash into high-quality dividend growth stocks for more than a decade now.

This has allowed me to build the FIRE Fund.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

What’s especially nice about this is, I’m still fairly young.

In fact, I was able to quit my job and retire in my early 30s.

How?

My Early Retirement Blueprint explains.

Suffice it to say, following the common sense I just laid out has been crucial to my success.

But it’s not about just separating the wheat from the chaff in the quality sense.

But it’s not about just separating the wheat from the chaff in the quality sense.

It’s also about doing so in the valuation sense.

Whereas price is what you pay, value is what you end up getting.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Separating the wheat from chaff by buying undervalued high-quality dividend growth stocks sets up an investor for excellent results over the long run.

Now, this idea does assume that one understands the basics of valuation.

But it’s not difficult to forge this understanding for yourself.

My colleague Dave Van Knapp has made that a pretty straightforward process, via his Lesson 11: Valuation.

Part of an overarching series of “lessons” on dividend growth investing, it lays out a valuation system that can help you to ascertain an estimate of fair value for just about any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Linde PLC (LIN)

Linde PLC (LIN)

Linde PLC (LIN) is the world’s largest industrial gases company.

Founded in 1879, Linde is now a $156 billion (by market cap) gases giant that employs approximately 65,000 people.

The company reports results across the following geographic business segments: Americas, 39% of FY 2021 revenue; EMEA (Europe, Middle East, and Africa), 25%; APAC (Asia, Pacific), 20%; Linde Engineering, 9%; Global Other, 7%.

I love this business model for three key reasons.

First, industrial gases (like nitrogen and hydrogen) are critical input for the manufacturing processes of many different end products we all use every single day.

Think various electronics, for example.

Simply put, global manufacturing basically doesn’t work without this input.

That’s another way of saying our modern-day society ceases to exist without the gases.

Second, since reliable access to a constant source of these gases is a process requirement, a manufacturer will set up a long-term contract with a dependable provider.

A provider, like Linde, will then often install complex infrastructure on-site in order to ensure regular access to industrial gases, which makes it almost impossible for a manufacturer to switch providers at a later date.

Third, Linde is part of a global oligopoly – only three major companies in this space control almost all of global market share.

This is a dream setup, which is what perfectly positions Linde for continued growth across revenue, profit, and the dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

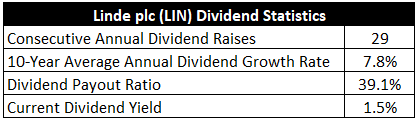

To date, the company has increased its dividend for 29 consecutive years.

Linde is a vaunted Dividend Aristocrat.

Linde is a vaunted Dividend Aristocrat.

The 10-year dividend growth rate is 7.8%, which is very good.

Better yet, there has been a noticeable acceleration in dividend growth of late.

For perspective on that, the most recent dividend raise came in at 10.4%.

That kind of double-digit dividend growth is really what you want to see here, as the stock’s lowish yield of 1.5% almost requires it.

Good news on that front: The payout ratio is only 39.1%, based on current fiscal year EPS guidance.

With that, there’s room for more low-double-digit dividend growth over the foreseeable future.

Now, the yield isn’t super compelling for income seekers, even though it is basically right in line with its own five-year average.

But Linde is a world-class compounder that can, and should, churn out significant wealth and dividend income over time.

For younger dividend growth investors who have a long-term vision, Linde offers a fantastic dividend package.

Revenue and Earnings Growth

As fantastic as that package might be, though, parts of it are based on the past.

However, investors must risk today’s capital for tomorrow’s rewards.

As such, I will now build out a forward-looking growth trajectory for the business, which will later aid in the valuation process.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I will then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast should give us the ability to reasonably judge where the business may be going from here.

Linde advanced its revenue from $11.2 billion in FY 2012 to $30.8 billion in FY 2021.

That’s a compound annual growth rate of 11.9%.

This looks outstanding on the surface.

But Linde merged with former rival Praxair in an all-stock transaction in late 2018.

So a lot of this top-line growth wasn’t totally organic.

Earnings per share grew from $5.61 to $10.69 (adjusted) over this period, which is a CAGR of 7.4%.

That number does factor in the big jump in the outstanding share count starting in FY 2019.

The thing is, we also have to take the bottom-line growth rate with a grain of salt.

That’s because we’re looking at a blend of a pre-merger growth rate and a post-merger growth rate.

The former was slower than the latter.

An acceleration in EPS growth has been playing out, which is why we see the aforementioned acceleration in dividend growth.

The company’s most recent quarterly earnings report – Q3 FY 2022 – showed 14% YOY adjusted EPS growth.

And the guidance in that report is calling for 12% to 13% YOY adjusted EPS growth for the full year.

Looking forward, CFRA is forecasting that Linde will compound its EPS at an annual rate of 12% over the next three years.

This is further evidence of that growth acceleration.

Seeing as how this lines up pretty well with Linde’s own projections, I’m inclined to strongly agree with CFRA’s number.

I think CFRA states it best with this: “We expect [Linde] to continue to hike prices and drive volume growth, resulting in sales growth of nearly 11% in 2022 and highsingle digits in 2023. Approximately 65% of [Linde’s] sales are from fixed fees or resilient end markets and most of [Linde’s] business has immediate cost pass-through clauses. A strong long-term growth outlook is supported by secular growth in electronics, healthcare, and clean energy.”

If that’s not enough to make you giddy about investing in Linde, I’m not sure what will.

But just in case the message isn’t coming through, CFRA adds this: “We think [Linde] is well-positioned to benefit from rapid growth that we anticipate in clean energy markets. [Linde] already has several significant applications that reduce, capture, sequester or clean, and monetize gas streams for use, such as [Linde’s] $1.3 billion carbon dioxide business. [Linde] is also a leader in the hydrogen supply chain, producing and supplying hydrogen to enable cleaner energy.”

Simply put, this is a remarkable business that has multiple ways in which to win and make a lot of money for shareholders.

Taking CFRA’s number as our near-term base case, Linde should easily be able to increase the dividend at a 10%+ annualized rate for at least the next few years.

That may very well settle into a high-single-digit range thereafter.

Either way, you’re looking at a high-grade compounding machine here.

And you’re starting off with a respectable yield while the machine makes you money.

Financial Position

Moving over to the balance sheet, Linde has an extremely strong financial position.

The long-term debt/equity ratio is 0.3, while the interest coverage ratio is north of 67.

Profitability is mixed, but the metrics have been sharply and steadily improving since FY 2019 (after the merger finalized).

Over the last five years, the firm has averaged annual net margin of 13% and annual return on equity of 11.8%.

It’s really hard to find anything to dislike here.

And the business does benefit from durable competitive advantages that include global economies of scale, high barriers to entry, switching costs, a global oligopoly, and long-term contracts backed by fixed infrastructure.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

The industry’s oligopoly does limit competition, however.

The business has cyclic traits, and a recession (which would reduce manufacturing activity) would almost certainly adversely affect Linde.

Linde’s involvement in large-scale energy projects around the world adds uncertainty from the fast-evolving nature of energy.

Input costs can be volatile, but pass-through clauses mitigate this issue.

Less than half of the company’s sales come from the Americas, which exposes the business to currency and geopolitical risks.

I see these risks as being really quite acceptable for such a high-quality business.

That’s especially after considering the valuation of the business, which looks decently attractive right now…

Stock Price Valuation

The forward P/E ratio is 27.5.

That’s based on adjusted EPS guidance for FY 2022.

I’d like to see it lower, but it’s not unreasonable at all for the growth profile.

We can also see that the P/CF ratio of 16.8 is modestly lower than its own five-year average of 17.3.

And the yield, as noted earlier, is just about in line with its own five-year average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 12% dividend growth rate for the next 10 years, and a long-term dividend growth rate of 8%.

The two-stage model is designed to account for Linde’s post-merger acceleration in bottom-line and dividend growth, which should moderate over time.

The initial stage of growth is not far off from Linde’s recent dividend raises.

It’s also right in line with CFRA’s near-term EPS growth projection for the firm.

And that projection is backed by Linde’s own near-term EPS growth guidance.

The payout ratio remains low, giving further flexibility to the dividend.

The long-term dividend growth rate I used is reserved for very high-quality businesses (like Linde).

It assumes a normalization of overall growth down the road, which I believe is likely.

The DDM analysis gives me a fair value of $354.36.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

While I wouldn’t say that Linde looks extremely cheap, it does appear to be modestly undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates LIN as a 3-star stock, with a fair value estimate of $347.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates LIN as a 4-star “BUY”, with a 12-month target price of $352.00.

We have a super tight consensus here, which is encouraging. Now, this stock jumped by almost 10% while I was in the middle of compiling data and putting this report together. That’s untimely. Still, averaging the three numbers out gives us a final valuation of $351.12, which would indicate the stock is possibly 7% undervalued.

Bottom line: Linde PLC (LIN) is a very high-quality business with many levers to pull in order to make money. Surprisingly, it’s only getting better, with improving profitability and accelerating growth being prime indicators of that. The stock did run up in the middle of my work, but it’s a terrific business to own for the long haul. With a market-like yield, an accelerating dividend growth rate, a low payout ratio, nearly 30 consecutive years of dividend increases, and the potential that shares are 7% undervalued, long-term dividend growth investors looking for a world-class compounder should definitely have this Dividend Aristocrat on their radar.

Bottom line: Linde PLC (LIN) is a very high-quality business with many levers to pull in order to make money. Surprisingly, it’s only getting better, with improving profitability and accelerating growth being prime indicators of that. The stock did run up in the middle of my work, but it’s a terrific business to own for the long haul. With a market-like yield, an accelerating dividend growth rate, a low payout ratio, nearly 30 consecutive years of dividend increases, and the potential that shares are 7% undervalued, long-term dividend growth investors looking for a world-class compounder should definitely have this Dividend Aristocrat on their radar.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is LIN’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 99. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, LIN’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income