Every day of every year offers a chance to increase your wealth and passive income. But the start of a new year is a particularly good time to look at investment ideas that could hold the potential to deliver better results than most other investment ideas available.

With this in mind, I’m going to reveal my Top 5 Stock Ideas for 2023!

Let’s say you have $5,000 that you’d like to spread across five different stocks. Well, you might want to take a good look at this list.

Now, keep in mind that I’m a long-term investor, and these are long-term investment ideas. I think all five stocks will do very well over the next 10+ years. And when I think about investing in these businesses, that’s the kind of time horizon I have in mind.

However, I think each stock is especially attractive at this point in time due to a variety of reasons that apply to each specific business, such as growth, valuation, yield, fundamentals, and competitive advantages.

As a result, I think they’ll do well over both the short term and long term.

That’s a win-win. I’ve personally invested in stocks just like these on my way to going from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint. If you’re interested, you can download a free copy of my Early Retirement Blueprint here.

If your aim is to build your wealth and passive income, become financially independent, and potentially even retire early in life, these stocks could help you do all of that.

Today, I want to tell you my Top 5 Stock Ideas for 2023.

Ready? Let’s dig in.

Before diving in, I want to tell you three important things about these five stocks.

First, they’re all dividend growth stocks.

Dividend growth stocks tend to outperform the broader market over the long run. It’s easy to understand why. Dividends aren’t simply a component of the market’s total return over the long term; dividends are the main component. And reinvesting growing dividends intensifies that effect.

Second, they’re all high-quality businesses.

Second, they’re all high-quality businesses.

It’s one thing to be a business. It’s quite another thing to be a wonderful business. A growing dividend can, and often does, serve as a great initial litmus test for business quality, indicating a certain level of wonderfulness.

That’s because only a strong business that’s producing growing profit can sustain a growing cash dividend for years on end. But it definitely isn’t the only thing to look for. To that point, every business I’m highlighting has brisk top-line and bottom-line growth, robust profitability, a rock-solid balance sheet, impressive dividend growth metrics, and numerous competitive advantages. The importance of business quality has never been more clear than right now. The last few years have shown us that only the strong survive.

Third, they all appear to be attractively valued.

Even the best stock in the world can be a poor investment, especially over a shorter period of time, if an investor pays far too much. But if one is able to invest in a great business at a great value, they’re setting themselves up for truly outstanding investment performance. That outstanding investment performance is possible over the short term, but it’s almost certain over the long term.

Now my Top 5 Stock Ideas for 2023.

Stock #1: CME Group (CME)

CME Group (CME) is a global markets company. Founded in 1898, CME Group now has a market cap of $62 billion. You’ve just gotta love the exchange companies.

They generate sky-high margins, as each exchange is a miniature monopoly. CME Group, for instance, has averaged annual net margin of 60% over the last five years. That’s outstanding. If you want to buy certain financial products, you must go to a particular exchange for that.

In the case of CME Group, it’s the world’s largest financial derivatives exchange. It’s the home of the VIX. It’s also the exclusive place to trade and clear S&P futures contracts. Exclusivity is a huge competitive advantage for every exchange, including CME Group.

This is a special business with some special perks. CME Group has compounded revenue at an annual rate of 5.5% and EPS at an annual rate of 11.7% over the last decade. Great businesses tend to compound at high rates like this, and that’s why their shares tend to compound investors’ wealth at high rates.

Indeed, this stock has more than quadrupled in price over the last decade. Great business performance is also what’s allowed for great dividend performance. The dividend has been increased for 12 consecutive years. The 10-year DGR is 9.2%. And the stock yields a comfortable 2.3%, which is 60 basis points higher than its own five-year average. The balanced payout ratio of 54.6% shows a healthy dividend.

If all of that weren’t enough, CME Group routinely declares special dividends. This year it was $4.50/share. Combined with the regular quarterly dividend, that brings up the stock’s yield to 5% at current pricing!

If all of that weren’t enough, CME Group routinely declares special dividends. This year it was $4.50/share. Combined with the regular quarterly dividend, that brings up the stock’s yield to 5% at current pricing!

This stock has had a rare bad year, and that’s why it could be set up so well for 2023 and beyond.

The stock is down by 24% in 2022. Slightly worse than the broader market. That’s rare. CME Group regularly outperforms. But what this has done is, it’s compressed the valuation and set the stock up even better on a go-forward basis.

The P/E ratio of 23.3 trails its own five-year average of 28.2. The P/CF ratio of 22.4 shows a similar disconnect when compared to its own five-year average of 27.5. I think this is a high-quality business with monopolistic attributes being sold at an attractive valuation. Morningstar has its fair value at $215/share. And you’re also getting a safe, growing dividend that even comes with an annual special dividend kicker. 2023 could be the year in which this name comes roaring back and outperforms once again.

Stock #2: Domino’s Pizza (DPZ)

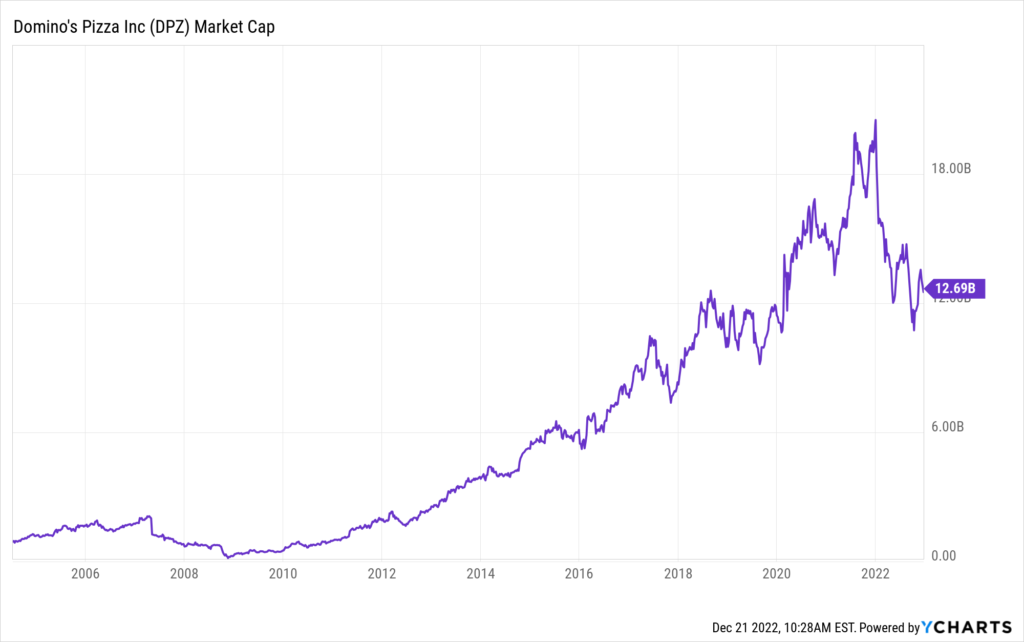

Domino’s (DPZ) is a multinational pizza restaurant chain. What a meteoric rise here. Founded in 1960 – only 62 years ago – Domino’s has become the world’s largest pizza company, with a market cap of $13 billion. Investing in pizza makes so much sense for so many reasons.

Selling pizza is a simple-to-understand business model. It easily passes Peter Lynch’s “crayon test”. Pizza is a classic food staple, and we all gotta eat. Moreover, since the odds of a recession are rising in 2023, Domino’s acts as a hedge against that. You can give up a lot in a recession. But not food. And since Domino’s offers easy-to-acquire food at a low price point, it should do well – even in a recession.

Selling pizza is a simple-to-understand business model. It easily passes Peter Lynch’s “crayon test”. Pizza is a classic food staple, and we all gotta eat. Moreover, since the odds of a recession are rising in 2023, Domino’s acts as a hedge against that. You can give up a lot in a recession. But not food. And since Domino’s offers easy-to-acquire food at a low price point, it should do well – even in a recession.

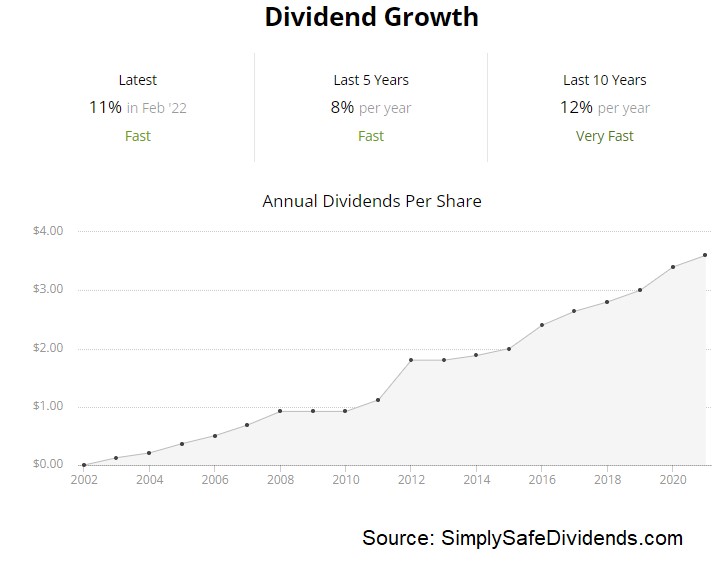

The growth here is off the charts. Revenue has a CAGR of 11.1% over the last decade. EPS has a CAGR of 24.3% over that period. Phenomenal. There’s so much excess bottom-line growth here because Domino’s has been prolific at buying back its own stock and improving its margins.

Those buybacks have been a good use of capital, seeing as how the stock is up by more than 700% over the last 10 years. The company was buying back at much cheaper prices. Also, all of this huge business growth has driven huge dividend growth – the dividend, which has been increased for 10 consecutive years, has a five-year DGR of 19.9%. And with a payout ratio of only 35.6%, the dividend growth is probably just getting started. The one bummer? The stock’s yield is only 1.2%. This is really more of a compounder than an income play.

No matter what happens in 2023, I’m confident that a lot of people will buy and eat pizza. Call me crazy, but I just think Domino’s is a no-brainer long-term investment. Of course, anything could happen in 2023 with the stock. That’s just how it is. But I’m highly confident that Domino’s, as a business, will continue to perform quite well.

People aren’t going to suddenly stop ordering and eating pizza. There’s a high degree of predictability here. That’s what’s so great about this business. And that predictability isn’t all that expensive, in my view. We put out a full analysis and valuation video on this business back in the summer, with the estimate for fair value coming out to right about $441/share. The business is currently trading hands for about $356/share. A lot of potential near-term upside here from one of the best compounders you’ll ever find.

Stock #3: Essex Property Trust (ESS)

Essex Property Trust (ESS) is a real estate investment trust that owns and operates a portfolio of US West Coast multifamily properties.

After being founded in 1971, Essex Property Trust has grown into a REIT with a market cap of $14 billion. Let’s talk about supply and demand for a moment. What’s great about Essex Property Trust is the inherent demand for what they offer.

We’re talking about housing here. It’s a basic need. And so there’s a base amount of demand in place already, which is advantageous. Further increasing demand is the fact that most of their property portfolio is located in California, which is a place that is geographically and economically attractive for a variety of reasons. Making things even more advantageous for Essex Property Trust is limited supply. That’s because California’s red tape and unique geographic features conspire to limit supply.

This is a world-class real estate operation. Revenue has a CAGR of 11.3% over the last 10 years, while FFO/share has compounded at an annual rate of 8.5% over that period. And that growth has been accelerating – the company’s Q2 report increased guidance on FFO/share YOY growth to 15.7%.

The occupancy rate is 96.1%. We have an investment-grade credit rating. What else do we have? Great dividend metrics. Essex Property Trust is a Dividend Aristocrat, with 28 consecutive years of dividend increases and a 10-year DGR of 7.2%. The stock offers a market-smashing 4.2% yield. And the payout ratio is 60.9%, based on midpoint guidance for this year’s FFO/share. That’s low for a REIT.

The occupancy rate is 96.1%. We have an investment-grade credit rating. What else do we have? Great dividend metrics. Essex Property Trust is a Dividend Aristocrat, with 28 consecutive years of dividend increases and a 10-year DGR of 7.2%. The stock offers a market-smashing 4.2% yield. And the payout ratio is 60.9%, based on midpoint guidance for this year’s FFO/share. That’s low for a REIT.

For years and years, this has been one of the best REITs money can buy.

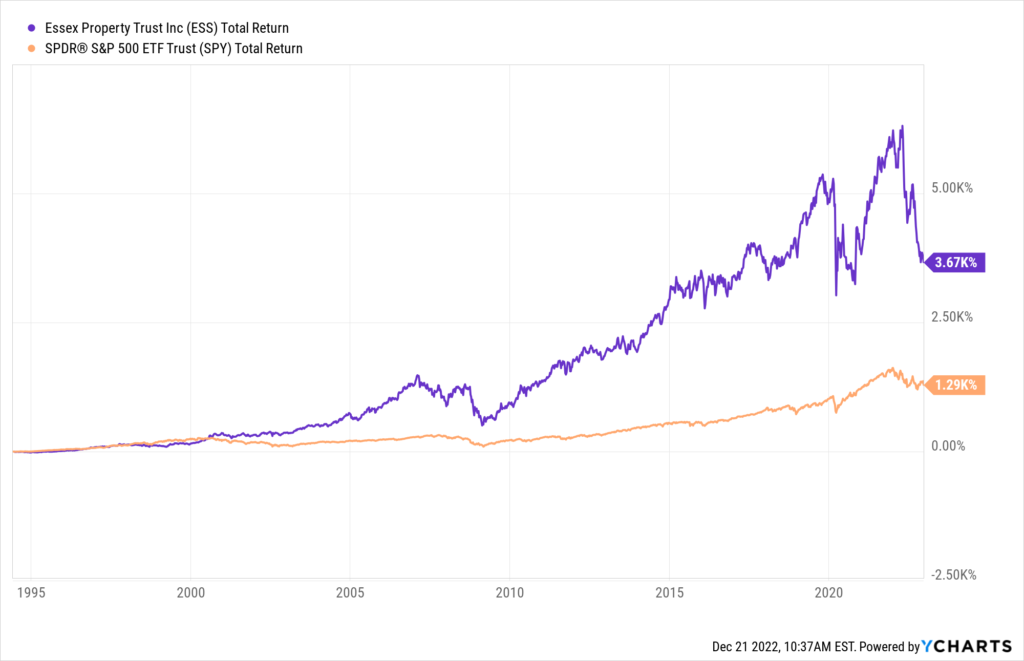

From its 1994 IPO through July 2022, the stock’s 5,123% total return blows away the 1,452% total return from the S&P 500. That’s the kind of stuff long-term investing dreams are made of. It’s what makes a lot of people very, very wealthy over time.

Despite that massive long-term outperformance, and despite the fact that rents are way up over the last few years, this stock is actually priced more than 30% lower than it was in early 2020 – before the pandemic hit. We put out an analysis and valuation video on this REIT about two months ago, showing why shares could be worth nearly $300/each. The stock is currently sitting at about $212.

Despite that massive long-term outperformance, and despite the fact that rents are way up over the last few years, this stock is actually priced more than 30% lower than it was in early 2020 – before the pandemic hit. We put out an analysis and valuation video on this REIT about two months ago, showing why shares could be worth nearly $300/each. The stock is currently sitting at about $212.

Huge upside potential and a huge dividend. This name could, and arguably should, shoot way higher in 2023.

Stock #4: L3Harris Technologies (LHX)

L3Harris Technologies (LHX) is a major American defense contractor. Founded in 1895, L3Harris Technologies now has a market cap of $39 billion. Not the biggest defense contractor out there. But it is one of the best.

Here’s the thing about defense contractors: They benefit from secular growth, largely because the need for sovereign security is eternal. Unfortunately, our species is a rather violent one. It’s been true since we were fighting with rocks. It’s true now that we’re fighting with bombs. And it’ll be true 100 years from now, let alone the next year.

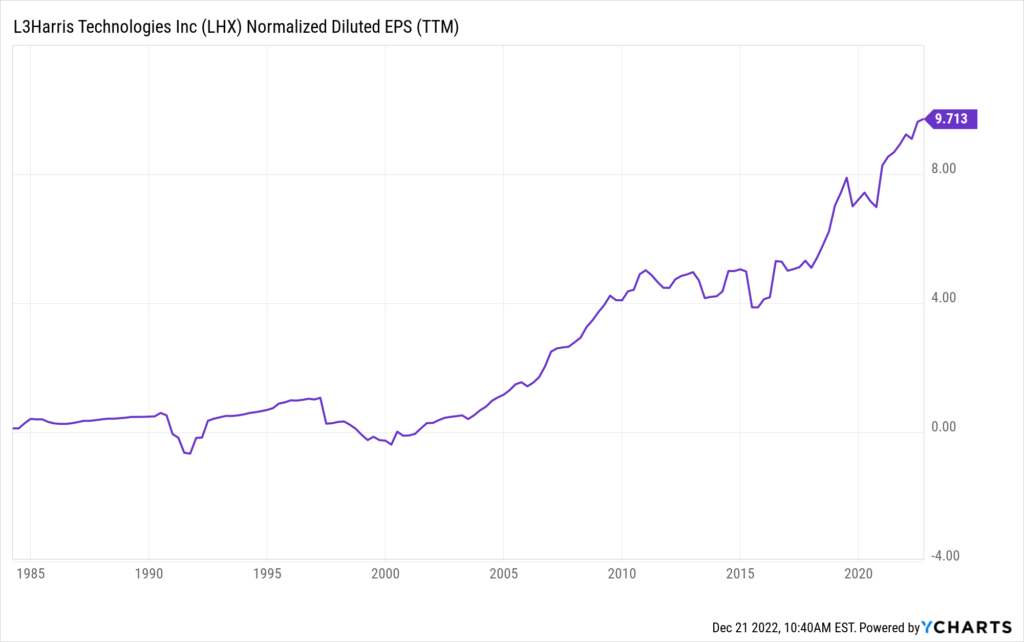

L3Harris Technologies flies under the radar (pun intended). But it really shouldn’t. Because L3Harris Technologies is the result of an all-stock merger between Harris Corporation and L3 Technologies back in 2019, the numbers are messy.

Revenue jumped in a big, non-organic way from the larger combined sales base. However, growth on a per-share basis looks good – EPS has compounded at 7.5% annually since FY 2019. And the company’s growth profile could get a boost (again, pun intended) from the planned acquisition of Aerojet Rocketdyne Holdings (AJRD) – for $4.7 billion.

In addition, the dividend has been increased for 21 consecutive years, surviving the merger. The 10-year DGR is 12.8%, which is better than some well-known defense players. The stock’s yield of 2.2% is 50 basis points higher than its own five-year average. And the payout ratio is only 34.8%, based on midpoint guidance for this year’s adjusted EPS.

In addition, the dividend has been increased for 21 consecutive years, surviving the merger. The 10-year DGR is 12.8%, which is better than some well-known defense players. The stock’s yield of 2.2% is 50 basis points higher than its own five-year average. And the payout ratio is only 34.8%, based on midpoint guidance for this year’s adjusted EPS.

What really sets up L3Harris Technologies so well for 2023 is relative underperformance in 2022. Defense names did well this year. Lockheed Martin (LMT) – was one of my top picks for 2022. Well, that stock rose by 36% in 2022, as I write this near the end of the year.

Compared to the S&P 500, that’s significant outperformance. LHX, however, is down by about 3% this year. Better than the market. But worse than many peers. And that underperformance relative to peers is why I think 2023 could be the year for catching up.

Most basic valuation metrics here trail their own respective recent historical averages. The forward P/E ratio, based on that guidance, is 16. The P/CF ratio of 18.2 is well off of its own five-year average of 22.4. The stock’s price is about $205. CFRA’s 12-month target price is $263. The geopolitical landscape is still very hot. And I think L3Harris Technologies could heat up in 2023.

Stock #5: Medtronic (MDT)

Medtronic (MDT) is a global developer and manufacturer of medical devices for chronic diseases. Founded in 1949, Medtronic has grown into a company with a market cap of $ 103 billion. Here’s another business with secular growth. The price of oil? War in Europe? The US dollar?

None of that will have anything to do with someone’s need for healthcare, in general, or Medtronic’s products, specifically. If you need heart surgery, you need heart surgery. Nothing else really matters in that moment. Not even the price of Medtronic’s products. The dynamics here are super favorable.

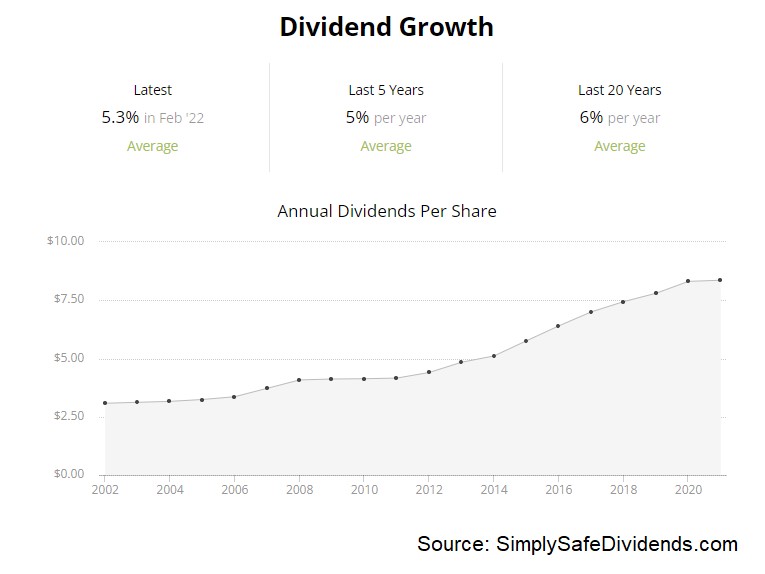

Also super favorable? The dividend metrics. This is a vaunted Dividend Aristocrat, with 45 consecutive years of dividend increases. The 10-year DGR is 10.3%. And you’re pairing that double-digit dividend growth with the stock’s current yield of 3.5%.

With the payout ratio at only 51.6%, based on midpoint guidance for this fiscal year’s adjusted EPS, this dividend looks easily covered and positioned for more increases ahead. All of this dividend growth has a foundation built on business growth. Medtronic has compounded its revenue at an annual rate of 7.5% and its EPS at an annual rate of 5.7% over the last decade. The company has a rock-solid financial position. And net margin is routinely in the double digits.

This stock has had a miserable 2022. That’s partially why I’m selecting it as a top idea for 2023. As I write this, Medtronic’s stock is down by 27% in 2022. That’s surprising. The stock didn’t look all that expensive at the start.

It’s one thing to have a 30% drop when you’re overpriced by 40%. It’s quite another thing to drop so much when the valuation wasn’t all that crazy to begin with. I believe this has created a coiled spring. And as the supply and demand shocks fade for Medtronic, the quality of the business will shine through. And that should cause the stock to viciously uncoil, with price reaching for value.

It’s one thing to have a 30% drop when you’re overpriced by 40%. It’s quite another thing to drop so much when the valuation wasn’t all that crazy to begin with. I believe this has created a coiled spring. And as the supply and demand shocks fade for Medtronic, the quality of the business will shine through. And that should cause the stock to viciously uncoil, with price reaching for value.

Speaking of that, we covered Medtronic’s business not long ago, estimating fair value for the firm at about $111/share. With Medtronic selling for $77/share, it looks materially undervalued to me. Meanwhile, you get a market-smashing yield from a Dividend Aristocrat while you let 2023 play out.

— Jason Fieber

Imagine having 12 new monthly income checks, carrying the potential of up to 21% yields.This is possible because of a tested strategy to get paid out regularly, like a paycheck. For over a decade, I have helped more than 26,000 investors secure 12 new monthly payouts. Meaning, you know exactly how much you'll make every month... Because of some stocks that pay us 8%,13.4%, and even 21.6% yields. See it for yourself here.

Source: Dividends & Income