I’ve been hearing quite a bit about how this is one of the worst years ever for the stock market.

2022 is up there with the Great Depression, the dot-com bust, and the Global Financial Crisis. But guess what? Each of those three periods were amazing buying opportunities for long-term investors.

If you bought a lot of stock in, say, 2002 or 2009, you’re likely doing quite well for yourself these days. In both of those years, you were able to pick up shares left and right for deep, deep discounts.

That’s because everyone else was fearful, leading to these discounts. You have to be willing to buy when there’s blood in the streets. That’s how you get lower valuations, higher yields, greater-long term total return prospects, and reduced risk.

As a consistent asset accumulator and buyer of stocks, if 2022 is in the same company as 2002 or 2009, count me in.

I always see short-term volatility as a long-term opportunity. That perspective helped me to go from below broke at age 27 to financially free at 33.

By the way, I explain exactly how I achieved financial freedom in just six years in my Early Retirement Blueprint. As much as 2022 might be a great time to buy, though, not every business and not every stock is the same.

Focusing on the very best long-term ideas right now is what this article is all about. Today, I want to tell you my top 5 dividend growth stocks for November 2022.

Ready? Let’s dig in.

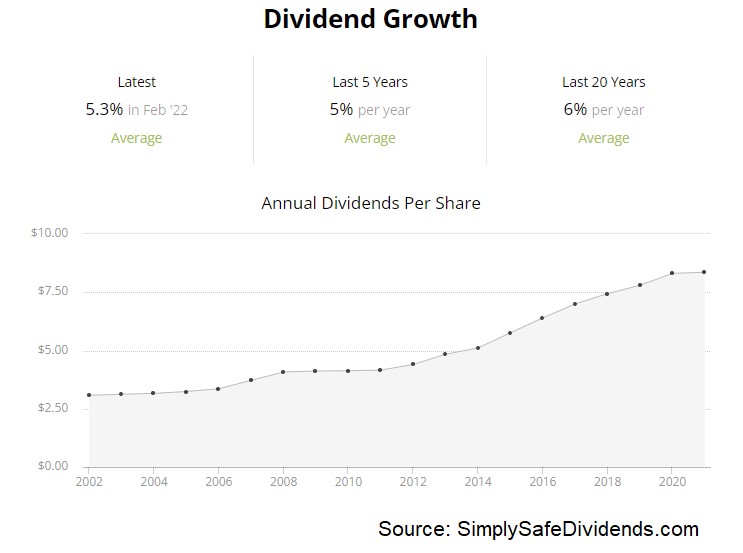

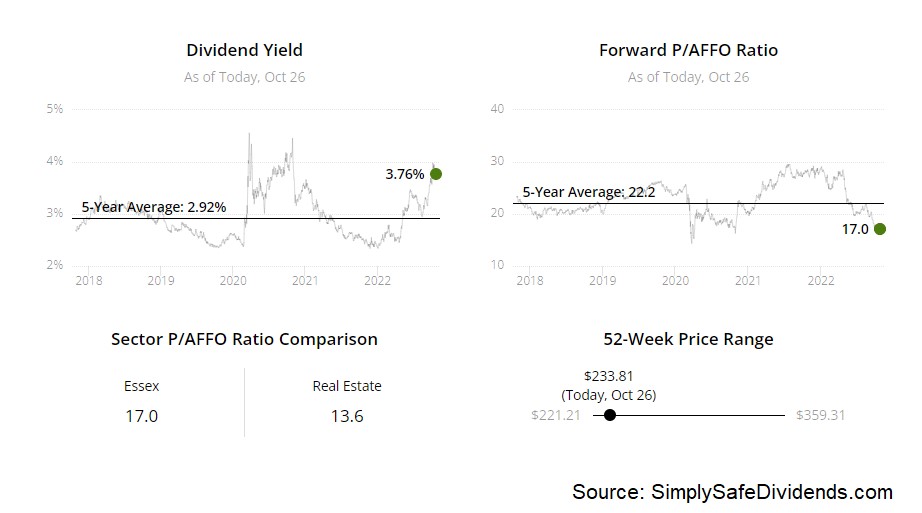

My first dividend growth stock pick for November 2022 is Essex Property Trust Inc. (ESS).

Essex Property Trust is a real estate investment trust that owns and operates a portfolio of US West Coast multifamily properties.

I love real estate. One of the reasons why is its flexibility. There are so many different applications for real estate. One of the most attractive applications is housing. After all, we all need somewhere to live. While a lot of real estate is fairly discretionary, like shopping malls and storage facilities, housing is not. Shelter is a basic need.

What Essex Property Trust does is build on this basic need and supercharges it with exposure to supply-constrained markets. When supply is constrained and demand is high, that plays right into their hands. Indeed, revenue has compounded at an annual rate of 11.3% over the last decade, while FFO/share has compounded at an annual rate of 8.5% over that time frame.

Unsurprisingly, all of this business growth has led to plenty of dividend growth.

The REIT has increased its dividend for 28 consecutive years, cementing their status as a vaunted Dividend Aristocrat. One of the very few Dividend Aristocrats that’s a REIT, by the way. The 10-year DGR of 7.2% is quite solid, in and of itself. But it’s made to look even more solid when you consider the stock’s starting yield of 3.9%.

Pairing a near-4% yield with that kind of dividend growth rate, on a Dividend Aristocrat, is almost unheard of. With a payout ratio of just 60.9%, based on midpoint guidance for this year’s FFO/share, this large, growing dividend looks safe.

Pairing a near-4% yield with that kind of dividend growth rate, on a Dividend Aristocrat, is almost unheard of. With a payout ratio of just 60.9%, based on midpoint guidance for this year’s FFO/share, this large, growing dividend looks safe.

Basic need. Big dividend. And an attractive valuation. The one thing that would often keep long-term dividend growth investors away from Essex Property Trust was its valuation. It’s the kind of stock that usually gets a premium multiple. But not now. The forward P/FFO ratio is a lowly 15.7, based on guidance.

Since that’s analogous to a P/E ratio on a normal stock, we can see just how discounted this name has become. We will be putting out a full analysis and valuation video on the REIT very soon, if it hasn’t already gone live by now. Our video will show why this business could be worth almost $300/share. With the stock priced below the $230 mark, I think we have a lot of upside on this high-quality Dividend Aristocrat.

Since that’s analogous to a P/E ratio on a normal stock, we can see just how discounted this name has become. We will be putting out a full analysis and valuation video on the REIT very soon, if it hasn’t already gone live by now. Our video will show why this business could be worth almost $300/share. With the stock priced below the $230 mark, I think we have a lot of upside on this high-quality Dividend Aristocrat.

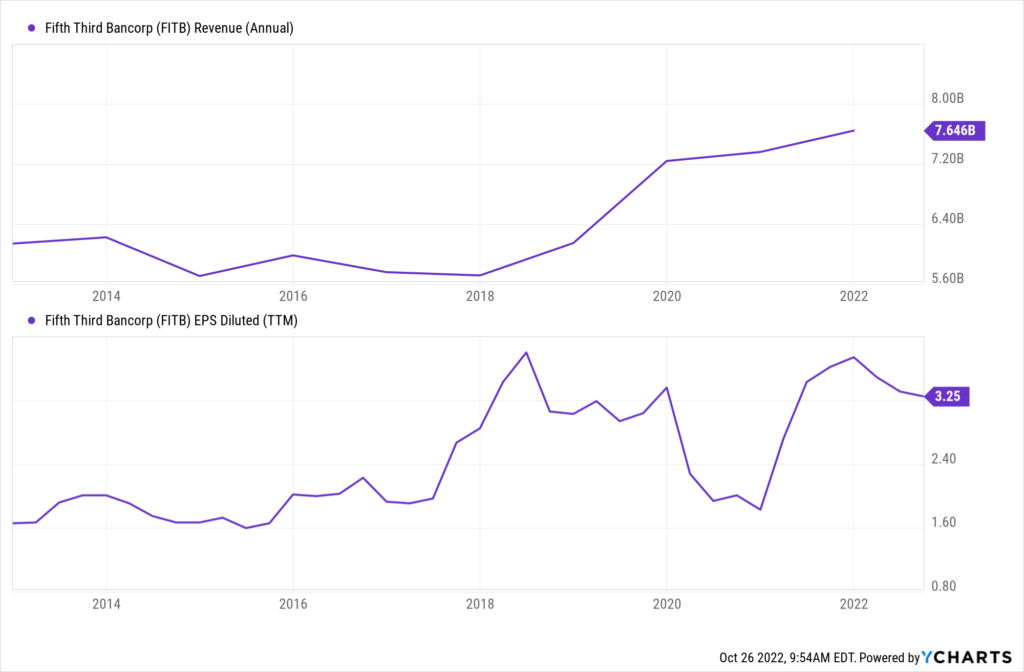

My second dividend growth stock pick for November 2022 is Fifth Third Bancorp (FITB).

Fifth Third is a diversified regional bank holding company.

Warren Buffett loves banks. I love banks. And maybe you should love banks. Why? Well, the banking business model is great. Banks are literally in the business of money. This is a business model that’s been around since antiquity. It’s so enduring because it’s so necessary – our society and economy depends on the proper flow of capital, and banks are integral to this flow. Thus, being one of the largest banks in the world’s largest economy bodes pretty well for Fifth Third. That’s why Fifth Third sports a 2.5% CAGR for revenue and a 9.4% CAGR for EPS over the last challenging decade.

It’s also why the bank sports a great dividend growth track record. Fifth Third has increased its dividend for 12 consecutive years. In fact, they just increased their dividend yet again in September by 10%. The 10-year DGR is 14.1%, so we can clearly see the double-digit dividend growth rate continuing.

It’s also why the bank sports a great dividend growth track record. Fifth Third has increased its dividend for 12 consecutive years. In fact, they just increased their dividend yet again in September by 10%. The 10-year DGR is 14.1%, so we can clearly see the double-digit dividend growth rate continuing.

On top of that double-digit dividend growth, the stock yields a mouth-watering 4%. How can anyone be displeased with this kind of combination of yield and growth? Even after this increase in the dividend, the payout ratio remains a comfortable 40%.

After dropping 35%, the stock looks cheap. The P/E ratio of 10.2 is well below the broader market’s earnings multiple. Now, banks like this one typically command low earnings multiples. But even by Fifth Third’s standards, this is unusually undemanding.

For perspective on that, the stock’s own five-year average P/E ratio is 10.6. And that aforementioned 4% yield is 90 basis points higher than its own recent historical average. There’s a disconnect here, which could be advantageous for long-term dividend growth investors.

We’ll soon have a full analysis and valuation video coming out on this bank, showing why it may just be one of the best investment opportunities in the market. Keep an eye out for that video on our YouTube channel, and keep this stock on your radar.

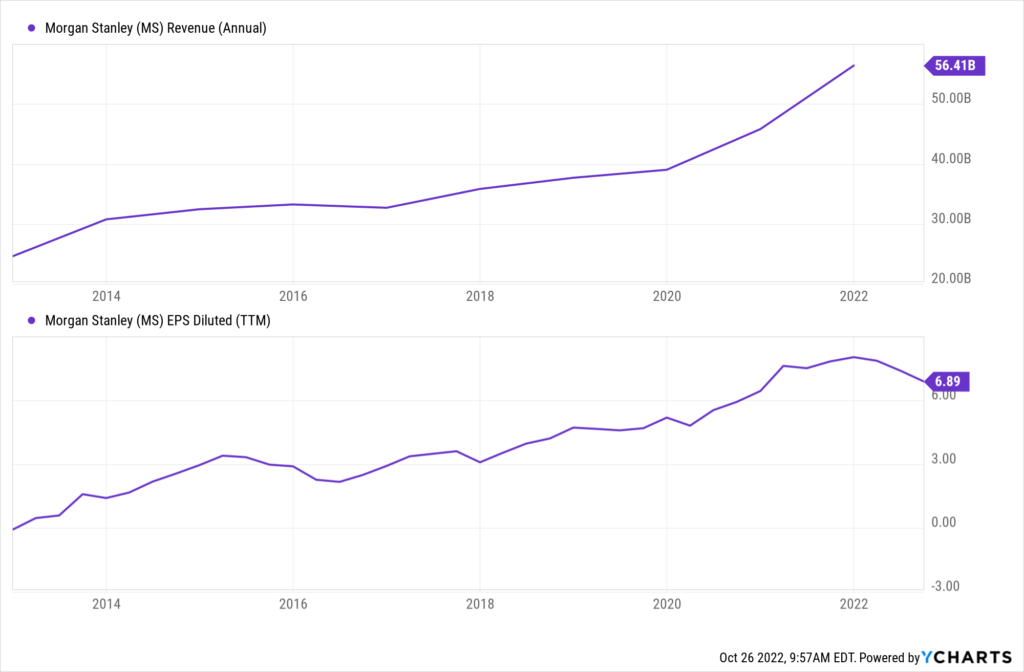

My third dividend growth stock pick for November 2022 is Morgan Stanley (MS).

Morgan Stanley is a multinational investment bank and financial services company. This is a global financial powerhouse, with two major pillars – investment banking, and wealth management.

This powerful one-two punch has been carefully crafted under the auspices of CEO James Gorman. And it has led to the prominent rise of Morgan Stanley into one of the world’s foremost financial institutions. It’s also led to a 9.7% CAGR for revenue and a 21.8% CAGR for EPS over the last decade.

What else has this led to? Great dividend growth. The company has increased its dividend for nine consecutive years, with a five-year DGR of 28.5%. Wow. Plus, the stock yields 3.9%. These are exceptional numbers that you tend to only see during periods of extreme market volatility, like we have in 2022.

What else has this led to? Great dividend growth. The company has increased its dividend for nine consecutive years, with a five-year DGR of 28.5%. Wow. Plus, the stock yields 3.9%. These are exceptional numbers that you tend to only see during periods of extreme market volatility, like we have in 2022.

Otherwise, you rarely see high yields and high dividend growth rates like this, because the market will bid up that growth and push the yield down during normal periods. Also, more good news here. The payout ratio is 41.9%, indicating plenty of leeway for more sizable dividend increases in the future.

Otherwise, you rarely see high yields and high dividend growth rates like this, because the market will bid up that growth and push the yield down during normal periods. Also, more good news here. The payout ratio is 41.9%, indicating plenty of leeway for more sizable dividend increases in the future.

Financials, in general, look cheap. Morgan Stanley is no exception. While Morgan Stanley isn’t the cheapest stock in the world, or even the cheapest financial I’ve seen, I fail to see any basic valuation metric as being onerous. The P/E ratio of 11.5 is “Exhibit A”. The P/B ratio of 1.4 is “Exhibit B”. These are not challenging numbers. And this is while Morgan Stanley isn’t running at full steam.

When earnings recover, these multiples will look silly. Our recent video on Morgan Stanley analyzed the business and estimated intrinsic value for the firm at just under $100/share. Shares are currently trading hands for $80/each. I think we have a big discrepancy between price and value, and now would be a good time to consider taking advantage of that.

My fourth dividend growth stock pick for November 2022 is Prudential Financial (PRU).

Prudential Financial is a global, diversified insurance company. Boy, I love insurance. You can generally make a bit of money by charging more in premiums than you pay out in claims. And if you’re underwriting properly, you should be able to do that.

However, the insurance business model really butters my bread because of the float – the low-cost capital that accrues as a result of a severe time lag between taking premiums in and seeing cash leave the door on claims. Many insurance companies make far more from the float than core underwriting.

On top of this, Prudential Financial also runs a substantial asset management business, which earns the firm sizable, recurring fees. Although revenue is messy because of one-time issues, the company has logged a tremendous 38.4% CAGR in its EPS over the last decade.

For income-oriented dividend growth investors, this name has to be on your radar. I say that because the stock offers a 4.8% yield. You just don’t see that kind of yield every day, even in this rising-rate environment. And this is a safe, growing dividend.

The company has increased its dividend for 14 consecutive years, with a 10-year DGR of 12.5%. Regarding safety, the payout ratio is 40.4%, based on TTM adjusted EPS. So the company has plenty of headroom here.

Prudential’s logo is the Rock of Gibraltar. That befits this rock-solid company. Better yet, it looks undervalued. The fundamentals right across the board are just solid. Prudential Financial might not “wow” me in any one area of the business. Instead, it’s the whole package.

Prudential’s logo is the Rock of Gibraltar. That befits this rock-solid company. Better yet, it looks undervalued. The fundamentals right across the board are just solid. Prudential Financial might not “wow” me in any one area of the business. Instead, it’s the whole package.

Part of that package is the valuation, which looks appealing right now. The stock’s P/E ratio is below 8, based on TTM adjusted EPS. The market has priced in very low expectations for Prudential Financial. We just put out a full analysis and valuation video on Prudential Financial, showing why the business could be worth $102.60 per share. I think you could do a lot worse than investing in this rock-solid company with a big dividend, especially at this valuation.

My fifth dividend growth stock pick for November 2022 is Williams-Sonoma (WSM).

Williams-Sonoma is a multi-channel retailer of high-quality home products and furnishings. This company hasn’t just survived but thrived in a very challenging period for legacy retailers. I believe it comes down to two factors: their differentiation, and their coherent omnichannel strategy.

Regarding that latter point, Williams-Sonoma has been way ahead of the curve on the e-commerce front; more than 65% of net revenues and profits in FY 2021 came about from the company’s e-commerce channel. Impressive. You know what else is impressive? The growth. Williams-Sonoma has posted up an 8.3% CAGR for revenue and a 21.4% CAGR for EPS over the last decade.

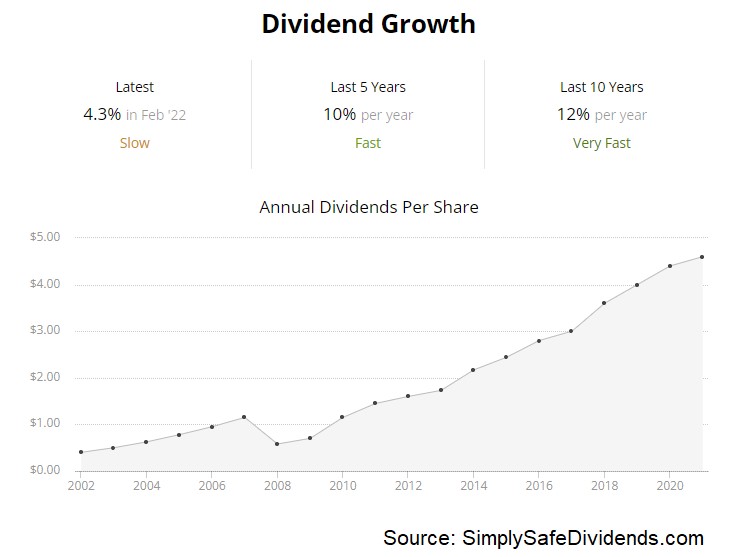

Another impressive aspect here is the dividend growth. The company has increased its dividend for 16 consecutive years. And these aren’t small dividend increases, either. The 10-year DGR is 13.6%. Along with that double-digit dividend growth rate, the stock yields a market-beating 2.7%.

What might be the best thing here about the dividend is the low payout ratio of only 19.5%. In the face of a tough housing market, the dividend is positioned ultra cautiously. I really like that.

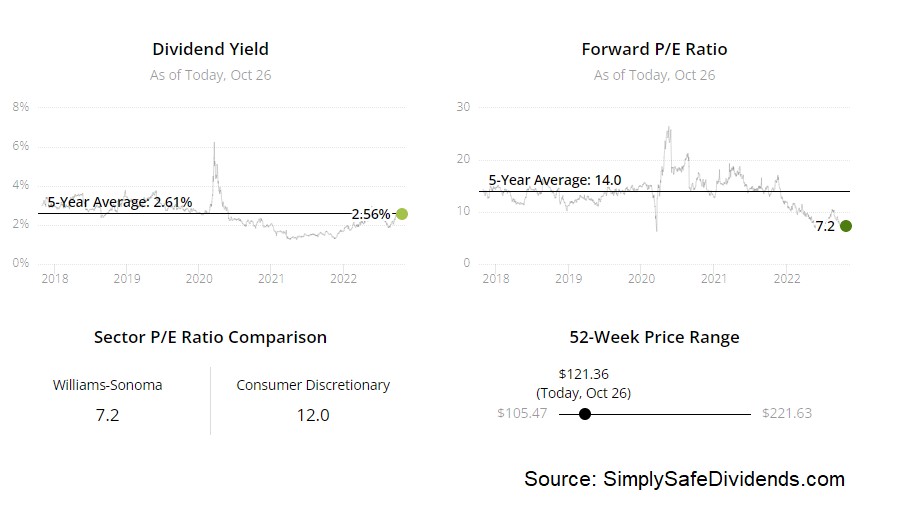

I also really like the valuation. The P/E ratio is a laughable 7.3. That’s low in and of itself, but it’s crazy low against a company that’s grown like Williams-Sonoma has. We’re talking about a PEG ratio of about 0.3. Insane.

Now, the last couple of years have been a bonanza for the company. And we just don’t know how secure the E in the P/E ratio is. The jury’s out on how much, if any, EPS will contract in the near term. Regardless, there’s a lot of cushion here. A big drop in earnings has already been priced in.

Now, the last couple of years have been a bonanza for the company. And we just don’t know how secure the E in the P/E ratio is. The jury’s out on how much, if any, EPS will contract in the near term. Regardless, there’s a lot of cushion here. A big drop in earnings has already been priced in.

Indeed, our recent video on Williams-Sonoma, which analyzes and values the business, estimated fair value at almost $178/share. This is one of America’s premier retailers. And it looks very compelling right now. Don’t forget about it.

— Jason Fieber

Motley Fool Stock Advisor's average stock pick is up over 350%*, beating the market by an incredible 4-1 margin. Here’s what you get if you join up with us today: Two new stock recommendations each month. A short list of Best Buys Now. Stocks we feel present the most timely buying opportunity, so you know what to focus on today. There's so much more, including a membership-fee-back guarantee. New members can join today for only $99/year.

Source: Dividends & Income