“Be greedy when others are fearful.”

Taken from a longer sentence about being opportunistic, it’s become enshrined as one of Warren Buffett’s best quotes. But how do you know when the fear is thick? How do you quantify that?

Well, CNN has what they call a Fear & Greed Index. The Index is currently showing 25, which is in “Extreme Fear” territory. And based on what I’m seeing in the market, that sounds about right.

Of course, being greedy when others are fearful is a hard thing to do. Otherwise, everyone would be doing it. And there wouldn’t be any fear to take advantage of.

So what makes it easier to be greedy right now? The dividend growth investing strategy.

When you’re buying and holding high-quality dividend growth stocks, big drops in the market are great.

You still see your dividend income flow and grow like clockwork. And when the income – the core – is holding up strong, you can be strong.

Meanwhile, you’re able to reinvest that growing dividend income – along with any other capital you have – into cheaper dividend growth stocks offering higher yields, greater long-term total return prospects, and reduced risk.

All of this serves you and gets you to financial freedom that much faster.

Today, I want to tell you about 5 dividend growth stocks that are down more than 30% from their recent highs.

Ready? Let’s dig in.

The first stock I want to talk about today is Alexandria Real Estate Equities (ARE).

Alexandria Real Estate is a life sciences real estate investment trust with a market cap of $22 billion. This is such an interesting and unique REIT. Alexandria Real Estate is an owner, operator, and developer that is focused on life science, AgTech, and technology campuses located in innovation clusters across key markets like San Diego and Boston.

While I think Alexandria Real Estate sometimes gets lumped in with office building REITs, this company actually owns specialized laboratories that are used for high-tech R&D purposes. You can’t do this kind of work in your pajamas out of your extra bedroom at home. This is what protects the REIT and gives it the ability to continue growing its revenue, profit, and dividend.

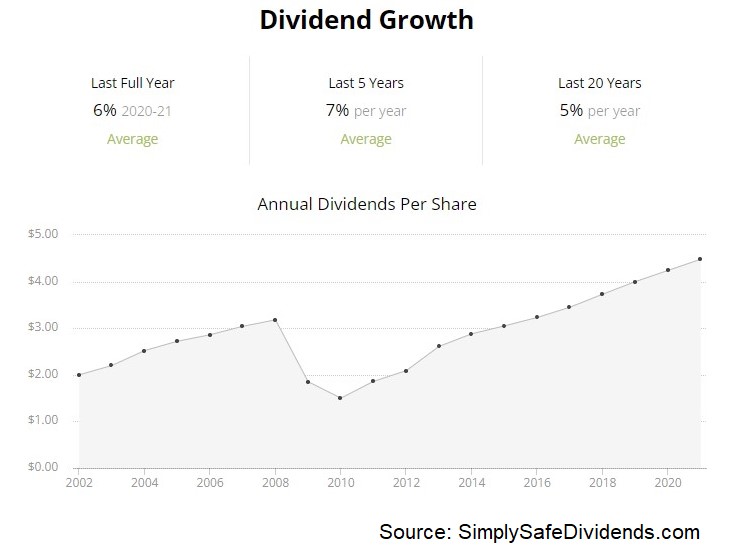

The REIT has increased its dividend for 12 consecutive years. Alexandria Real Estate sports some great dividend metrics. We’re right in the sweet spot here.

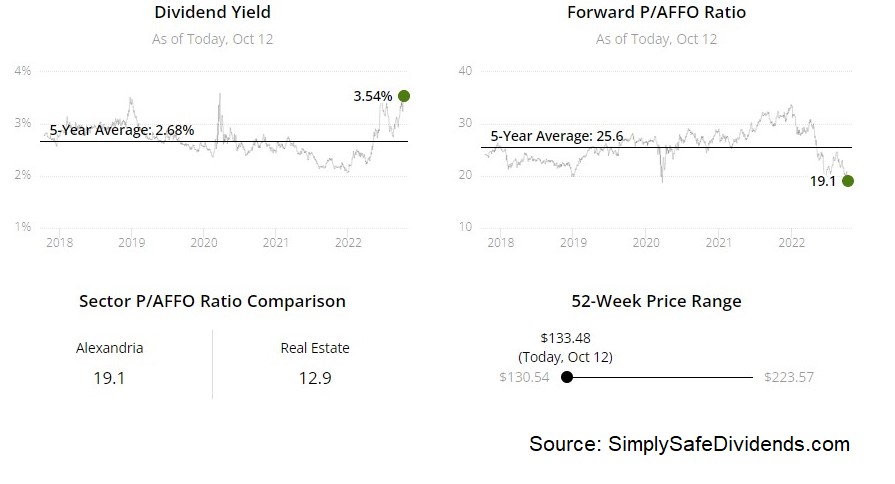

The stock yields 3.5%, which beats what the broader market gives you. And the 10-year DGR is 8.9%, which beats inflation. Getting back to the yield for a moment, this 3.5% yield is 90 basis points higher than its own five-year average.

The stock yields 3.5%, which beats what the broader market gives you. And the 10-year DGR is 8.9%, which beats inflation. Getting back to the yield for a moment, this 3.5% yield is 90 basis points higher than its own five-year average.

This is not a stock that typically offers this kind of yield. Yet, with a payout ratio of only 56.1%, based on midpoint guidance for this fiscal year’s AFFO/share, this big dividend is easily covered. This is actually a super low payout ratio for a REIT.

I think this stock is very buyable after its 40% – yes, 40% – drop.

In fact, I find it to be so buyable, I’m personally buying it. And I covered why I’m so enamored with this REIT in a recent video.

Look, at the stock’s 52-week high of $224.95, it definitely wasn’t on my radar. Nothing about it was interesting at that level. But down here, at $135? Nearly $100/share cheaper? I think it’s extremely interesting. The P/CF ratio of 19.4 is significantly lower than its own five-year average of 25.7.

Look, at the stock’s 52-week high of $224.95, it definitely wasn’t on my radar. Nothing about it was interesting at that level. But down here, at $135? Nearly $100/share cheaper? I think it’s extremely interesting. The P/CF ratio of 19.4 is significantly lower than its own five-year average of 25.7.

We’re not just lower than pre-pandemic pricing here – this was a $175 stock in early 2020. No, we’re back to pricing from 2017, despite the REIT growing its profit and dividend quite dramatically since then. Take a good look at this name, if you haven’t already.

The second stock I should go over today is Comcast Corporation (CMCSA).

Comcast is a media and entertainment conglomerate with a market cap of $129 billion. Here’s the thing with Comcast: The narrative is very different than the reality.

What’s the narrative?

Comcast is a dying company, with cord-cutting acting as death by a thousand cuts. What’s the reality? Comcast is a growing company, with both revenue and EPS up meaningfully over the last decade. How can this be so?

Well, it’s because Comcast isn’t just a cable TV company. It’s a diversified conglomerate. Its broadband arm, for instance, has been more than making up for the cable TV losses, as high-speed Internet access is becoming almost as necessary as electricity access. Meaningful revenue and EPS growth have led to – you guessed it – meaningful dividend growth.

Well, it’s because Comcast isn’t just a cable TV company. It’s a diversified conglomerate. Its broadband arm, for instance, has been more than making up for the cable TV losses, as high-speed Internet access is becoming almost as necessary as electricity access. Meaningful revenue and EPS growth have led to – you guessed it – meaningful dividend growth.

The conglomerate has increased its dividend for 14 consecutive years. A 10-year DGR of 11.9% and a yield of 3.7% is an awfully compelling combination. You just do not often find a near-4% yield paired with a double-digit long-term dividend growth rate.

But that’s what this dividend growth stock is offering you right now. This is not a name that usually offers a utility-like yield, either. Its five-year average yield is 2%. The current yield is almost twice as high as that. And the big dividend looks safe, protected by a payout ratio of only 35.2%.

But that’s what this dividend growth stock is offering you right now. This is not a name that usually offers a utility-like yield, either. Its five-year average yield is 2%. The current yield is almost twice as high as that. And the big dividend looks safe, protected by a payout ratio of only 35.2%.

I am completely shocked by this stock’s 50% drop from its recent high. Was there some correction due here? Sure. The stock’s 52-week high of $57.96 looked fully valued.

It may have even gotten slightly ahead of itself, with no margin of safety there. But I think the pendulum has swung too far to the other side, with the stock now sitting at about $29. I thought Comcast looked pretty decent at $50/share. It looked great at $40/share. But it looks downright amazing at $30/share.

We covered this company in late July, analyzing it and estimating its fair value at $57.77/share. Comcast looks materially undervalued right now. If your portfolio could use more media exposure, Comcast has to be top of mind.

One last thing I’ll note here about this name is that the low stock price could be a blessing: Comcast recently boosted its share repurchase authorization to $20 billion. That’s more than 15% of the entire company’s market cap. What an advantageous time to be buying back shares.

The third stock I have to highlight today is Domino’s Pizza Inc. (DPZ).

Domino’s Pizza is a multinational pizza restaurant chain with a market cap of $11 billion. Domino’s runs the largest pizza chain in the world. And what do we know about pizza? It’s a timeless food staple that translates extremely well.

I’ll tell you that I’ve been living in Thailand for more than five years. And guess what? Pizza sells well here, too.

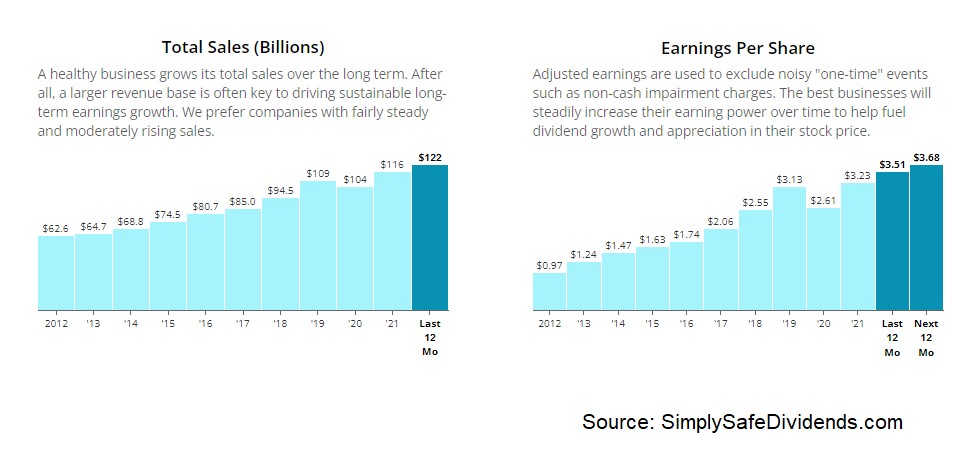

The US could be on the cusp of, or even in the midst of, a recession. But pizza is something that tends to be quite resilient when it comes to recessions. People have to eat. And pizza is a great-tasting, low-cost way to satiate oneself. That’s why Domino’s has been growing its revenue, profit, and dividend like gangbusters.

The pizza chain has increased its dividend for 10 consecutive years. And what a start they’re off to.

The five-year DGR is 19.4%. Even the most recent increase came in at 17%. On the other hand, the stock does yield just 1.4%. So that’s the give-and-take you’ve got. It’s more of a compounder than an income play. But seeing as how this stock is up more than 700% over the last 10 years, I’d say Domino’s is more than holding up its end of the bargain on the compounding side of things. And with a low payout ratio of 34.4%, I suspect Domino’s will continue to hand out sizable dividend increases.

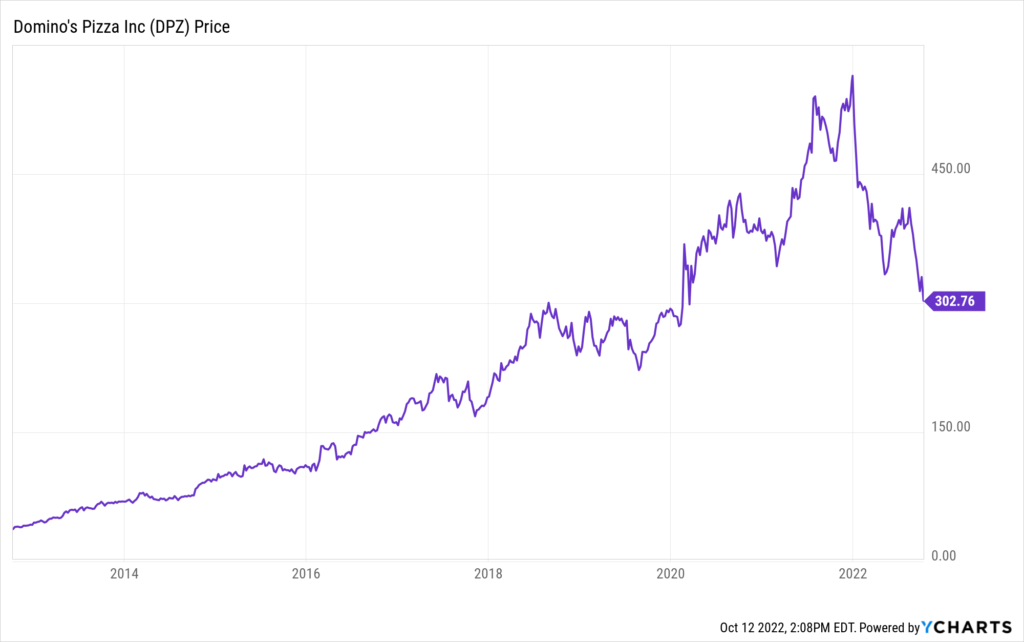

This world-class compounder has dropped by a stunning 45% from its 52-week high. This stock is still up by more than 700% over the last decade, even after a recent near-50% haircut. That’s incredible.

The 52-week high for the stock is $567.57. And you could argue it was expensive up there. But that was then. And this is now. The stock’s current pricing of $315 makes this business much, much more appealing.

The 52-week high for the stock is $567.57. And you could argue it was expensive up there. But that was then. And this is now. The stock’s current pricing of $315 makes this business much, much more appealing.

The P/E ratio of 24.5 might look rich at first glance, but its five-year average is 34.3. It’s typically received a premium multiple because of the premium growth – we’re talking about a 10-year CAGR of 24.3% for the company’s EPS.

Our most recent analysis and valuation video on Domino’s went live back in May, and that video showed why the business could be worth slightly over $441/share. We’ll have to update that coverage again soon. Meanwhile, consider taking a bite out of Domino’s after it’s stunning drop.

Fourth up today is U.S. Bancorp (USB).

U.S. Bancorp is a bank holding company with a market cap of $60 billion. U.S. Bancorp is in the business of money. And business is good. Always has been. Always will be.

Sure, the economy could be better. The bank could be better. Everything could always be better. But this bank continues to put up great numbers, which is probably why Warren Buffett, arguably the greatest investor to ever live, has nearly $5 billion of his firm’s capital invested in U.S. Bancorp.

Buffett wouldn’t be so heavily invested unless he believed that U.S. Bancorp could continue to grow its revenue, profit, and dividend for years to come. I’m inclined to believe the same.

The bank has increased its dividend for 12 consecutive years. And unless the next recession is on par with what we experienced during the Global Financial Crisis, which I think is a highly unlikely scenario, this bank is just getting started with the dividend growth train.

The 10-year DGR is 11.1%, although more recent dividend increases have been in the mid-single-digit range. That said, the stock yields 4.8%. That is an extremely uncommon yield for a large bank. That’s up there in REIT territory.

Indeed, this is 170 basis points higher than the stock’s own five-year average yield. With this kind of yield, you don’t need a huge dividend growth rate to make sense of things. And with a payout ratio of just 44.2%, the outsized dividend is healthy.

Indeed, this is 170 basis points higher than the stock’s own five-year average yield. With this kind of yield, you don’t need a huge dividend growth rate to make sense of things. And with a payout ratio of just 44.2%, the outsized dividend is healthy.

This stock didn’t look overly expensive at the 52-week high. But after dropping 37% from that level, it now looks downright cheap. The 52-week high for the stock is $63.57.

A bit too high? Sure. Egregious? I don’t think so.

A bit too high? Sure. Egregious? I don’t think so.

Either way, the stock is now below $40. And I fail to see how this is anything but downright cheap.

In fact, our recent analysis and valuation video on U.S. Bancorp showed why the bank could be worth $57.54 per share. We have what appears to be substantial undervaluation. And we also have what is for sure a very high yield. If you want to be invested alongside Warren Buffett, this might just be the best way to do it right now.

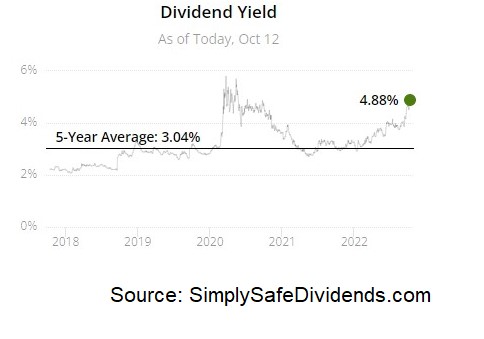

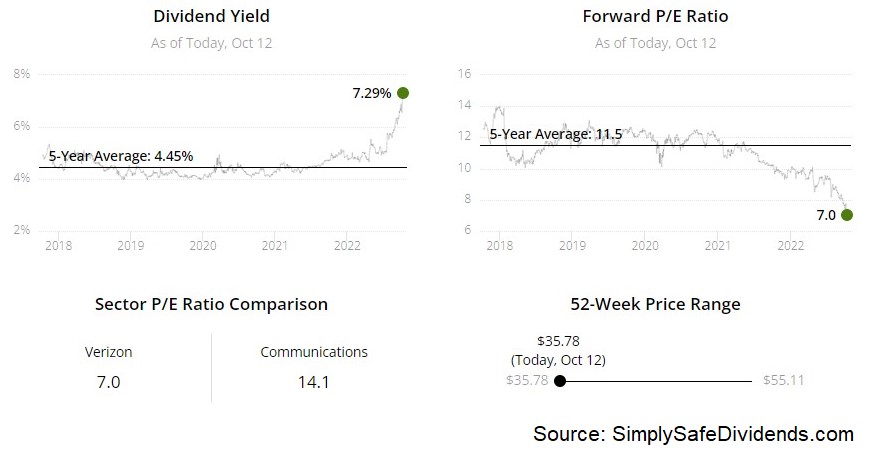

Last but not least, let’s cover Verizon Communications Inc. (VZ).

Verizon is a multinational telecommunications conglomerate with a market cap of $154 billion. There are some things to not like about Verizon. Namely, the balance sheet.

With more than $140 billion in long-term debt, there’s a serious weight here. On the other hand, Verizon gushes revenue and profit. More than $130 billion in annual revenue. More than $20 billion in annual net income.

They’re able to gush money because the services they’re providing, coalescing around high-speed mobile data, are ubiquitous. Many people would probably rather see their electricity cut than their mobile phone taken away from them. That bodes well for Verizon’s ability to continue gushing money, which obviously should lead to a gushing dividend.

The telecommunications company has increased its dividend for 18 consecutive years. The one bugaboo here is that debt load.

Otherwise, I see nothing to indicate that this dividend is going anywhere but up. Now, “up” is relative. Verizon is growing its dividend at a slow rate. The 10-year DGR is 2.5%. But you don’t buy Verizon for growth. You buy it for income. And it delivers in this regard. The stock’s yield is 7.1%.

Otherwise, I see nothing to indicate that this dividend is going anywhere but up. Now, “up” is relative. Verizon is growing its dividend at a slow rate. The 10-year DGR is 2.5%. But you don’t buy Verizon for growth. You buy it for income. And it delivers in this regard. The stock’s yield is 7.1%.

Even for Verizon, that’s a shockingly high yield. Consider its five-year average yield is 4.5%. We are in the stratosphere right now, relatively speaking. The payout ratio, at 52.4%, shows us a safe dividend, despite what the elevated yield may be saying.

This stock is down 34% from its 52-week high. I’m really surprised to see much Verizon has dropped. I say that because, at the 52-week high of $55.51, the stock didn’t look all that expensive from the outset.

Verizon has never been given a premium multiple. It’s always just kind of plodded along, throwing off a big dividend along the way. But with the stock now below $37, I’ve never seen it this cheap. And I’ve been investing for more than 10 years. The P/E ratio is 7.4. So this stock is offering a double 7 – a 7 P/E ratio and a 7% yield.

Verizon has never been given a premium multiple. It’s always just kind of plodded along, throwing off a big dividend along the way. But with the stock now below $37, I’ve never seen it this cheap. And I’ve been investing for more than 10 years. The P/E ratio is 7.4. So this stock is offering a double 7 – a 7 P/E ratio and a 7% yield.

How often do you see something like that? Almost never. This isn’t the kind of stock you buy because you think it’ll double tomorrow. But as long as they can continue to cover that massive dividend and increase it slightly each year, you’ve got it made in the shade from an income standpoint. Take a good look at Verizon here.

— Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Imagine having 12 new monthly income checks, carrying the potential of up to 21% yields.This is possible because of a tested strategy to get paid out regularly, like a paycheck. For over a decade, I have helped more than 26,000 investors secure 12 new monthly payouts. Meaning, you know exactly how much you'll make every month... Because of some stocks that pay us 8%,13.4%, and even 21.6% yields. See it for yourself here.

Source: Dividends & Income