The S&P 500 continues its epic run. That’s great if you bought stocks a while back. But what about putting new capital to work? Where are the deals?

Well, that’s what I’m here to talk about. While the market is at all-time highs, there are a lot of individual stocks that have strongly corrected.

In fact, I know of quite a few very appealing dividend growth stocks that are down huge. So if you’re the kind of investor who abstains from chasing stocks higher and likes to buy the dip, I’ve got you covered.

Today, I want to tell you about five high-quality dividend growth stocks that are down 20% or more from their respective 52-week highs. Ready? Let’s dig in.

The first high-quality dividend growth stock I want to highlight is Cummins (CMI).

Cummins is a multinational engine and power generation manufacturer with a market cap of $31 billion.

Cummins is in a sweet spot in a lot of ways. On one hand, they’ve got a great legacy engine and power generation business that has excellent fundamentals, brand power, and customer loyalty. On the other hand, they’re positioning themselves for the future of mobility by investing in fully electric and hybrid powertrain systems, as well as hydrogen fuel cell technology. Taking a strong foundation and making it even stronger? That should pay dividends – literally and figuratively. Indeed, Cummins isn’t just an engine powerhouse; it’s also a dividend growth powerhouse.

Cummins has increased its dividend for 16 consecutive years.

The five-year dividend growth rate of 8.5% easily beats inflation, even in this inflationary environment. And you get to pair that high-single-digit growth with a yield of 2.7%. That’s a very nice combination of yield and growth. And with a low payout ratio of 39.0%, this dividend is easily covered and highly likely to continue growing for years to come.

The five-year dividend growth rate of 8.5% easily beats inflation, even in this inflationary environment. And you get to pair that high-single-digit growth with a yield of 2.7%. That’s a very nice combination of yield and growth. And with a low payout ratio of 39.0%, this dividend is easily covered and highly likely to continue growing for years to come.

This is a great business, but the stock has been anything but great lately. It’s down 22% from its 52-week high.

The 52-week high is $277.09. Shares are currently trading hands for a bit over $216/each, so we’re a long way from those highs. I don’t know if/when it’ll just zoom right back up to the $280 area. And in all honesty, that kind of pricing looked a bit expensive to me. That said, I recently highlighted Cummins as a high-quality dividend growth stock that looked undervalued. In that full analysis and valuation video, I estimated intrinsic value for Cummins to be right about $250/share. So there’s a lot of potential upside here. And in the meantime, you’re collecting a market-beating yield growing at a high-single-digit rate. There’s really not much to complain about.

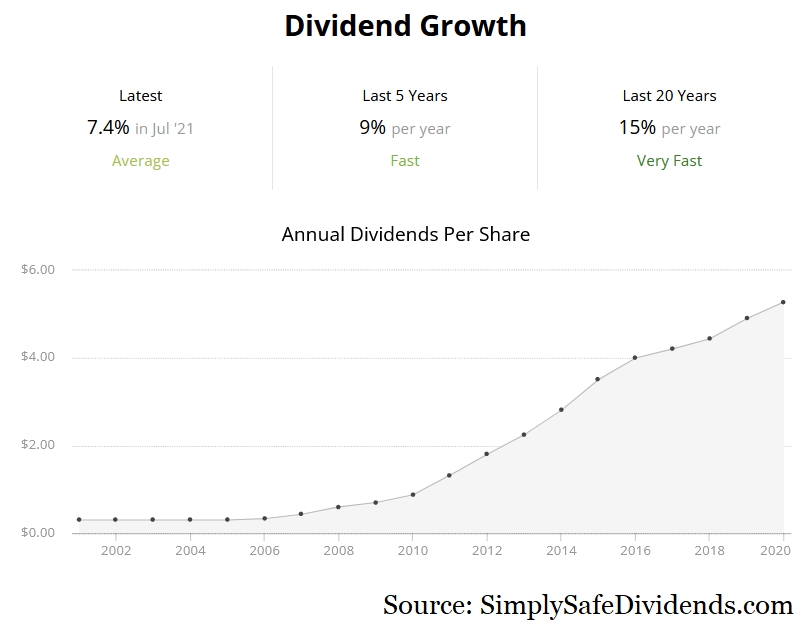

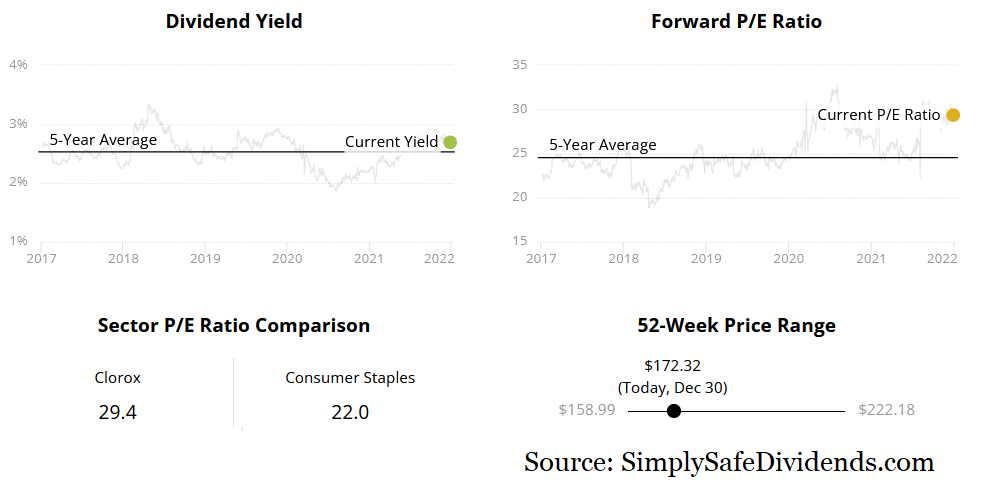

Next, let’s talk about Clorox (CLX).

Clorox is a global manufacturer and marketer of a variety of everyday consumer products with a market cap of $21 billion.

Clorox was a 2020 darling, back when the pandemic first broke out and people were buying up cleaning products like crazy. Clorox’s sales went through the roof, which drove the stock through the roof. Well, it’s been a totally different story in 2021. This stock went from darling to disaster. However, that’s just the stock. The business is still holding up pretty well. After all, people are still going to continue buying products like kitty litter and trash bags. More importantly, the dividend has held up perfectly.

The company has increased its dividend for 44 consecutive years.

What’s really admirable about Clorox is how consistent they stayed throughout the crisis. It’s easy to get wrapped up in the moment and react emotionally, but Clorox didn’t do that. They increased the dividend at basically the same rate in both 2020 and 2021 – despite those years looking very different in terms of sales. That prudence and commitment to the long-term plan is fantastic. The 10-year dividend growth rate of 7.5% is paired with a yield of 2.7%, so we’re looking at a 10%+ combination of yield and growth here. I like that. The payout ratio is 83.6%, based on midpoint adjusted EPS guidance for this fiscal year. That’s somewhat high, but the business will likely normalize starting in 2022.

While you wait for that normalization, there could be an opportunity here. The stock is 26% off of its 52-week high.

Now, there’s an argument to be made that the stock should have never touched its 52-week high of $231.11 in the first place. The market seemed to be permanently pricing in a lot of temporary, pandemic-related sales. However, down here around $170/share, Clorox looks very interesting. I last analyzed and valued the business back in the summer, estimating fair value to be about $193.50/share. So I don’t know why people were paying over $230/share in early 2021. Likewise, I don’t know why people would be shunning it down here. Take a look at Clorox, if you haven’t already.

Now, there’s an argument to be made that the stock should have never touched its 52-week high of $231.11 in the first place. The market seemed to be permanently pricing in a lot of temporary, pandemic-related sales. However, down here around $170/share, Clorox looks very interesting. I last analyzed and valued the business back in the summer, estimating fair value to be about $193.50/share. So I don’t know why people were paying over $230/share in early 2021. Likewise, I don’t know why people would be shunning it down here. Take a look at Clorox, if you haven’t already.

I now want to highlight Corning (GLW).

Corning is a multinational technology materials company with a market cap of $32 billion.

Corning is the go-to company when it comes to specialty glass, which is used in applications ranging from portable electronic devices to fiber optics. Does anyone think any of this will be less important or used less tomorrow, five years from now, or ten years from now? If you think that, raise your hand. Right. I didn’t think so. And because of that, Corning is positioned to benefit from all kinds of tech trends, which bodes well for their ability to continue paying and increasing their dividend.

This company has increased its dividend for 11 consecutive years.

The five-year DGR of 12.9% is impressive, especially since you’re layering that double-digit dividend growth on top of a yield of 2.6%. You usually have to sacrifice yield in the face of growth, or vice versa. But Corning gives you a nice dose of both. And this market-beating dividend is protected by healthy free cash flow that covers the dividend more than twice over.

The stock has fallen 20% from its 52-week high. If you like buying the dip, this stock has dipped big time.

The stock has fallen 20% from its 52-week high. If you like buying the dip, this stock has dipped big time.

Actually, this is more than a dip. It’s a full-on correction – and then some. The 52-week high is $46.82. Shares are now going for a bit over $37/each. And you know, even at the 52-week high, the stock didn’t look obscenely valued. It’s just that it’s a lot more appealing now than it was back then. Indeed, most basic valuation metrics indicate notable undervaluation. That aforementioned 2.6% yield, for example, is 30 basis points higher than the stock’s own five-year average yield. And the P/CF ratio of 9.7 is well off of its own five-year average of 11.7. In a sea of expensive stocks, Corning is trying to throw you a lifeline. It’s definitely worthy of consideration here, if not capital.

The fourth high-quality dividend growth stock we have to talk about is International Bancshares (IBOC).

International Bancshares is a Laredo-Texas based bank holding company with a market cap of $2.7 billion.

Charlie Munger, Warren Buffett’s right-hand man and billionaire investor in his own right, has shared his affinity for the banking business model on numerous occasions. And what’s not to love? Owning a great bank is about as close as it gets to owning a money tree. Now, small banks, like this one, have a different risk/reward setup than the large banks. Greater risk, greater possible reward. And that translates to the dividend, too.

This bank has increased its dividend for 12 consecutive years.

It might be small, but the bank packs a big dividend punch. The five-year DGR is 13.7%. And the stock yields 2.9%. That’s the best combination of yield and growth out of the five stocks I’m talking about today. Actually, forget the comparisons. It’s just a great combination in general. It’s rare that you get a near-3% yield and double-digit dividend growth. And with a payout ratio of just 30.2%, the dividend is clearly headed higher. One thing to be aware of about the dividend is that it’s paid semi-annually.

The stock has been in a downtrend since March, and it’s now down 20% from its 52-week high.

The stock has been in a downtrend since March, and it’s now down 20% from its 52-week high.

That’s despite the business reporting some very strong numbers all year long. The 52-week high of $53.06 looks distant when compared to the current stock price of right about $42. But it could easily close that gap, as the stock doesn’t look expensive at all. If anything, it looks cheap. That 2.9% yield is 80 basis points higher than its five-year average. The P/B ratio is 1.2. And the current P/E ratio of 10.8 significantly trails its own five-year average of 14.3. If your portfolio has room for a small bank, I’d take a close look at this name.

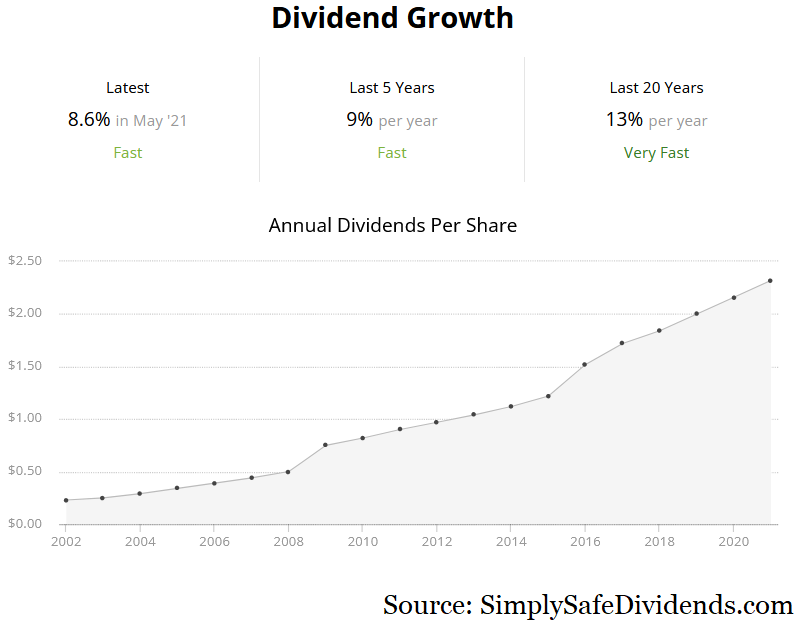

Last but not least, let’s discuss Medtronic (MDT).

Medtronic is a global medical devices manufacturer with a market cap of $140 billion.

This is one of the best businesses around. And it’s in a general area of the economy – healthcare – that is experiencing secular long-term growth. In addition, a lot of their specific products are extremely non-discretionary in nature. However, because vaccine makers have been sucking all of the oxygen (and capital) out of the room, almost everything else in healthcare has suffered. On top of that, Medtronic has shot itself in the foot with some quality control issues at a California facility. Despite all of that, this company has a very bright future. And so does its dividend.

The company has increased its dividend for 44 consecutive years.

This is a vaunted Dividend Aristocrat. With a 10-year DGR of 10.0% and a yield of 2.4%, you’re getting great compounding prowess and a yield that circles the market twice over. If 44 straight years of ever-higher dividends wasn’t enough to instill confidence, the payout ratio of 44.2%, based on midpoint guidance for this fiscal year’s adjusted EPS, ought to.

This is a vaunted Dividend Aristocrat. With a 10-year DGR of 10.0% and a yield of 2.4%, you’re getting great compounding prowess and a yield that circles the market twice over. If 44 straight years of ever-higher dividends wasn’t enough to instill confidence, the payout ratio of 44.2%, based on midpoint guidance for this fiscal year’s adjusted EPS, ought to.

This stock has been in free fall since early September, and it’s now down 23% from its 52-week high.

It’s pretty rare that you’ll see a Dividend Aristocrat just totally fall off a cliff like this. But as I always say, I see short-term volatility as a long-term opportunity. Indeed, I recently highlighted Medtronic as an undervalued high-quality dividend growth stock idea in late November. In that video, I estimated intrinsic value to be almost $124/share for the business. The stock is currently at under $105, which is a long way from the 52-week high of $135.89. It might have been a bit rich at that 52-week high, but it looks materially undervalued now that it’s close to its 52-week low. In my view, Medtronic is a high-quality Dividend Aristocrat that’s screaming opportunity after some recent volatility.

— Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

The goal? To build a reliable, growing income stream by making regular investments in high-quality dividend-paying companies. Click here to access our Income Builder Portfolio and see what we’re buying this month.

Source: DividendsAndIncome.com