Bull market, bear market, it doesn’t matter: Underappreciated, under-covered companies always manage to make a splash.

That’s how my Hidden Yields service delivers portfolio doublers every five or six years. The market has clusters of dividend growth stocks that are too boring for the financial media or most analyst firms to lavish with coverage, and that don’t yield nearly enough for income hunters to take notice.

Yet time and time again, these stocks turn into total-return machines that can rip off 15% in annual returns, rain or shine.

And the current bear market is providing a rare opportunity to pinpoint these payout powder kegs.

In fact, a handful have popped up on my radar of late, and in a minute, I’ll show you these three outperforming oddballs.

First, let’s talk about “defense.”

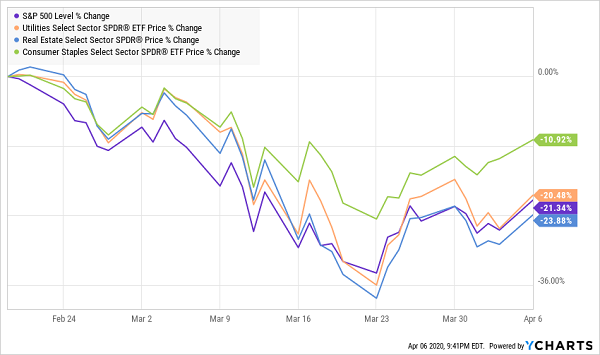

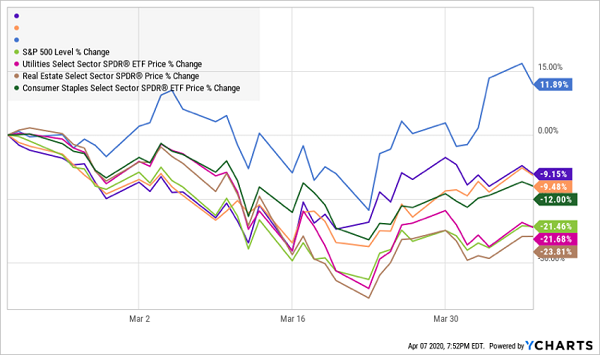

Consumer staples. Utility stocks. Real estate. These were the companies that were supposed to save us from the bear market. Their defensive nature, not to mention oodles of dividends, were a supposed no-brainer for whenever disaster struck and investors were sent scrambling for life preservers.

But theory and reality have played out much differently.

One Outta Three Ain’t Good

Sure, big dips allow investors to go fishing for once-in-a-lifetime dividend buys, but you don’t want to be the guy holding onto those stocks while they’re plunging. While staples have held up their end of the bargain, utilities and real estate have been woefully inadequate. That’s especially maddening in the case of slow-growth utility stocks, which effectively live to serve as hedges against market downturns, but have provided only minimal downside protection this time around.

In the meanwhile, a trio of companies have earned plenty of plaudits (but received none) by quietly chugging along, outperforming the market and even “safe” sectors.

Most investors haven’t batted an eye. And that’s a shame. Because there’s much more to these three companies than their stellar outperformance in this bear market.

Let me introduce you to three companies that are past due for a little attention. Their yields on current prices might not stir you into a frenzy. But they’ve made a statement these past few months, and their seemingly durable businesses are fueling persistent dividend growth—a core component of high and sustainable retirement returns.

RLI Corp. (RLI)

Dividend Yield: 2.2%

RLI Corp. (RLI) is in the dreadfully boring insurance business, offering business, personal and surety products across the U.S. About two-thirds of its business is in the casualty segment (personal umbrella, executive products, general liability and others); another 23% in property products such as excess & surplus and earthquake; and the rest in contract, commercial and other surety.

At least its history is a little more interesting.

The company got its start in 1961 as a contact lens insurance agency called Replacement Lens Inc. (hence the current acronym). It eventually merged its contact lens division with Hester Enterprises, which makes Maui Jim Glasses – a legacy investment that it retains a 40% stake in to this day. It eventually moved into specialty P&C coverage in 1997, and it earned an A.M. Best A+ rating in 2004 that it carries to this very day.

Investors might be more interested in its dividend history, however, which includes 44 consecutive dividend hikes – with a 45th potentially on deck if the company announces in May, per usual. Also interesting is its financially responsible dividend program, which includes small quarterly payouts and a large special dividend as profits allow. RLI has now delivered 10 of these special annual payouts without interruption.

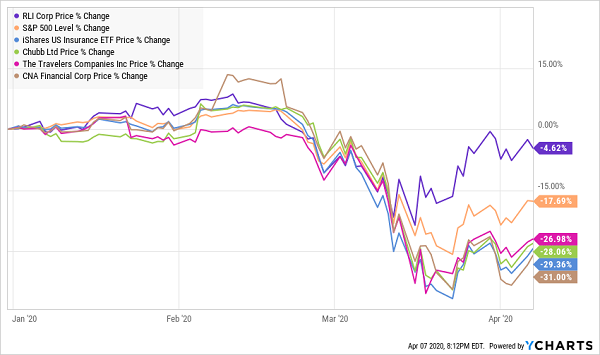

What’s really remarkable, however, is this insurer’s performance through the downturn.

What’s notable isn’t just RLI’s price action compared to the market, but compared to the insurance industry at large, as well as several of its best-known competitors. No, RLI isn’t selling toilet paper or medical facemasks. It just has balanced, diversified product lines, and a similarly smooth investment allocation that helps it churn out more consistent products than many of its peers.

It’s a yawner of a business, but RLI delivers where it counts.

West Pharmaceutical (WST)

Dividend Yield: 0.4%

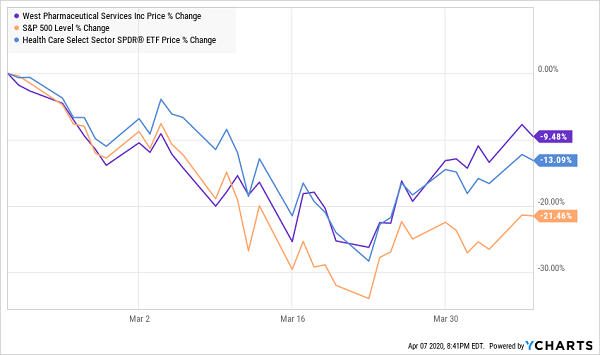

No one should be surprised to see a pharmaceutical name on this list given just how understandably well the healthcare sector has held up in this crisis.

But West Pharmaceutical (WST) isn’t really a traditional pharma name. In fact, West doesn’t really make drugs at all. But what it does is every bit as necessary – it creates the packaging that carries those vital treatments – vials, stoppers, seals, as well as more complex products such as self-injection systems and syringe/cartridge components.

In other words, West Pharmaceuticals isn’t going to create the first coronavirus vaccine. But it’s entirely possible that vaccine might come in a West Pharmaceuticals-made vial.

Again, a boring business, but also an extremely vital one that will see demand no matter what. And the stock acts like it.

Like RLI, this boring business has fueled a longstanding dividend. West Pharma is a Dividend Champion that has raised its payout for 27 consecutive years and counting. The 0.4% yield is a laugher, but the longer your money is wrapped up in WST, the more income you should collect.

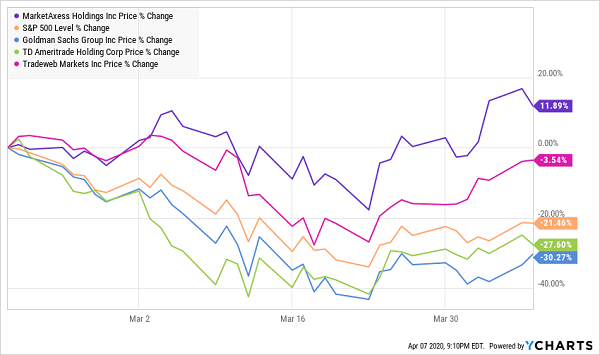

MarketAxess Holdings (MKTX)

Dividend Yield: 0.6%

MarketAxess Holdings (MKTX) is a fintech company that’s leading an investing revolution – the migration of bond trading into the here and now.

While institutional investors were quick to adapt electronic trading in equities, the debt-market shift hasn’t been as rapid. As of last year, only about a quarter of corporate bonds were traded electronically, and MarketAxess effectively owns that market. Its 85% market share dwarfs competitors Tradeweb Markets (TW) and Bloomberg. MKTX also has its hand in international bonds, too.

And bonds have been big business of late.

It’s difficult to find much in the way of direct competitors, but MKTX is outperforming Tradeweb through the downturn, and it’s clobbering most anything else tied into market business.

Bond trading shot up by more than 50% year-over-year during March, to $269.5 billion. And the company allowed “a record number of users to access our global liquidity and manage risk,” according to CEO Rick McVey.

MKTX doesn’t have nearly the dividend history of the prior two stocks, but it has been aggressively growing that payout. Its 60-cent quarterly dole to start the year was nearly 18% better than a year ago, and 130% better than 2016 levels. New money can expect the current yield to get much better over time.

— Brett Owens

How to Collect $4,000 in Dividends Each and Every Month [sponsor]

Of course, MarketAxess could double its dividend in each of the next two years and still deliver less income than a corporate-grade bond fund. They’ll be powerful total return machines way, way down the road, but investors with bills to pay need something much more substantial.

And you can lock in that kind of income via my “Monthly Dividend Superstars.”

These aren’t 1%, 2% or 3% yields that need years to blossom into real cash generators. These companies are doling out roughly four times the market average at their currently discounted prices, giving income investors a chance to pounce on a proven 1-2 combo:

High dividends at low prices.

These contrarian plays tick off every checkbox in the retirement wish list, including …

- High annual yields nearing 10%. That translates into over $4,000 in monthly income … on a nest egg of just $500,000. It’s all gravy from there if you’ve saved up even more.

- Real upside potential of about 10% annually. That will keep your nest egg growing in retirement, protecting it against any sudden financial “shocks.”

- Hidden value. There’s such a thing as “too popular.” If too many investors crowd into a stock, it becomes grossly overpriced, making more upside difficult to come by and increasing the risk of hyper-aggressive selling if investors get nervous. My “Dividend Superstars” are too small to be flush with institutional money, and far off the radar of many analysts, creating price inefficiencies that you and I can exploit.

This is the path less traveled.

Most finance-TV pundits will tell you to sink your hard-earned retirement money into “can’t-miss” blue chips like the Dividend Aristocrats. They’ve grown their dividends for decades, and probably will for decades more.

Ignore that nonsense. Those same Dividend Aristocrats only yield a little more than 2% on average, and the most established Aristocrats have slowed their dividend growth to a sloth’s pace. Worse, some of these “Aristocrats” might be kicked out of the club by this time next year, their artificially propped-up payouts exposed by a lethal dose of reality. If you retire with these kinds of stocks, your income stream will dry up so quickly that, within just a few years, you’ll be forced to hack away at your savings to pay your monthly bills.

Don’t take that gamble. Pay your monthly bills with outsize monthly dividend checks, and use the leftover cash to take a couple trips, build that backyard pool or spoil your grandkids rotten.

Let me show you the way to a set-it-and-forget-it 10% portfolio. Click here to get a FREE copy of my exclusive “Monthly Dividend Superstars” report, complete with tickers, buy prices, yields and analysis … as well as other bonuses, including 12 popular dividend stocks that you need to SELL NOW before they ruin your retirement.

Source: Contrarian Outlook