With so much pain in the retail space, it’s easy to get pessimistic about apparel companies. However, some brands have a certain type of immunity in this mess, one of which is Lululemon Athletica (NASDAQ:LULU). While LULU stock is still down more than 26% from its highs, shares fell an incredible 51.6% from peak to trough.

That kind of performance is simply an overreaction and it’s unlikely investors will get such a great opportunity in the stock again.

Put simply, Lululemon is a premium consumer brand.

Although it’s possible for the company to fall out of favor, that’s not the case right now.

The company continues to pull the right levers. Prior to the novel coronavirus outbreak momentum had been quite strong. Lululemon may not be on Apple’s (NASDAQ:AAPL) level per se, but it’s up there with Nike (NYSE:NKE).

Does Nike Provide Clues?

On March 24, a day after the market bottomed, Nike reported its fiscal third-quarter results. Keep in mind, this isn’t for a quarter ended months ago, it was a quarter that ended Feb. 29. Nike beat on earnings and revenue estimates, and pointed to a huge rebound in pent-up demand out of China. Further, management said that online sales had been strong amid the global outbreak.

What does that have to do with LULU stock?

Lululemon has that “it” factor, as does Nike. It’s not immune to mall closures and retail slumps, but like Nike, people are going to buy its products in good times and bad. That’s evident by its own quarterly earnings report on March 26.

Like Nike, Lululemon reported earnings late March. However, the reported period ended Feb. 2, so it doesn’t give us as good of a look at how the virus is impacting business. Still, the company was able to beat on earnings and revenue expectations.

Further, management pointed out that once coronavirus restrictions were relaxed in China, there was an immediate spike in business. That has improved week by week, but it’s the online sales that caught our attention. Nike said it saw a near-triple-digit spike in Chinese digital sales. Lululemon saw a 60% jump in its Chinese digital channel, while management remains committed to doubling its store count in the country this year.

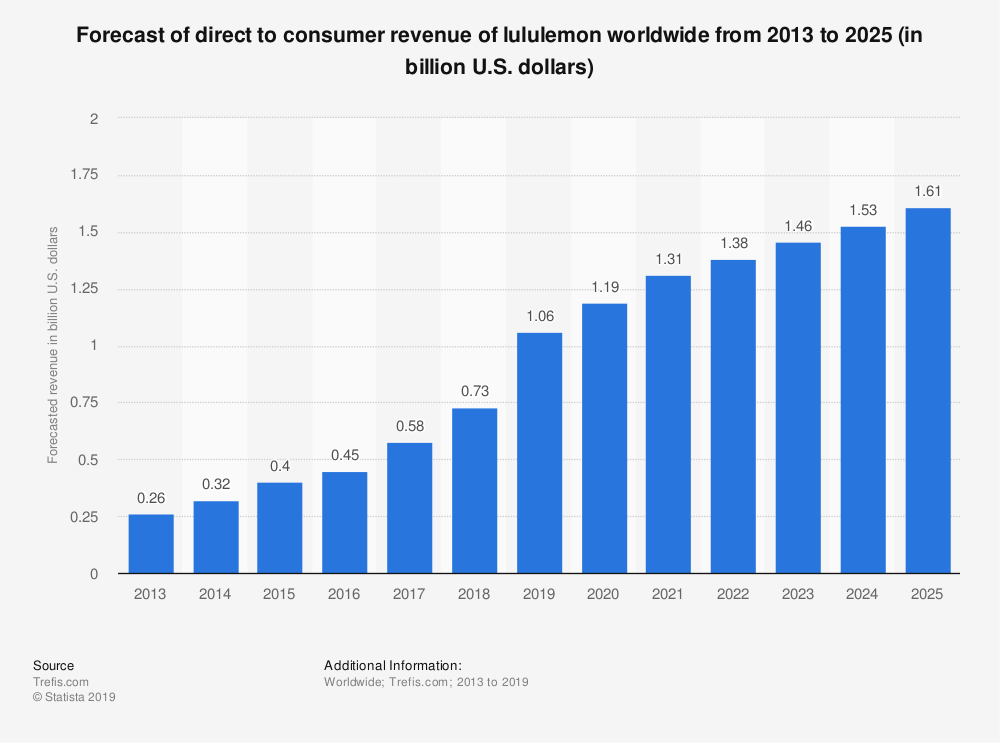

Source: Chart courtesy of Statista, Source from Trefis.com

Source: Chart courtesy of Statista, Source from Trefis.com

Nike has a larger presence in China, but both companies show how this region can be a significant revenue generator. In a way, looking at LULU stock is like looking at Nike in the past — and that’s very encouraging for Lululemon’s future. Particularly with both companies’ latest quarterly figures.

Future of Commerce

Think of the big-box retailers that are doing well, like Target (NYSE:TGT) and Costco (NASDAQ:COST). Or brands like Apple, Nike and Lululemon. They all have one thing in common over their peers that are dying out: traction in e-commerce.

These companies do an excellent job blending in-store sales and experiences with online sales. It’s not just China where Lululemon is experiencing strong online sales. In the quarter, overall revenue rose 20%, while comp-store sales climbed 9%. However, direct-to-consumer (DTC) sales jumped 41%.

One could argue that Lululemon is more exposed to changes in fashion trends and has a smaller addressable market than Nike. That’s true, but like its athletic-apparel peer, Lululemon is leaning more on DTC sales to drive its top line. As retail continues to evolve, this should only benefit LULU stock in the long run.

Bottom Line on LULU Stock

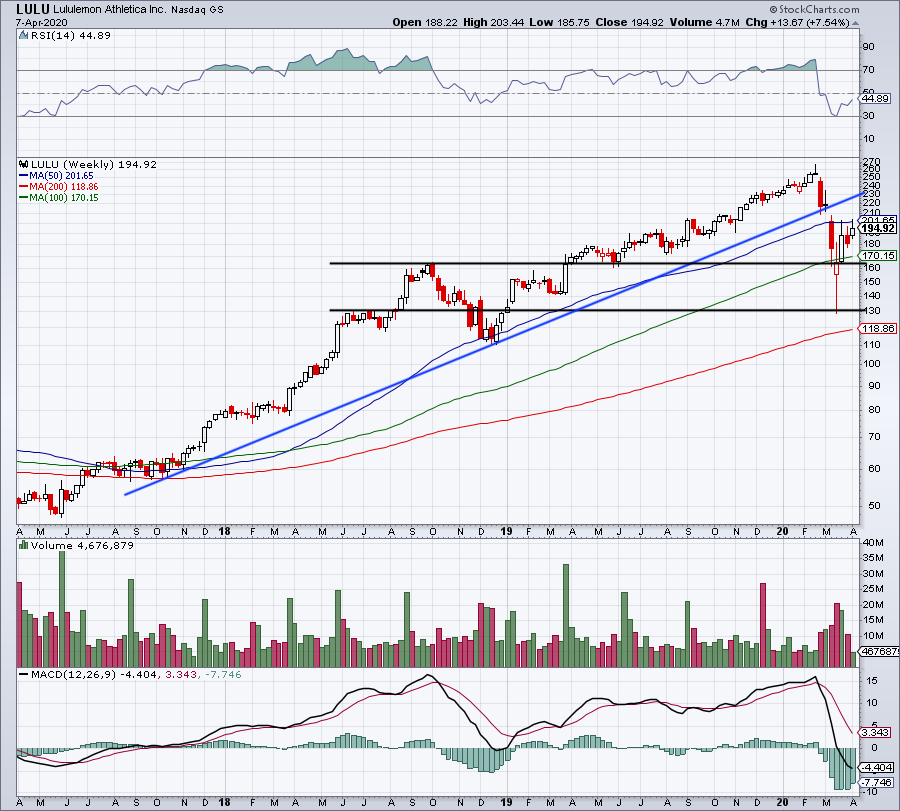

Source: Chart courtesy of StockCharts.com

Source: Chart courtesy of StockCharts.com

At the end of the day, brands like Nike and Apple thrive for a few main reasons: They innovate and they have great customer loyalty. It doesn’t take a rocket scientist to see that Lululemon has similar qualities.

LULU stock is an excellent stock for those with a long-term view and can see the value in Lululemon. There will be carnage in retail, but the cream of the crop will rise to the top. I would be surprised if shares retest the lows near $130. If they do — down abut 50% from the highs — buy-and-hold investors will be rewarded down the road. But even a dip back into the $165 area wouldn’t be so bad.

— Matt McCall

Legendary fund manager Louis Navellier – a man Forbes calls "the king of quants" – is going "ALL-IN" on this game-changing AI technology. He says, "This is the culmination of everything you've been reading about AI for the last 60 years."Get the details...

Source: Investor Place