Today I want to show you how you can retire on $405,000—and with just five buys, too! Put together, these five stocks and funds hand you a 7.4%-yielding portfolio that will pay you reliably for decades.

First, though, let’s quickly run through how our “5-buy” portfolio will work—and how it proves the so-called “experts,” who say you need a million dollars or more to clock out—are dead wrong.

A Million-Dollar Retirement … for $405K!?

To be smack in the middle of income in America, you need to bring in about $30,000 per year. So, at a 7.4% yield, you’d need to invest $405,000. In other words, that’s how much it takes for a person to retire and be middle class in America.

I know what you’re thinking: “That sounds great, but where the heck am I supposed to find a safe dividend that high anywhere in the market?”

Fair question—and that’s why I’ve chosen a special kind of fund called a closed-end fund (CEF) to form the bedrock of our 5-pick portfolio.

These funds—like the 21 in the portfolio of my membership-only CEF Insider service—regularly pay this much and often more, with yields well into the double digits.

And for years, CEFs have been helping retirees quit the rat race earlier than the “experts” say is possible.

Here’s how.

If you want to get $30,000 per year in income from something like the S&P 500 SPDR ETF (SPY), you’d need to invest over $1.6 million. That’s because SPY yields a measly 1.8%, a fraction of what CEFs provide.

Plus, many CEFs let you diversify beyond stocks, as these funds go further afield, into areas like bonds and real estate investment trusts (REITs), helping insulate you from a market crash.

Interested? Read on and let me show you the keys to high-yield financial independence.

Pick #1: A Mortgage and Bond Fund From the Biggest Name in CEFs

The PIMCO Dynamic Income Fund (PDI) yields 8.3% and even pays you a dividend every month instead of every quarter. That high payout comes from its combination of corporate and mortgage-backed bonds, which are handpicked by PIMCO, widely seen as one of the best bond-investment companies in the world.

PDI has been growing its dividend since inception, in addition to paying periodic special dividends, which is why it’s been delivering a total return that crushes the market over the fund’s lifetime:

Huge Monthly Dividends Drive Huge Gains

Also, since PDI doesn’t invest in stocks, it’ll help you diversify in case of a market correction: note how the orange line above is much smoother than that of SPY. That’s because of the fund’s lower volatility and bigger income stream, which help you weather short-term downturns. PDI investors have been sleeping well at night for years.

Pick #2: “Boring” Utilities and Exciting Outperformance

I wouldn’t blame you if you said the Gabelli Utility Trust (GUT) sounds boring: a utility fund with a stable portfolio, GUT boasts a “no-drama” 8.4% dividend that’s been a mainstay of high-income investing for years. But no matter how boring its investments sound, GUT’s results are anything but dull:

GUT Powers Past Stocks

With more than double the total return of the S&P 500 over 20 years, GUT has proven that you can beat the market for a long time, again showing that a long retirement on a reasonable nest egg is possible.

Pick #3: The New Kid on the Block

The 5.8%-yielding Blackrock Science & Technology Trust II (BSTZ) is one of BlackRock’s newest funds. Managed by the firm’s tech and growth-stock team, who have been crushing the market in other funds for years, BSTZ has the promise of long-term outperformance, thanks to BlackRock’s unique access to the market.

Simply put, because it has over $6 trillion in assets under management and is a creditor for many companies in tech and beyond, BlackRock knows where to go for big returns.

A nice thing about BSTZ is that it goes far beyond “FAANG” stocks—Facebook (FB), Amazon.com (AMZN), Apple (AAPL) and Google (known as Alphabet [GOOGL])—to find hidden gems that haven’t already been bid up in the tech world.

In addition to private firms you can’t easily buy, like C3 AI, BSTZ also holds names like Twilio (TWLO) and IAC/Interactive Corp. (IAC), which are still up over 25% in 2019, even after recent market volatility.

Think of BSTZ as a way of buying into the best of private and public tech firms before they turn into the next Google, all while benefiting from BlackRock’s market access and research capacity. Those were the secret weapons that have made BlackRock’s other tech funds outperform, so expect this one to do the same over time.

Pick #4: Profit Like a Landlord—Without the Hassle

The Cohen & Steers Quality Income Realty Fund (RQI) is a way you can get rich off of real estate without dealing with tenants or maintenance. That’s because RQI invests in many different companies that hold thousands of different properties between them—and professional managers pick up and distribute the rents to RQI shareholders.

Does this system work? You bet. With a 6.2% yield, RQI’s passive income stream is a main part of its success story:

Dividends Help RQI Clobber the Market

With nearly double the market’s returns, RQI is another index-buster that’s seen investors happily enjoying massive gains for nearly two decades. And the fact that RQI, as a real-estate fund, survived the subprime-mortgage crisis and still delivered outperformance just proves how powerful this CEF is.

Pick #5: Tap an 8.3% Yield With This Savvy Business Investor

Business-development companies (BDCs) have a unique model: by pooling together investors’ capital and lending it to mid-sized firms that don’t want to deal with banks, BDCs have carved a niche that gives you a large income stream and diversification away from stocks.

Many people don’t know about BDCs, but they should; many of these companies yield over 7% and have massive long-term returns.

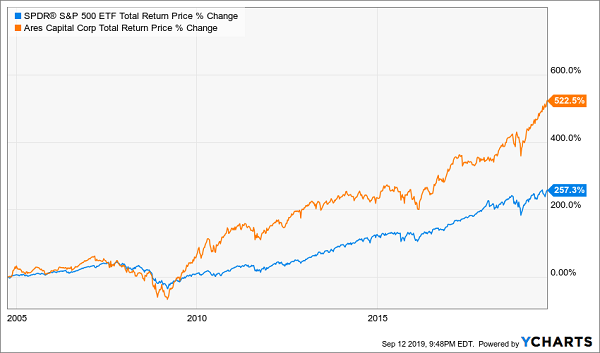

Ares Capital Corporation (ARCC) is a prime example. One of the largest and most successful BDCs, it has crushed the market and survived recessions while giving investors a growing dividend—currently at 8.3%:

ARCC Blows Past the Market

There are two main reasons for Ares’s success. First, its size lets it diversify widely, to ensure it isn’t too exposed to one market or another. Second, Ares’s depth of knowledge and experience in private corporate lending help it find the best deals.

The Final Word

As I just showed you, you can create a diversified high-yielding portfolio that crushes the market and makes retirement on a reasonable nest egg possible. Don’t believe the fearmongers: financial freedom is closer than you realize.

— Michael Foster

Don’t Let Fear Keep You From These Huge 8% Dividends (and Gains) [sponsor]

You know what’s even worse? Wall Street actively steers folks away from CEFs—the one piece of the retirement puzzle that’s essential if you want to clock out on a reasonable nest egg!

That’s because your typical advisor would rather you just buy popular blue chips or ETFs. It’s easier than having to do the actual legwork needed to help you tap into the big payouts (and upside) in quieter corners of the market, like CEFs.

But if you take just a few moments to dip your toe into CEFs, it can pay off very handsomely for you. I just showed you how—by building a “no-drama” 7.4%-yielding retirement portfolio that sets you up for nice price gains, too!

All in just a handful of buys.

Here’s the best news: I’ve tracked down 5 other “hidden” picks—all CEFs—that yield even more than the 5 picks above: I’m talking huge 8% payouts, on average.

And that’s just the average! One of these picks pays an incredible 9.3% now, has exploded 743% since inception (absolutely dominating the market) and has plenty more upside, thanks to its current massive discount.

A 9.3%-Paying Outperformer You Need to Buy Now

I know it sounds crazy that a fund could be cheap after a run like that, but this kind of thing happens all the time in CEFs. And now is a terrific time to jump in.

The whole “5-pack” of 8%+-yielding CEFs (with 20%+ price upside in the next 12 months!) is waiting for you now. All you need to do is click here and I’ll share the full story: names, tickers, buy-under prices, my unfiltered take on management—the works!

Source: Contrarian Outlook