Today I’m going to expose a major mistake way too many folks make. Then I’m going to reveal 3 totally ignored stocks whose dividends are soaring. They yield up to 5.8% now and are poised for 50%+ gains in short order!

More on those in a moment. First, we need to talk about that classic wealth-killing blunder.

Funny thing is, it’s one of those moves that seems like the safe thing to do, but if you fall into this trap, you’ll leave a fortune in gains—and income—on the table!

I’m talking about limiting your portfolio to the household names of the S&P 500.

I hate seeing investors do that, especially because there’s another—much bigger—group of stocks out there that has thoroughly outgunned the popular names.

But these unsung wealth builders don’t get nearly the respect they deserve.

I’m talking about midcap stocks, or companies with market capitalizations between $2 billion and $10 billion (especially the three I’m going to show you below).

Midcaps are in a sweet spot that gives you the best of all worlds: higher liquidity than you’ll find in small caps but faster growth than you’ll ever get from large caps.

And here’s something that will probably surprise you (it did me): midcaps have clobbered their small- and large-cap cousins over the long haul.

Here’s how the S&P 400 MidCap Index, with a median market cap of $3.5 billion, has performed against the S&P 500 and its small cap rival, the S&P SmallCap 600 (with a median market cap of $1.0 billion) over the past two decades:

Red-Hot Gains From “Goldilocks” Stocks

Even better, midcaps have taken a bit of a breather this year, so many haven’t seen the big price run-ups the market’s biggest players have racked up.

Even better, midcaps have taken a bit of a breather this year, so many haven’t seen the big price run-ups the market’s biggest players have racked up.

Translation: it’s time to go bargain hunting!

A “Just Right” Entry Point

Here are 2 other reasons why these Goldilocks plays deserve a place in your portfolio:

Here are 2 other reasons why these Goldilocks plays deserve a place in your portfolio:

- They pay dividends: Unlike small caps, which mostly plow their profits back into their businesses, midcaps pay dividends—and sometimes big ones! As I write, the Vanguard Mid-Cap ETF (VO) pays 1.4%, not far below the SPDR S&P 500 ETF (SPY), at 1.9%. But don’t let that headline number fool you, because plenty of midcaps throw off much bigger yields, like the 5.8% payer I’ll show you in a second.

- They’re off the radar: Wall Street largely ignores midcaps. One of the stocks I’ll tell you about below has just two analysts covering it. Compare that to Apple (AAPL), the biggest US company by market cap, with 32! That thin coverage is fine for us because we get a wider field in which to find bargains than we’ll ever get in the large cap universe.

Here are 3 mid-caps that should definitely be on your radar now.

Midcap Pick No. 1: This Dividend’s on a Roll

Penske Automotive Group (PAG) stock has been sideswiped by worries about decelerating car sales, falling 13% this year.

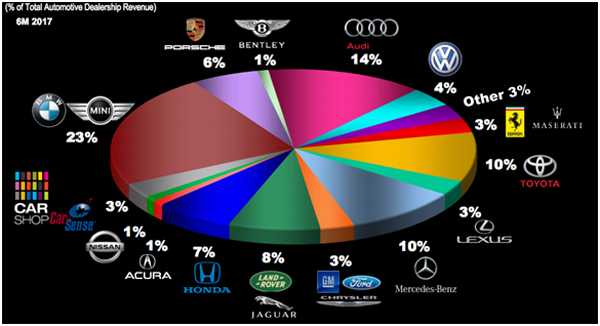

Too bad management didn’t get the memo, because the company, owner of car and commercial truck dealerships in the US, Canada and Western Europe, saw record numbers of vehicles roll off its lots in the second quarter (up 13% from a year ago), along with record revenue (up 2.5%) and earnings per share (EPS; up 10.8%).

The reason? Diversification. Check out the number of brands—both high- and lower-end—Penske peddles, and how nicely spread out its revenue was in the first half of 2017:

A Diversified Sales Machine

Source: Penske Automotive Q2 investor presentation

Source: Penske Automotive Q2 investor presentation

Here’s where that pays off: through July, US car sales were down 2.9% from a year earlier. That sounds bad, but remember we’re coming off a string of record years here.

And Penske didn’t even notice thanks to its brand diversification and one other big factor: huge growth in used car sales. In Q2, the company wheeled 66,208 secondhand rides, up 25.1% from a year ago and more than the 63,919 new cars it sold (up 2.8%)!

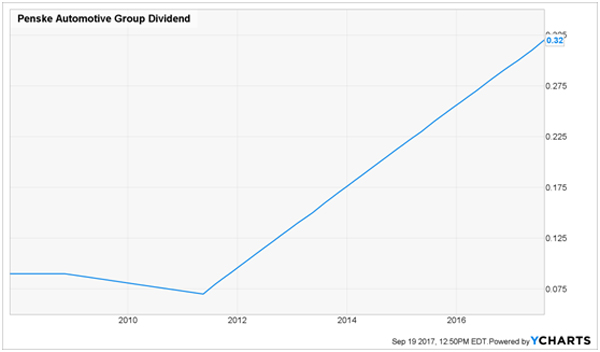

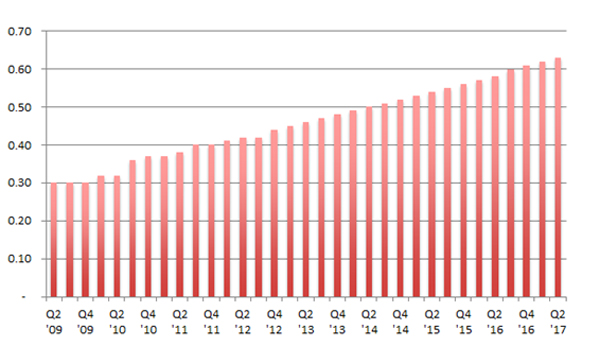

I love management that can shift gears like this. And even if sales do hit a pothole, we’ve got a cushion thanks to PAG’s cheap 10.7 price-to-earnings ratio and its dividend, which yields 2.9% and has risen every single quarter since 2011:

Payout Growth: Smooth Out of the Corner

Which brings me to…

Which brings me to…

Midcap Pick No. 2: A Low-Key Innovator With a 5.8% Payout

EPR Properties (EPR) has cracked the secret to profiting from millennials: sell them experiences, not stuff. The data backs that up: according to a recent study by the Harris Group, that’s where 72% of this generation would rather spend their cash.

EPR is custom-built for trends like this. Here’s a quick overview of the real estate investment trust’s business (which includes 378 locations in the US and Canada):

- Entertainment, including megaplex theaters and entertainment centers.

- Recreation, including ski areas, TopGolf golf-entertainment complexes and water parks.

- Education, including public charter schools and early childhood education.

And those properties are packed. As of June 30, the REIT boasted a sky-high 99.3% occupancy rate. That’s about as high as you can get!

That’s translating into rising funds from operations (FFO; the REIT equivalent of EPS) and lighting a fire under EPR’s dividend. The stock pays a gaudy 5.8% today, but that’s just the start. It pays dividends monthly and grows its payout every year!

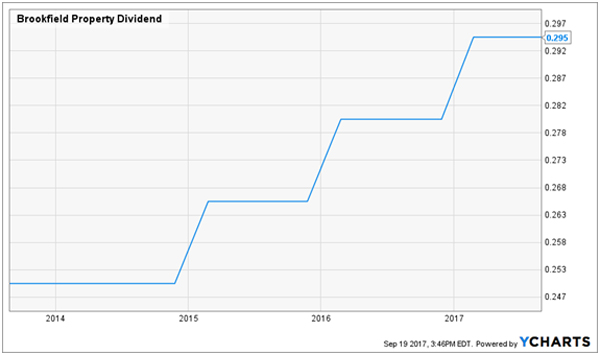

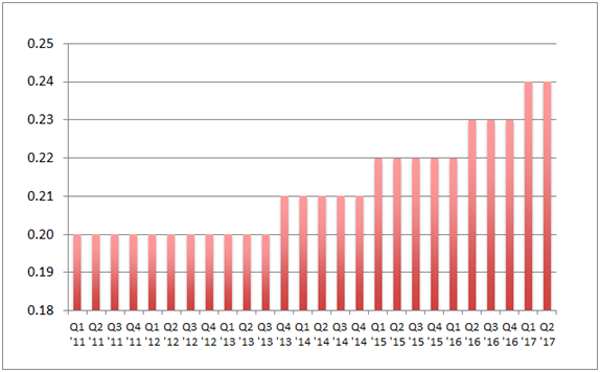

Those hikes have been far from token: last year’s jump came in at 6.25%—and EPR’s payout is accelerating, pulling the share price along with it:

EPR Investors Win Twice

The REIT can easily keep the hikes coming. It paid out 82% of trailing-twelve-month FFO as dividends, easily manageable for a REIT. It also trades at 20.7 times FFO, reasonable for the dividend growth and upside here.

The REIT can easily keep the hikes coming. It paid out 82% of trailing-twelve-month FFO as dividends, easily manageable for a REIT. It also trades at 20.7 times FFO, reasonable for the dividend growth and upside here.

Midcap Pick No. 3: A Global Dividend Star

The last midcap pick I have for you today is Brookfield Property Partners (BPY), which boasts a 5.1% dividend yield and is even cheaper than EPR, trading at just 16.5 times trailing-twelve-month FFO.

Brookfield, whose market cap clocks in at $6.0 billion, is another “jack of all trades,” with malls, office towers, industrial properties, shopping centers and apartments the world over, about 250 million square feet of space in all.

Like EPR, it aims to hand you a nice mix of high yield and dividend growth. We know because management says so, with a stated goal of 5% to 8% yearly payout growth.

So far it’s been true to that pledge: since it was spun off from Brookfield Asset Management (BAM) in 2014, BPY (technically a partnership, not a REIT) has hiked its quarterly payout three times, for an average yearly increase of 5.7%.

Yield and Payout Growth in One Buy

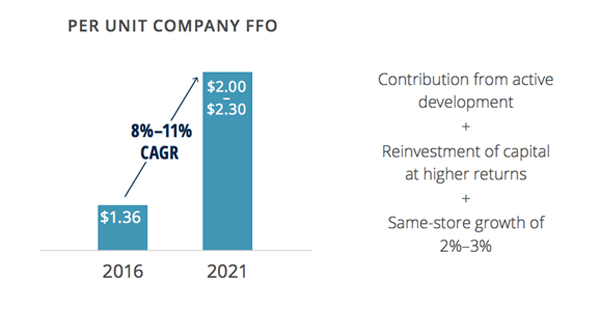

It should have no problem sticking to that promise: the payout is well covered at just 81% of FFO, and management doesn’t see that ratio going higher, thanks to a robust FFO growth forecast:

It should have no problem sticking to that promise: the payout is well covered at just 81% of FFO, and management doesn’t see that ratio going higher, thanks to a robust FFO growth forecast:

Source: Brookfield Property Partners investor fact sheet

Source: Brookfield Property Partners investor fact sheet

The kicker? BPY is a bargain at 16.4 times FFO.

— Brett Owens

Revealed: 2 Hot Midcap Buys for 7.6%+ Yields and 25% Upside [sponsor]

I’ve been encouraging my paid subscribers jump on 2 REITs with bigger upside and fatter yields than you’ll get from either EPR or BPY.

And I want to share those 2 picks with you right now.

One of these undercover REITs recently hiked its dividend again—by 4% over last quarter’s payout. That’s its 20th consecutive quarterly dividend hike!

Dividend Hikes Every Quarter

It pays an 8.1% yield today—but that leaps to an 8.5% forward yield when you consider we’ll see 4 MORE dividend increases in the next year.

It pays an 8.1% yield today—but that leaps to an 8.5% forward yield when you consider we’ll see 4 MORE dividend increases in the next year.

Best of all, this stock trades at a ridiculously low 10-times FFO! When you throw in its relentless dividend hikes you’re looking at an easy 25% GAIN here.

Then there’s my No. 2 pick—a 7.6% payer backed by an unstoppable trend that will deliver growing dividends for the next 30 years!

Lucky shareholders in this company have racked up 86% total returns over the last five years. And now is the perfect time to buy because, just like EPR, its dividend is accelerating!

An Accelerating Dividend

Don’t miss your chance to grab these 2 income wonders before their share prices run away from us, pushing their hefty dividend yields lower as they do. All you have to do is CLICK HERE and I’ll give you their names, tickers, buy prices and my complete REIT investing strategy now.

Don’t miss your chance to grab these 2 income wonders before their share prices run away from us, pushing their hefty dividend yields lower as they do. All you have to do is CLICK HERE and I’ll give you their names, tickers, buy prices and my complete REIT investing strategy now.

Source: Contrarian Outlook