Want to be Target’s (TGT) landlord? You’ll earn more collecting rent from the retailer than you would if you bought shares in the company directly.

How? By investing in the companies that lease space to big box retailers and profit as retail continues its “stealth” recovery. And contrary to what you read in the mainstream press, retail is doing well.

[ad#Google Adsense 336×280-IA]Last quarter, the Census Bureau reported that retail sales were up 8% year-over-year in a quarter when GDP grew just 0.5%.

Picking winners and losers in the retail world is challenging. How do we know if Walmart (WMT) will beat out Costco (COST)?

And what about all those little retail stores that might be gaining market share at the expense of the big boys?

Rather than play retail stock jock, we can instead simply profit from rising demand for office space in increasingly crowded downtown districts across the country.

We do this buy investing in landlords who count Walmart, Costco, Target and many other shops big and small as their tenants. This is possible through something called a triple net lease retail real estate investment trust. A mouthful, yes, so let’s unpack it one step at a time.

REITs (Real Estate Investment Trusts)

REITs, or real estate investment trusts, are a unique kind of corporation that are legally required to invest the vast majority of their assets in real estate. Usually managed by real estate pros, these REITs do all of the property investing, marketing, leasing and management so you don’t have to. Buying a REIT is like outsourcing being a landlord to a management company.

But it’s much better than buying one rental property. For one, these REITs can cut big deals worth millions or billions, thus attracting much better tenants than you can with, say, a condo in a university town. Additionally, REIT managers are trained to find the best value, lowest risk properties, so your risk of renting to a deadbeat goes way down. The best REITs have 99% occupancy rates and nearly 100% of their lessees pay their rent and pay it on time.

Retail REITs

Another key advantage: with REITs you can easily invest in commercial property. And since commercial property is booming right now, REITs are on a tear—many commercial REITs are up 20% or more just this year alone, thanks in no small part to the higher prices of commercial property throughout the country.

With that in mind, let’s think about retail REITs. These are firms that specialize in renting to retailers. I’m talking malls, strip malls, standalone big supermarkets and retail centers.

Triple Net Leases

Commercial real estate is different from residential real estate – mostly in ways that are favorable to landlords. Leases are much longer (sometimes 5 years or more). And tenants will agree to different kinds of arrangements with landlords – one being the a triple net lease, sometimes called a net-net-net lease or NNN.

Here, a tenant pays all real estate taxes, insurance on the building and maintenance fees to upkeep the property. Landlords love this because it lowers their overhead and variable costs when renting properties. Plus, the highest quality tenants tend to prefer triple-net leases because they want more control over the property and how they use it.

My 3 Top Retail REIT Picks

A triple-net lease retail REITs gives us exposure to high-quality retail tenants and high income streams – we now need to consider which ones to pick. There is a large universe to choose from. Here are my three favorites.

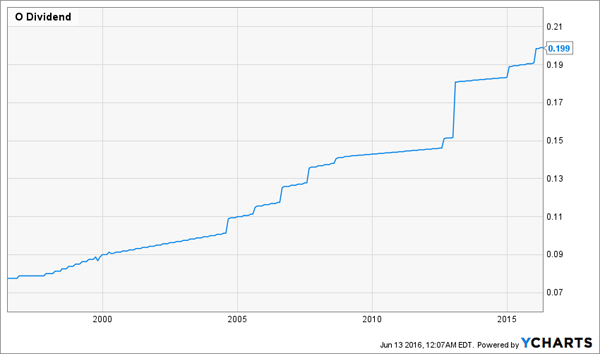

The lowest risk and so far highest reward pick is Realty income Corporation (O), which currently pays a 3.7% dividend. This stock has been loved by retirees for decades for its monthly dividend payment and strong dividend growth history—the dividend has gone up over 150% in the last 20 years, and even kept rising in 2008 and 2009. Since the crisis, the firm’s dividend has grown faster than ever:

Dividend Growth Just Keeps Growing

Realizing how resilient the company is and how strong its income stream is, investors have crowded in. That’s why O is up 25% year-to-date, and some have gotten scared it’s ready to correct. I’m not. Dividend coverage has always been extremely high, and management expects its funds from operations (FFO) to be 119% of its dividend payouts in 2016. That gives O plenty of room to raise its payouts yet again.

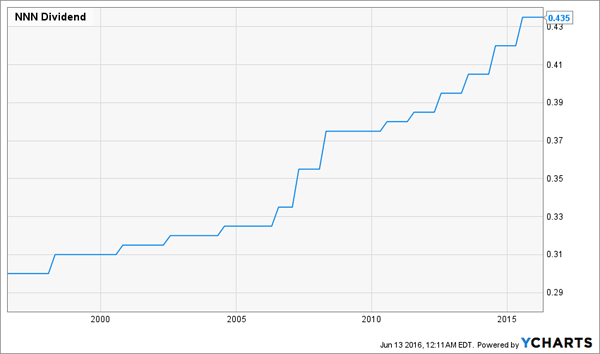

My second pick is even safer, but still gives us a growing 3.6% income stream: National Retail Properties (NNN).

NNN Dividend Sharply Up and To the Right

See those big jumps in income? More are to come. Dividend is covered by over 100% and the company is still expanding operations to get more income from more tenants.

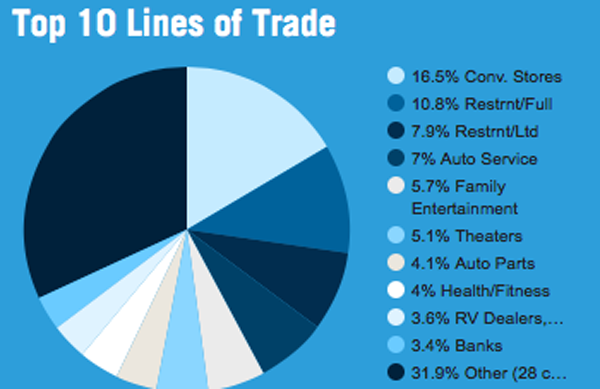

I like this company because it’s huge—with properties in 47 states, the REIT is well insulated from a downturn in one part of the country. I also like NNN because of its blue chip clients: Sunoco, L.A. Fitness, 7-Eleven, SunTrust Bank, AMC Theatre, and BJ’s Wholesale Club are some of the firm’s top tenants, which span many sectors:

NNN Rents To All Kinds of Businesses

The diversification makes NNN low risk; so too does its balance sheet. NNN’s debt-to-equity ratio is 0.4, far below most retail REITs, and management has said repeatedly that their goal is to avoid debt. In the words of NNN CFO Kevin Habicht, “Our balance sheet remains in great position to fund future acquisitions and weather potential economic storms in capital markets.”

In a sector that is commonly funded on leverage, NNN’s aversion to debt – and ability to profit successfully without it – is quite impressive.

For our third retail REIT, we’ll get a bit more daring—and secure a higher income stream at the same time. Lexington Realty Trust (LXP) is another great triple-net REIT, and it yields 7% even after a breathtaking 20% year-to-date jump so far. That big yield is partly because LXP is a little different; they don’t invest in retail properties per se, but instead focus on offices that retailers use.

This is great because LXP is a landlord to Amazon.com (AMZN)—which means if you’re worried about retailers losing to e-commerce, you’re covered with LXP. Plus, Lexington Realty has some other great tenants, like AT&T, Bank of America, Best Buy, Carlson Restaurants, Cummins, John Wiley & Sons, L’Oreal, Staples, Boeing, Kroger and many more.

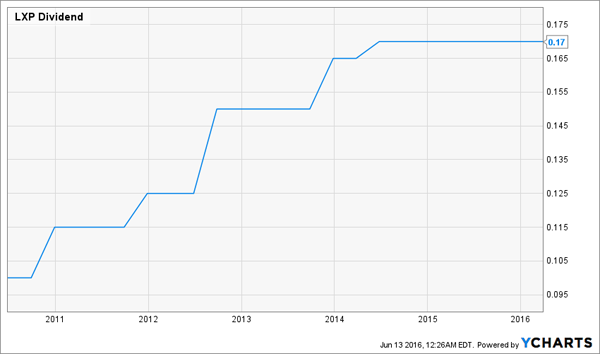

What about the dividend? High yield often implies high risk, but I don’t see it here. While it’s true that funds from operation fell in 2015, the dividend remained amply covered by even the lower FFO; by the end of 2015, FFO was 157% of payouts. Over the last six years, LXP has sharply increased dividends as it recovered from the financial crisis:

LXP Dividend Due for a Jump?

But in the last two years that dividend growth has screeched to a halt. This is in no small part to management’s acknowledgment that FFO was declining, but those drops have moderated since then and the company is still leasing over 96% of its properties to tenants who are current on their leases. Additionally, Lexington has invested over $80 million in ongoing rental projects in the last six months, meaning its income—and shareholders’ payouts—are due to start rising again.

Conclusion

With a portfolio of these three REITs, we get nationally diversified exposure to high quality retail operations and an average dividend yield of 4.8% that is likely to continue growing for years to come. This puts us in a great position to boost our portfolio’s overall income in the short term, while also setting us up for constant income increases as the American economy improves.

— Brett Owens

Sponsored Link: Retail REITs are a great place to start, but why stop there? Other industries offer even more income and greater diversification. For instance, the healthcare space has a number of REITs that may have more growth potential than any other industry in America—including tech! Want to know what’s driving those gains—and how you can take advantage of them with a REIT portfolio yielding over 7%? Take a look at this overlooked but high-reward AND high yield option to rent to aging America.

Source: Contrarian Outlook