Growth at a reasonable price, or GARP, is an investing strategy that blends value and growth investing. Instead of just buying a stock that’s cheap, or one that’s growing earnings fast, we look for stocks that appear decently priced with respect to year-over-year growth.

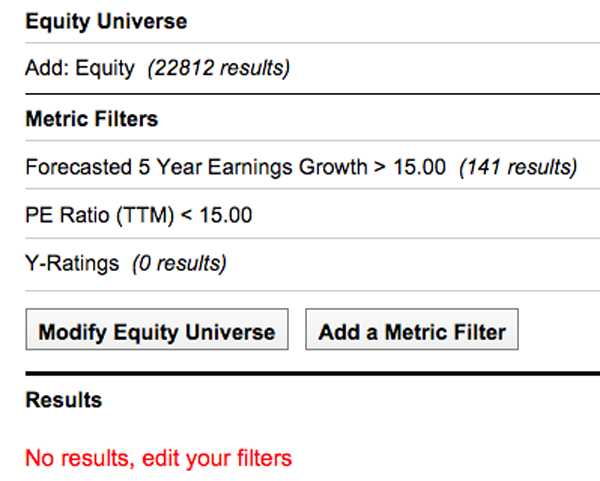

[ad#Google Adsense 336×280-IA]For example, a company growing 15% annually with a price-to-earnings (P/E) ratio of 15 or less would be considered cheap by GARP standards.

Since the “E” is growing at 15% per year, the P/E next year will either decline towards 13, or the stock price will rise in tandem with earnings.

It sounds like a foolproof investing formula.

Problem is, everyone knows it is.

Which is why there are exactly ZERO stocks in the universe that have a P/E below 15, and earnings growth above 15%, according to YCharts.

Sorry… Sold Out of GARP

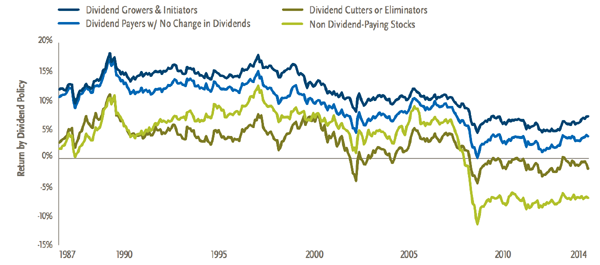

Now all is not lost – there is a proven way to make money buying growth. According to Ned Davis Research, 80% of the total return of the S&P 500 since 1960 can be credited to the compounding and reinvestment of dividends.

Now all is not lost – there is a proven way to make money buying growth. According to Ned Davis Research, 80% of the total return of the S&P 500 since 1960 can be credited to the compounding and reinvestment of dividends.

Since 1987, perennial dividend growers have returned 10.1%. They’ve outperformed static dividend payers, non-dividend paying firms, and dividend cutters or eliminators.

Dividend Growers Outperform, Returning 10.1% Annually

The key takeaway here is that it’s good to buy a dividend, but even better to buy tomorrow’s higher payout today. I’ll share my three favorite “dividend growth at a reasonable price” plays in a minute. These are fast growing payouts selling for cheap.

The key takeaway here is that it’s good to buy a dividend, but even better to buy tomorrow’s higher payout today. I’ll share my three favorite “dividend growth at a reasonable price” plays in a minute. These are fast growing payouts selling for cheap.

But first, let me warn you about three stocks that appear to fit the “D-GARP” criteria on paper. Their current payouts aren’t as secure as investors believe, however, because they’re funding them with borrowed money.

3 Dividend Growth Stocks to Sell Now

Asset manager Blackstone Group (BX) sure prioritizes its dividend. Shares currently yield 8.9%. Unfortunately, that’s not sustainable, as Blackstone has paid out roughly 37% more to shareholders ($2.73 per share) that it generated in free cash flow ($1.97 per share) over the past twelve months.

As I cautioned in November, you don’t want to own firms like Blackstone when credit markets are shaky. Shares are down 19% since my original warning, during which time competitor KKR (KKR) cut its payout by more than 50%. Historically the best time to buy these issues is after a credit collapse (see: 2009) – not before, or during.

HSN (HSNI) has a business model straight from the 1990s – selling random products on cable television. The internet is starting to catch up with HSN, with its payout ratio ballooning to 353%. Sales have started to decline as well.

The company won’t be able to pay its dividend, let alone grow it, without a new business model. But HSN doesn’t have any money leftover for a much needed acquisition to help “pivot” to a more modern focus.

Finally Las Vegas Sands (LVS) has nearly tripled its dividend since 2011, with shares currently yielding 5.6%. Unfortunately, the company is taking on debt to fund its payout, which is now 138% of earnings.

CEO Sheldon Adelson is gambling on a rebound in Macau to not only save the day, but also spur on future payout increases. That may eventually happen, but in the meantime I’d rather bet on surer things – like these three companies…

And 3 Dividend Growth Stocks To Buy & Hold

My 3 favorite “D-GARP” stocks have business models well suited for 2016 and beyond. Their current dividends are well funded by free cash flow, and payout growth should continue in tandem with rising profits for at least the next 5 years.

Boeing (BA) pays a 4% dividend today. The last time it paid this much was July 2009, after the last panic in the markets. If you had bought it then, you’d have made 230% since. This is why panics must be bought rather than sold.

This time, it’s no different. “First-level investors” are worried that emerging market problems are going to dampen demand for Boeing’s planes. This allows the company to use the pullback to repurchase cheaper shares. In January, it increased its authorization $7.25 billion, which would retire nearly 10% of outstanding shares at today’s prices.

The 4% dividend is well supported by the company’s manageable 48% payout ratio. Add in the 10% share reduction under the current buyback program, and shareholders are receiving a net payout of 14% this year!

Utility Edison International (EIX) boasts expected rate base growth of 7-8%, which is well ahead of the industry average of about 5%. Since 2005, Edison has doubled its dividend – with an increase of 35% in the last two years alone!

Its 39% payout ratio is still low for a utility. Edison is targeting a 45-55% payout ratio – which means its 3% yield has plenty of room to keep moving in the years ahead.

Its 39% payout ratio is still low for a utility. Edison is targeting a 45-55% payout ratio – which means its 3% yield has plenty of room to keep moving in the years ahead.

— Brett Owens

Sponsored Link: My favorite dividend grower already pays a gaudy 6.8% today. And it increases its payout not just every year, but every single quarter. If you buy shares today, you’ll be earnings a 10%+ cash yield on your initial investment in no time.

Best thing is, this company’s business model is bulletproof. You see, no matter what happens to the price of oil, the outcome of this year’s election, or even China or the Fed, there’s one sure economic bet in America:

The country will be older in the future than it is now, and demand for healthcare services is set to skyrocket.

In fact, by 2024, national healthcare expenditures are expected to climb to $5.43 trillion, or about 20% of GDP. This firm is capitalizing on this trend, and growing its already-big 6.8% dividend literally every 3 months. Plus, shares have easy 20% upside from here or better, as they’re trading for just 10-times cash flow.

Source: Contrarian Outlook