Steelmakers have been under fire over the last 18 months. Nucor Corporation (NYSE: NUE) has not been an exception.

North America’s largest steel producer and recycler has suffered from the worldwide steel industry downturn. Prices for steel have collapsed as companies subsidized by foreign governments have dumped their goods into the U.S. market.

[ad#Google Adsense 336×280-IA]Steel is a notoriously volatile business.

Prices go up and down with supply and demand.

While many of Nucor’s competitors have fallen into bankruptcy, Nucor has survived and even thrived by keeping its costs in check.

It is one of the lowest-cost American producers.

At the same time, Nucor has managed to reward its shareholders.

The company has paid a dividend since 1973 and has raised it for 43 consecutive years. That track record is not too shabby!

Right now, though, sentiment is negative. Nucor’s stock price is down 31.55% from its peak in September 2014. It has been a painful ride for shareholders. Thank goodness the dividend has helped ease some of the sting of the price decline.

But will investors be able to count on the dividend stream in the future?

In 2015, Nucor generated $1.78 billion in free cash flow. That is a whopping 164% increase over the prior year. Since 2012, Nucor’s free cash flow has gone up 605%. The triple-digit increases are impressive on their own, but even more so considering the steel industry environment.

The company’s efficiencies and efforts to control costs are paying off.

However, steel prices are not expected to improve in 2016. The market remains challenging.

This year, analysts predict Nucor’s free cash flow will decline 45% to $975.1 million. It looks like it will be a temporary blip. They assume the company’s free cash flow will resume its climb in 2017.

The company brings in more than enough cash to cover its dividend obligations. In 2015, Nucor paid out $479.43 million in dividends. The company’s payout ratio, dividends to free cash flow, was just 26.34%. This year, the Street is expecting a miniscule increase to $480.38 million.

Even with the decline in free cash flow, Nucor still sports a comfortable 49.26% payout ratio. The low payout ratio gives the company plenty of room to keep up with the dividend even if free cash flow dips further than expected.

“The finest steel has to go through the hottest fire.” – Richard M. Nixon.

The steel industry has never been an easy business. It is highly cyclical and correlated with economic growth. Foreign competition flooding the market has made it even worse. However, Nucor and its dividend have proven they can weather the storms.

With its impeccable history of paying dividends, rising free cash flow and more-than-manageable payout ratio, investors should not have to steel themselves for a dividend cut.

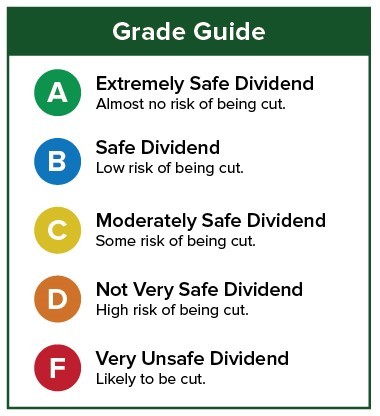

Dividend Safety Rating: A

Good investing,

Kristin

P.S. Want to know about other rock-solid dividends like Nucor’s? Check out Safety Net Pro to see the safety ratings of nearly a thousand dividends. Browse by grade, industry and market cap – and never again be surprised by a dividend cut.

[ad#mmpress]

Source: Wealthy Retirement