As hard as it is to believe, we’re headed full speed into the end of 2015. That means now’s a perfect time to discuss one of the most powerful investment tactics of all.

Before I tell you what it is though, let me say that the tactic we’re going to discuss today is something many investors believe they know a lot about. Yet, in practice, very few actually get it right.

[ad#Google Adsense 336×280-IA]That’s sad because “it” can significantly boost your returns and reduce your losses – all while taking less than 90 seconds of your time.

Ready to get started?

Here’s How to Maximize Profits Immediately

People ask me all the time how much time they have to put into investing to make the process “worth it,” and they nearly fall over every time I answer…

…about 90 seconds.

That’s about how long it will take you to “rebalance” your portfolio.

If you’ve just joined us, rebalancing is one of the single most powerful yet easy-to-use strategies available to individual investors today for five simple reasons:

- You can do it anytime.

- You can lock in profits immediately.

- You minimize risk every time you rebalance.

- You maximize upside potential for years to come.

- You can do it easily… in about 90 seconds.

Simply put, rebalancing is a strategy that ensures your money is working the way you want and, perhaps most importantly, is aligned with your individual risk tolerance, objectives, and financial aspirations.

Here’s How Rebalancing Works

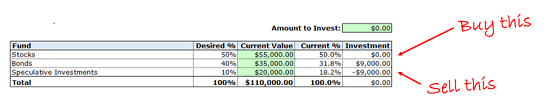

Let’s say you have a $100,000 portfolio that’s invested 50%-40%-10% in stocks, bonds, and speculative investments, respectively. That means you’d have $50,000 in stocks, $40,000 in bonds, and another $10,000 in speculative investments.

A year from now, let’s suppose that stocks have appreciated 10% and bonds have lost 12% because the U.S. Federal Reserve got aggressive. Let’s also say you hit the big time with your speculative play and that it’s up 100%.

That means your $100,000, 50-40-10 portfolio would now be worth $110,000 and the allocation would be more like 50%-31.8%-18.2%.

To get back to your targeted 50-40-10 risk profile, you’d rebalance by selling $9,000 worth of your speculative investments and buying a corresponding $9,000 worth of bonds using the proceeds, assuming you had no new money to invest.profitable 2016

This is where most investors go off the rails.

This is where most investors go off the rails.

They don’t see a problem with letting their winners “ride.” That’s fine if you’re in a Las Vegas casino and want to leave your money on the table even as you continue to bet you won’t lose it, but that strategy is totally unsuited to today’s financial markets. Every dollar you earn if you don’t rebalance means you’re taking on more risk.

Source: Fidelity Investments

Source: Fidelity Investments

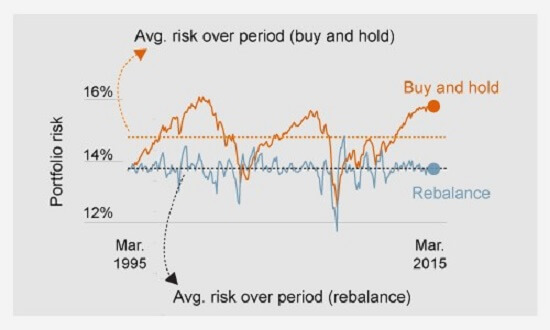

This is where many investors found themselves coming into the dot-bomb crash of late 1999/2000 and the Financial Crisis of 2008. They thought they were doing great. What they didn’t realize was how concentrated their risk was becoming… in the very stocks that were making them gobs of money.

You can see that very clearly in orange. Note how much higher the risk associated with letting things ride became in 2000 and in 2007… right before the bottom fell out and they got shellacked. Contrast that with the much lower risk of a constantly rebalanced portfolio in blue.

Let’s get back to our example.

Every day you’re not in the markets is a day of lost opportunity, which is why we’ve talked about the importance of constantly investing – in good times and in bad.

Invest for one day and you’ve got approximately a 54% probability of making money in the stock markets. Invest for a year and that number jumps to around 68%. But leave your money alone for a full decade and the probabilities rise to a smile-inducing 87%, according to Dan Wiener and Jeff DeMaso of the Independent Advisor for Vanguard Investors, who based their analysis on returns from 1927 to 2014.

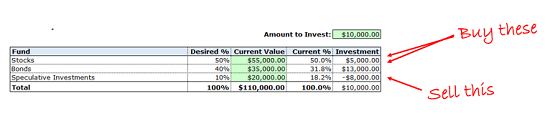

So let’s rerun those numbers assuming you’re going to add an additional $10,000 to your investments as you rebalance.

That means you’ll be buying $5,000 more stock, buying another $13,000 worth of bonds, and selling $8,000 worth of speculative investments to get back to your perfect 50-40-10 portfolio allocation.90-second strategy

The thinking here is pretty simple. Rebalancing ensures you are capturing profits and buying more of whatever’s on sale. Over time this can significantly reduce portfolio volatility AND boost your returns.

The thinking here is pretty simple. Rebalancing ensures you are capturing profits and buying more of whatever’s on sale. Over time this can significantly reduce portfolio volatility AND boost your returns.

This Strategy Can Really Boost Your Returns

By how much?

There’s extensive research showing that the advantage can be anything from a few percent a year to 300% or more over time. The answer, like many things, depends on your personal circumstances, the time you leave your money invested, and how you’ve allocated it.

But, and this is very important, the principles are the same no matter how much or how little money you have in play. That’s why rebalancing is so very important to understand and to get right.

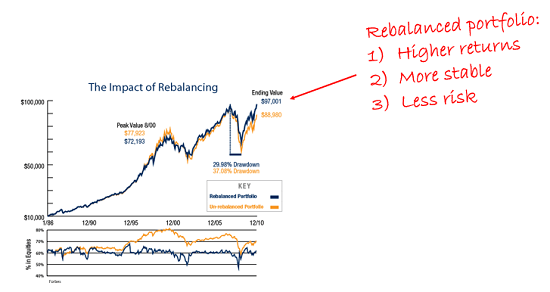

Here’s a study from Forbes highlighting the performance of two hypothetical $10,000 portfolios starting in 1985 and ending in 2010. Both use a 60/40 mix of stocks and bonds based on the S&P 500 Index and the Barclays Aggregate Bond Index. The only difference is that the blue portfolio was rebalanced annually while the orange portfolio was never rebalanced.

As you can see, the rebalanced portfolio was worth just over $97,000 at the end of the study. That’s a total return of 870%. The un-rebalanced portfolio was worth only $88,980 and resulted in a total return of 789%.profitable strategy

Here’s the real kicker, though…

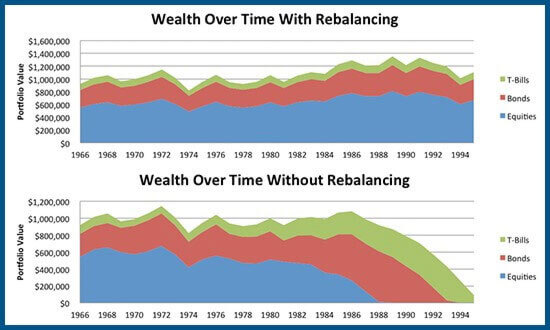

Let me show you what can happen when you don’t rebalance. This catches a lot of people by surprise.

Source: Kitces.com

Source: Kitces.com

Put very bluntly, not rebalancing periodically is so damaging that it can lead to dramatically worse results over time even if there are other investment decision rules in place, according to my research and that of Michael Kitces, a partner for Pinnacle Advisory Group, a private wealth management firm overseeing more than $1.8 billion of client assets.

Are there some wrinkles?

Sure.

For one thing, there’s more than one way to rebalance.

I’ve highlighted a simple percentage-based method today, but you could introduce variables related to trade risk, trading method, parity, or any number of other institutional-grade concepts if you wanted. For all but the most sophisticated individuals, that’s overkill.

The key to rebalancing successfully is to: 1) use predetermined thresholds like the 50-40-10 I advocate in the Money Map Report and 2) rebalance consistently when it gets out of line.

For another, there’s a lot of debate about how often to rebalance.

I think keeping things simple is easiest and most effective. Very few investors have the discipline needed to realign their holdings monthly or even quarterly. That’s why I’m a big fan of picking a date you’ll remember like your birthday and rebalancing annually.

There can be tax considerations, too.

That’s why, if possible, you want to rebalance within retirement accounts or using tax-advantaged investments to avoid paying Uncle Sam any more than you legally have to. You can always work with a financial advisor or accountant to combine rebalancing with tax-smart moves that pair gains with losses that are then applied against realized capital gains or ordinary income.

In closing, let me leave you with a thought.

There are a lot of people who believe that the markets are high and that, therefore, there’s nothing to buy. Don’t fall for it.

The risks of a correction may be mounting, but that’s why rebalancing is so very powerful.

Because then you’ll know exactly what to buy no matter what happens next.

— Keith Fitz-Gerald

[ad#mmpress]

Source: Money Morning