Don’t believe every contrarian you read on the internet – not all REITs have interest rate risks sufficiently priced in.

Two weeks back, I highlighted the good performance that REITs turned in during the last rising rate period from June 2004 to June 2006. The Vanguard REIT Index ETF (VNQ) hardly suffered as rates rose from 1% to 5.25%, returning 33% over the 24-month period.

[ad#Google Adsense 336×280-IA]Some REITs didn’t do as well, however.

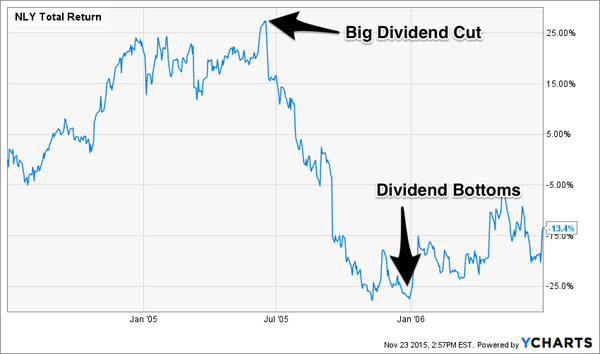

Mortgage REIT favorite Annaly Capital (NLY) posted a total return (dividends included) of -13.4%.

If you own similar issues like Redwood Trust (RWT), Capstead Mortgage (CMO), or MFA Financial (MFA) then please pay attention.

Annaly is a well-run company that we’re going to use as our historical case study thanks to its track record through a few interest rate cycles.

The “original mortgage REIT” suffered through 2004-06 because it holds fixed-rate securities that decline in price when rates rise. This crushed Annaly’s income, which in turn crushed its dividend (it dropped 80% in just one year).

Some hopefuls are arguing that today, the prospect of rising rates may already be priced into shares of mortgage REITs. But interest rates aren’t the threat – the ensuing payout cut is.

And despite the stock market’s reputation as a “forward-looking vehicle” it didn’t price anything into Annaly shares until it actually cut its dividend by 20% in June 2005. Share prices bottomed exactly when the dividend bottomed at $0.10 per share (down from $0.50 a year earlier) in December 2005.

Higher Rates Didn’t Hurt Annaly Until It Had To Cut Its Dividend

It’s actually pretty easy to time good entries and exits to and from mortgage REITs. When dividends are steady or rising, they’re good buys that pay double-digit yields.

But when dividends are falling, or in danger of doing so, they’re time bombs with short fuses that put several years worth of dividends at risk. Let’s look at a few historical examples.

From December 2002 to October 2003, Annaly’s dividend slid off a slow, brief cliff from $0.68 per share down to $0.28 per share. Investors lost 7.8% in nine months.

Annaly Investors Do Alright Until The Big Dividend Cut

Our 2004-06 example looks even more drastic when we isolate the specific dividend cuts. Once again, investors were willing to tolerate rising interest rates and a slightly declining dividend. But they bailed when the dividend cuts “got real.” Total returns were -40% for the year that saw the dividend drop 80%.

The 2005 Dividend Goes Off The Same Cliff As Share Prices

Since then, it’s been mostly good times for Annaly investors. The dividend climbed from its $0.10 bottom to a peak of $0.75 in December 2009. The stock has delivered a 167% total return in the last decade.

However most of that return (140% of it) came in the rising dividend period of 2006 through 2009. From June 2011 to December 2013, Annaly lowered its payout by more than 50% and delivered investors a total return of -26.4%.

If you own Annaly, Redwood, Capstead, MFA, or any other mortgage REIT today, your big risk is not interest rates themselves. Rather, it’s the actual dividend cut that’s likely to turn your double-digit yield into double-digit losses.

This is a fine point, but an important one – just ask any mortgage REIT investor from years past who got them mixed up.

And sure, some of these REITs are smartly working to diversify. Annaly for one is quite excited about its budding commercial business.

It still only represents 15% of the company’s total equity, but could provide hope as a buffer from future rate cycles.

However, rates are likely to rise – if only a little. Which means these dividends are likely to get cut – with share prices likely to slide in tandem, and wipe out the yields plus some.

For now, I’d steer clear of these mortgage traps and would instead consider a trio of healthcare REITs. These companies going to keep making money no matter what interest rates do, as they’re capitalizing off a huge shift in U.S. demographics – the aging baby boomer population.

These REITs are paying 6.6%, 7.3%, and 7.5% respectively – and unlike their mortgage cousins, these issues are likely to continue increasing their dividends annually.

— Brett Owens

This 7.5% Dividend Is About to Double [sponsor]

I’ve uncovered a recent spin off tapping into the aging baby boomer profit tsunami. It pays 7.5% today and the yield is expected to double fast. Recent pullbacks have created the perfect buying opportunity just in time for the next dividend payout. Click here for the name of this stock and the Billionaire’s Secret we used to find it…

Source: Contrarian Outlook