The last time this happened, municipal bonds soared 40% over the next 12 months.

These usually-steady payers are coming off their worst month since September 2008, according to Standard & Poor’s, when its “muni” index dropped 4.8% (and popular funds fared even worse):

The Last Muni Bloodbath in Sept 2008…

October 1, 2008 didn’t mark the bottom for munis. But it turned out to be a pretty good time to buy, with these funds returning up to 38.4% in the ensuing 12 months!

… Gave Way to This 12-Month Muni Boom

Those were scary times. The financial world was melting down, and prominent pundits feared that municipalities would be the next wave of defaults.

These pundits were, of course, dead wrong. Munis have actually been the safest bonds you could have purchased this side of U.S. Treasuries.

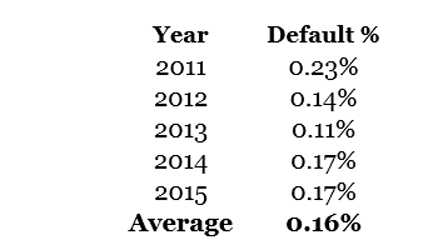

The S&P Municipal Bond Index tracks over 79,000 bonds from over 22,000 different issuers.

Over the last five years, it’s recorded a default rate averaging just 0.16%:

Only 0.16% of Muni Bonds Defaulted Recently

This Time, “They” Are Worried About Inflation and Taxes

Munis were quite popular as recently as summer. Yields on the four Nuveen funds I highlighted earlier were sitting at or near five-year lows – a sign of endearment:

Muni Fund Yields Spike Off Lows

A couple of things triggered their recent selloff.

[ad#Google Adsense 336×280-IA]First, the 10-year Treasury yield rose a full percent – from 1.4% to 2.4% today.

And then Trump won the election.

His tax plan should benefit high earners, with the top Federal rate projected to drop to 33% (from 39.6%).

Which means rich guys won’t derive as much in tax savings from munis as they do today.

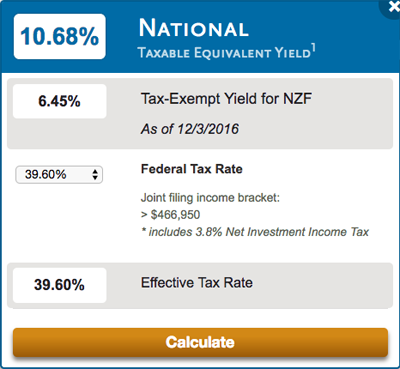

Most muni bonds are Federal tax-exempt.

Which means a 6.5% paying fund like the Nuveen Enhanced Municipal Credit Opportunities Fund (NZF) actually pays top-bracket earners a 10.7% tax equivalent yield!

A 10.7% Tax Equivalent Yield

Trump’s cuts wouldn’t derail this tax-efficient gravy train much, however. A 33% tax bracketer will still enjoy a 9.6% equivalent payout from a fund like NZF today.

What If Rates Really Climb?

Believe it or not, munis and long-term rates haven’t always had an inverse relationship. Last decade, they actually co-existed peacefully and tended to move in tandem:

Munis and Rates Haven’t Always Disagreed

This traditional relationship should eventually resume. If the 10-year yield (somehow) rolls towards 5% or 6%, municipalities will have to pay more to fund their projects. But their premiums should be modest, thanks to the tax benefits they provide.

The prices of fixed-rate bonds are suffering, however, as rates rise. This may not matter to someone who holds an individual muni issue with no intent to sell. But a fund that pays out its capital gains as part of its distributions to investors can no longer do so.

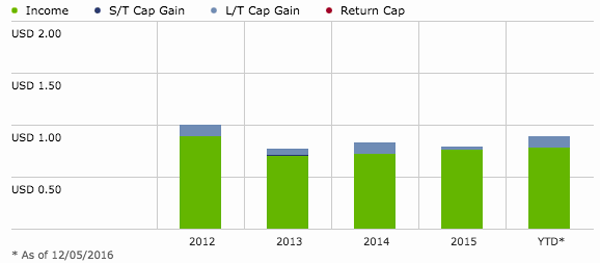

Last week, Nuveen announced modestly lower distribution levels for several of its funds in December versus November. At a glance, the cut is curious for a fund like NVG, which has actually netted more investment income this year than last. But it’s the blue icing on top, long-term capital gains, that is under pressure:

NVG Income Actually Ahead of Last Year’s Pace

A Tax-Efficient Contrarian Opportunity

For a secure investment, muni bond prices sure can swing wildly. Which is exactly why they provide us with such stellar buying opportunities.

In a sane world they would always trade at modest yield premiums to Treasuries. But I prefer to buy them now, when they are paying 7% to 8% more (in taxable terms) than T-Bills. An insane premium.

Plus, the best time to buy a fund or stock is often immediately after a distribution (or dividend) drop. It sounds counterintuitive, but managers prefer to cut just once. Which means Nuveen likely overshot the mark to stay on the safe side.

These income streams are secure, with no major credit risk. And portfolio managers will soon be able to buy higher paying issues to better compete with the 10-year.

Trends in interest rates do tend to stay in motion, and it’s impossible to call a top in yields (or bottom in munis) without the benefit of hindsight. But we contrarians make our money buying when nobody else wants to – and the last time munis were this hated, they returned 30-38% over the next 12 months.

— Brett Owens

More 8% Retirement Plays [sponsor]

The beauty of these types of secure high yields is that you can “ride out” any price fluctuations, because when you live off dividend income alone you never have to actually sell anything.

That’s why I recommend a full “no withdrawal” portfolio of secure 8% payers. There are actually safe funds and stocks that pay this much. They don’t get a lot of coverage in the mainstream financial media because most investors are distracted by big blue chip names. Problem is, this popularity comes at a price – and you can’t live off dividend income alone if you’re only banking 2% or 3% in yield.

The solution? Stealth plays like closed-end funds, preferred shares and recession-proof REITs. You can build a safe, diversified portfolio from these types of issues that pays 8% – which means you’ll never have to lose sleep over price gyrations again.

Want to learn more – and buy a few high paying shares? Click here and I’ll share everything about my “no withdrawal” strategy, including the names and tickers of the stocks and funds that you can buy for secure 8% yields.

Source: Contrarian Outlook