If you feel trapped grinding out dividend income at 3% or so, listen up. The Fed’s latest “no hike” call has provided big 7% to 9% yields with the “all clear” signal for another year or two, at least.

In a world where a million bucks worth of dividend aristocrats will only net you about $29,000 annually, you’re probably looking for higher yielding options.

[ad#Google Adsense 336×280-IA] Some closed-end funds (CEFs) paying up to 9% can be good candidates – if you choose wisely.

You’re probably familiar with their mutual “cousins”.

Closed-ends are a bit different. While mutual funds tend to buy individual stocks and mirror the market, CEF managers tend to have wider mandates and longer leashes.

A top CEF manager takes advantage of this flexibility to generate alpha.

He might buy safe sovereign debt in Australia when investors are scared of Asia altogether, and lock in secure 6% yields. Or he might buy preferred shares issued by JPMorgan paying 6.1% annually – a deal not available to an individual investor like you or me.

A savvy closed-end manager can even borrow cheaply and juice returns. CEFs borrow at rates tied to Libor (the London interbank offered rate) – good living today with the international benchmark at just 0.86%. The “spread” turns already good yields into great ones.

As you’d expect, it’s been a banner year for many closed-end funds. But investors are worried the party may be ending soon as rates creep higher. They’re wrong for two reasons.

First, Rates Aren’t Going That High

The smart money is torn on whether or not the Fed will (finally) hike again in December. But looking ahead to next year, few traders believe we’ll see more than one measly hike by this time next year.

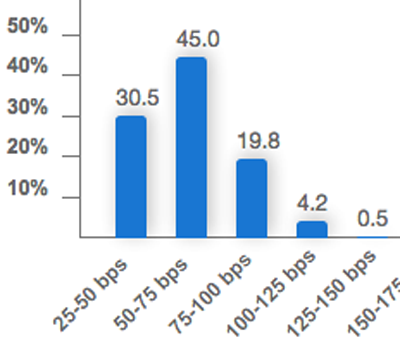

Here’s a look at the Fed Fund futures markets – where real money is being bet – for the September 2017 meeting. Three-quarters of traders are wagering on a maximum of one hike between now and then:

75% of Traders Bet No Hike or One Hike

The Fed says it’s going to hike twice next year, but traders are finally calling nonsense. In either scenario, borrowing costs for CEF managers will stay low.

Plus, It Doesn’t Matter Anyway

In June 2004, Fed chair Alan Greenspan began boosting rates from then-historic lows. Over a two-year period, he increased the federal funds rate from 1% to 5.25%. An earthquake.

How’d CEFs perform? I checked the historical performance of three prominent funds – they all outperformed the market during Greenspan’s aforementioned run:

Higher Rates No Problem for Top Closed-Ends 2004-06

With the “all clear” signal officially up for CEFs, which should you consider? Only those that meet these two criteria.

Demand a Discount

One aspect of the CEF structure lends itself perfectly to contrary-minded investing – fixed pools of shares.

Mutual funds issue more shares whenever they want. But closed-ends have a fixed share count, with their funds trading like stocks. As a result, from time-to-time a fund will fall out-of-favor and find its shares trading at a discount to its net asset value (NAV).

This is basically “free money” because these underlying assets are constantly marked to market. If a fund trades at a 10% discount, management could theoretically liquidate the fund and cash out everyone at $1.10 on the dollar immediately. Or it can buy back its own shares to close the discount window (and boost the share price).

Premiums, on the other hand, are rare in the closed-end space, and usually reserved for “rock star” managers and hot ideas. PIMCO’s funds would often trade at a premium when “Bond King” Bill Gross was running the show. In fact, three still do trade at double-digit premiums, with the most excessive at 48% today!

Yes, you read right – there are people who pay $1.48 for $1.00. Personally I prefer not to be down big out of the gate.

I demand a discount when I buy closed-ends, and so should you.

Then, Look for Alpha

Visit the homepage of any CEF you’re considering. Read through the most recent reports and the letters from management, and figure out if their strategy is adding value or just paying their own salaries.

There’s an easy way to verify – check the track records. Funds have histories, as do their managers. Look at both.

To check a fund’s track record, use the “total return” calculation, which includes dividends – this is important because most of the gains from CEFs come in the form of payouts.

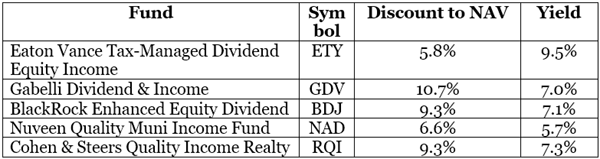

Five Alpha-Worthy 5% CEF Yields (at Big Discounts, Too)

Here are five CEFs that meet our initial criteria. They all:

- Pay 5% yields or better.

- Trade at 5% discounts or more.

- Have returned 50% cumulatively or better over the last five years.

Steady Gains From These Still-Cheap CEFs

— Brett Owens

Sponsored Link: A deeper understanding of both the stock and bond markets and the funds that provide these high incomes is necessary to building a strong, high-yield portfolio without with high risks. Billionaire investors are doing this right now—but you don’t have to be a billionaire yourself to follow in their footsteps.

“Bond God” Jeffrey Gundlach has been pounding the table over a particular group of funds that currently trade at significant discounts to net asset values and pay 8% yields—or more—simply because most people don’t know they exist. Click here to find out why Gundlach is so bullish on these funds and discover [more information on] my top three plays.

Source: Contrarian Outlook