I just got back from the 2016 MLP Investor Conference in Orlando.

The crowds were much smaller than they were at last year’s conference. By my count, there were at least 25% fewer master limited partnerships (or “MLPs”) presenting this year.

[ad#Google Adsense 336×280-IA]And that makes sense – companies had to decide if they were attending the conference months ago.

Back in February, oil bottomed near $27 a barrel… and things looked gloomy.

But things have changed. Oil prices have nearly doubled to around $50 a barrel.

Today, I’ll share what I learned at the conference… and why you should consider buying a certain group of high-quality MLPs…

Regular Growth Stock Wire readers are familiar with MLPs. These companies own and operate pipelines and storage tanks that are used to process, store, and transport oil and gas.

Because of its structure, an MLP doesn’t pay corporate taxes. In exchange, it pays out most of its earnings to investors in the form of “distributions” (its version of a dividend). These big distributions make MLPs popular income investments. (Of course, because of their unique structure, you should talk to an accountant before investing in one.)

But I saw something at the MLP Investor Conference that caught my eye: Despite what most people think, some MLPs are largely immune to swings in oil prices.

I went to a presentation from Dr. Grant Sims, chairman and CEO of Genesis Energy (GEL). Like many MLPs, Genesis has fixed-fee arrangements on its pipelines with the oil producers that use it to ship their products. As such, the company’s finances are less susceptible to moves in oil prices and more influenced by the volume of product moving through its pipes.

Sims’ company is also more diversified than many MLPs. In addition to its offshore pipelines in the Gulf of Mexico and onshore pipeline segments, Genesis offers refinery services, marine transportation, and supply and logistics. Genesis provides more offshore and refinery services than a pipeline company that simply ships crude oil.

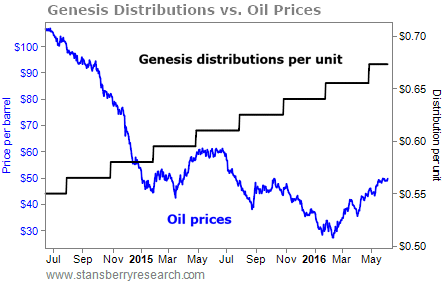

Genesis’ finances show its limited exposure to oil prices. From 2013 through March 2016 – as oil prices bottomed – the company’s earnings before interest, taxes, depreciation, and amortization (“EBITDA”) doubled.

Meanwhile, Genesis has raised its distribution 43 quarters in a row. The MLP paid out nearly 11% more per unit in 2015 than it did in 2014, despite tumultuous oil prices. At the current pace, the distribution will rise another 10% this year…

And Genesis’ EBITDA and operating cash flow per unit is higher over this period, too. Because MLPs pay out most of their income to investors, they regularly sell units or raise debt when they need money. That’s why it’s important to see growth on a per-unit basis (as well as reasonable debt levels). We need to know these companies are investing the additional funds profitably.

According to Bloomberg, Genesis is in elite company. Only 10 other MLPs saw their per-unit earnings increase and sported debt levels of less than 50% of their enterprise value. Here are the six largest…

Long-term investors who listened to Sims knew they were in better shape than oil prices over the past couple of years. The company’s wide variety of products and services shielded investors from the drop in oil prices. And today, Genesis units are moving up even faster than oil prices, nearly doubling from their February lows.

That trend should continue. Consider buying these names today.

Good investing,

Brian Weepie

[ad#stansberry-ps]

Source: Growth Stock Wire