Business development corporations (BDCs) are a great addition to a high-yield portfolio. With yields over 8%, and sometimes even over 10%, these companies provide a strong income stream right now, and can bolster the overall yield of your portfolio.

But BDCs can be dangerous. Because they are legally required to return 90% of their income to shareholders, and because they regularly issue a lot of new shares to expand operations, capital gains are rare in these asset classes and dividend cuts are common.

[ad#Google Adsense 336×280-IA]BDC investors need to carefully track how companies’ net investment income (NII) is trending, because they use NII to fund payouts.

If NII falls below the dividend, a cut to payouts is likely.

This happened early last year with Prospect Capital (PSEC).

PSEC had been an investor favorite for years, having survived the global financial crisis of 2007-2009 and slowly increasing payouts for years.

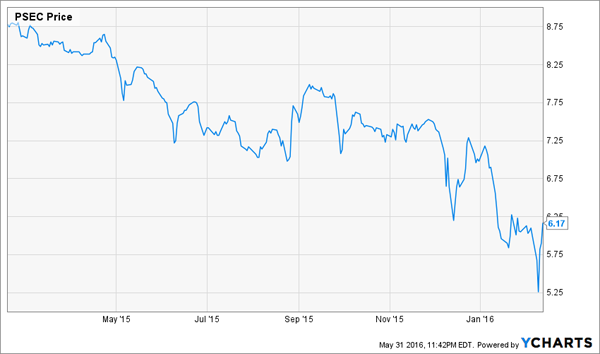

Then, in February of 2015, management cut its dividend by 25% and the stock fell steeply for months afterwards:

Dividend Cut Also Cut Prospect’s Price

The stock has recovered since then, thanks in part to a steep discount to the company’s net asset value (NAV). However, the NAV fell 6.7% on a year-over-year basis last quarter, and many analysts are expecting further NAV declines in the future. Still, at a 22% discount, some think those declines are already priced in.

The stock has recovered since then, thanks in part to a steep discount to the company’s net asset value (NAV). However, the NAV fell 6.7% on a year-over-year basis last quarter, and many analysts are expecting further NAV declines in the future. Still, at a 22% discount, some think those declines are already priced in.

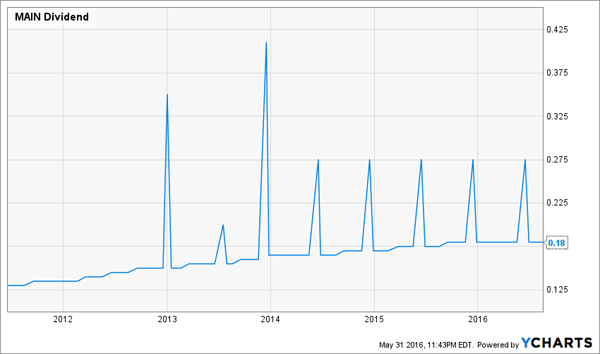

A BDC With No Cuts

Investors might want to look for BDCs that have never cut their dividend. There is one: Main Street Capital (MAIN), which IPO’d in 2010 and has actually increased dividends 44% since while paying frequent big special dividends. The stock has also returned incredible capital gains: 93% since IPO.

Main Street Payouts Keep Rising

Capital gains aren’t really where it’s at with BDCs, though. Buying and holding quality BDCs will secure you a sizeable (and potentially growing) income stream, making your initial yield on cost even more massive than the big payouts these funds currently offer. With MAIN, people who bought at the IPO were getting a 9% yield, but thanks to the increase in dividends that has swelled to 13%.

Capital gains aren’t really where it’s at with BDCs, though. Buying and holding quality BDCs will secure you a sizeable (and potentially growing) income stream, making your initial yield on cost even more massive than the big payouts these funds currently offer. With MAIN, people who bought at the IPO were getting a 9% yield, but thanks to the increase in dividends that has swelled to 13%.

A BDC With a Recent Cut

Sometimes, though, you actually want to buy a BDC that has recently cut its dividend – because a recent cut means there isn’t likely to be another one for a while!

At the same time, you want a company with strong management, a high yield, and strong dividend coverage. Triangle Capital Corporation (TCAP) fits this profile – the firm increased payouts by more than 73% since the summer of 2007, including its recent 17% cut in May.

The cut might concern some investors, but not to worry – TCAP is earning more in investment income than they are paying out by a healthy margin.

Putting Them Together for 10.5%

It might sound crazy buying stocks that have cut their dividends, but there’s a reason to make a contrarian BDC portfolio diversified across MAIN, TCAP and PSEC.

First, with PSEC you’re buying at a steep discount to NAV that effectively prices in much, if not all, of future NAV declines. Also with improvements in the high yield sector broadly, PSEC’s NAV declines are likely to moderate in the future, and the company might even find ways to reverse the trend.

PSEC isn’t the best BDC out there, though. TCAP is much higher quality, and its hefty 11.6% payout at current prices is an attractive compensation for the stock’s recent dividend cut. And of course MAIN, with its strong history of dividend increases, is a great income producer—although you are paying a price. At current levels, the stock is priced at a 52% premium to NAV, meaning buyers are likely to get a better deal if they wait to buy.

Picking up these three stocks today nets you a 10.5% average portfolio yield, and the income starts immediately. That is reason enough to buy some now, sit back, and wait for corrections to buy more.

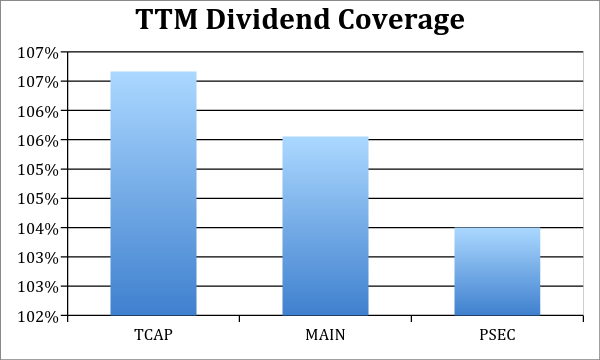

Why now? These stocks all are substantially covering their dividends, meaning payouts are secure for the foreseeable future:

For the last 4 quarters, each stock is earning over 100% of its dividend in NII. Coming in at the top is TCAP, whose strong dividend coverage and recent cut make it a good buy right now. MAIN’s strong coverage also makes it appealing, although the price is steep.

For the last 4 quarters, each stock is earning over 100% of its dividend in NII. Coming in at the top is TCAP, whose strong dividend coverage and recent cut make it a good buy right now. MAIN’s strong coverage also makes it appealing, although the price is steep.

PSEC’s coverage is a bit lower, but still well above 100%, meaning the dividend remains safe. Additionally, the stock is priced very cheaply, so any increase to NII or improvement in the future is likely to boost the stock, offering great capital gains potential.

-Brett Owens

Sponsored Link: When you’ve got your BDCs, you’re off to a great start in building a portfolio with a high yield. But we can go even further. I recommend adding three bond funds that yield over 8% can give us even more strong payouts while diversifying across companies and sectors. These funds are favorites of billionaire “Bond God” Jeffrey Gundlach – and if you’d like to know more information, click here to read my full analysis.

Source: Contrarian Outlook