Starbucks Corp. (SBUX) is staging a comeback as comparable store sales have turned around this year. This Zacks Rank #1 (Strong Buy) is expected to grow earnings by the double digits in 2026.

Starbucks operates more than 41,000 company-operated and licensed coffeehouses. It also has a growing presence in consumer-packaged goods.

Starbucks Beats in the Fiscal Second Quarter 2026

On Apr 28, 2026, Starbucks reported its fiscal second quarter 2026 earnings and beat on the Zacks Consensus by $0.06. Earnings were $0.50 versus the consensus of $0.44.

It was the first earnings beat in the last five quarters as the company has been struggling.

Comparable store sales, a key metric for restaurants, were better than expected.

Global comparable store sales rose 6.2%, driven by a 3.8% increase in comparable transactions and a 2.4% increase in average ticket.

U.S comparable store sales, its largest market, rose 7.1%, primarily driven by a 4.3% increase in comparable transactions and a 2.7% increase in average ticket.

International comparable store sales rose 2.6%, but China, one of its largest international markets, was up just 0.5%. However, China has been struggling so to see a positive comparable number was a surprise.

“We’ve been clear that topline improvement would come first, with earnings growth to follow. We have more work to do, but we’re pleased to see the combination of our comp growth and cost discipline starting to show up in margins,” said Cathy Smith, CFO.

Starbucks Raised Full Year Earnings and Comparable Sales Guidance

Starbucks is starting to see some fruit from its labor in the turnaround.

It raised its fiscal 2026 comparable sales guidance to 5% or higher from 3% or higher which it gave back in Jan 2026.

Starbucks also raised its earnings guidance to a range of $2.25 to $2.45 from the prior guidance of $2.15 to $2.40.

The analysts are bullish too. Nine estimates were raised for fiscal 2026 in the last month with eight being revised higher for fiscal 2027 during that time as well.

The fiscal 2026 Zacks Consensus estimate rose to $2.40 from $2.30 in the last 30 days. That’s an earnings gain of 12.7% year-over-year because Starbucks made just $2.13 last year.

For fiscal 2027, the Zacks Consensus has jumped to $3.05 from $2.93 in the last month. This is further earnings growth of 27.3%.

Here’s what it looks like on the price and consensus chart. You can see that 2026 and 2027 are starting to turn higher.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

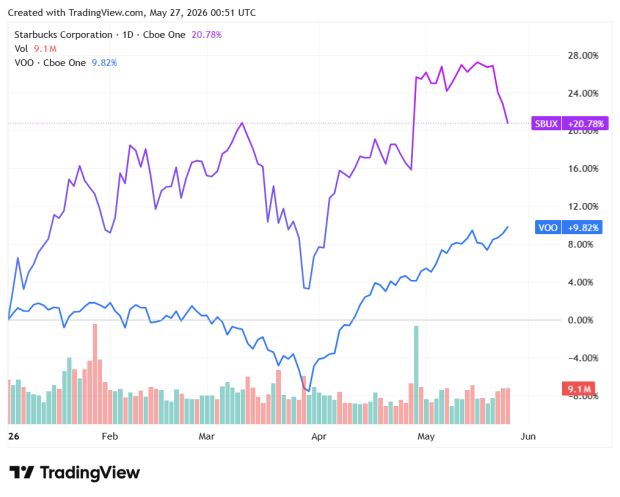

Shares of Starbucks Are Outperforming in 2026

It’s been tough being a Starbucks shareholder over the last 5 years. Shares are down 10.9% compared to the S&P 500, which has gained 78.7%.

But this year, shares are up year-to-date and are outperforming the S&P 500.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

It’s still a turnaround story, and not a fundamental one. Starbucks is trading with a forward price-to-earnings (P/E) ratio of 43. A P/E ratio over 30 usually means a company is extremely expensive.

Starbucks pays a dividend of $2.48, which is higher than the expected earnings this year. That’s a yield of 2.4%. But the dividend rewards shareholders for their patience.

Starbucks has not been a Zacks Rank #1 Strong Buy stock since 2019.

If you are looking for a turnaround play in the restaurant stocks, Starbucks should be on your short list.

— Tracey Ryniec

Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report.

Source: Zacks