Will the new peace in the Middle East hold? What will happen when the “reciprocal tariff” deadline arrives on July 9?

Truth is, no one knows. But we contrarians DO know this: Shaky times like these are tailor-made for us.

Yes, the S&P 500 has been shrugging off all of this (stocks do climb a wall of worry, after all). That’s true. But it’s also caused a lot of mainstream investors to miss the many strong dividend deals that are still on the board.

Near the top of my list for these “dumpster-dive” payers is the Hershey Co. (HSY). (To be clear, “dumpster dive” isn’t a comment on the chocolate!) The stock, which we hold in my Hidden Yields advisory, needs no introduction: Everyone knows these brands (pictured below with their annual sales):

Let’s look at a few reasons why HSY is a, er, sweet buy now.

Let’s look at a few reasons why HSY is a, er, sweet buy now.

Tariffs? War? Hershey Navigates Around Both

The company’s answer to overseas worries can be summed up in six words: Make it where you sell it.

The choco-giant churns out its confectioneries at 14 US plants, including in Hershey, Pennsylvania (of course!), as well as Virginia, Tennessee and Illinois. It also makes other snacks (more on those in a second), like Dot’s Homestyle Pretzels and Pirate’s Booty puffs, at facilities in Indiana and Kansas.

Internationally, Hershey has plants in Brazil, India, Canada and Mexico. That local focus gives it some insulation if those countries slap retaliatory tariffs on US imports. Moreover, international sales are only about 10% of yearly revenue, going by 2024 numbers, so we’re really talking about a domestic company here.

Nonetheless, Hershey does face one big cost its C-suite can’t fully control. Let’s talk about that now.

Dethroning “King Cocoa”

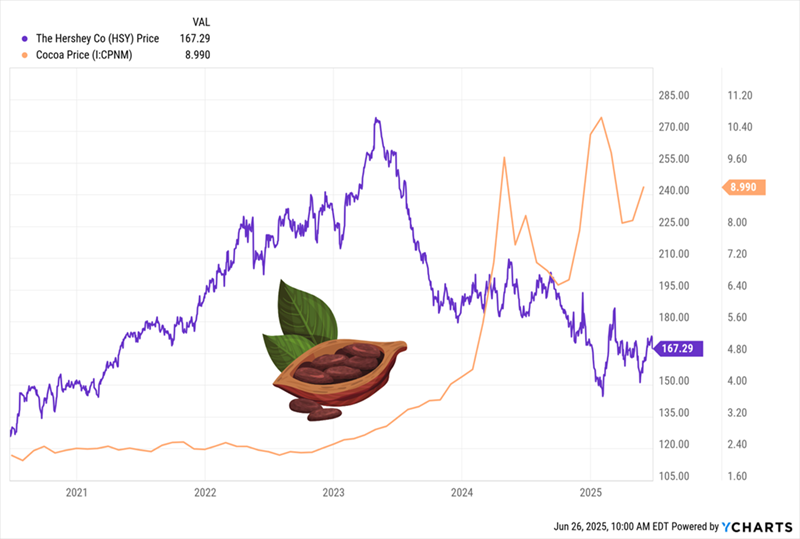

Hershey runs on cocoa like a Ford (F) F-150 runs on gasoline. In all, the bean accounts for about 20% of Hershey’s cost of goods sold. That’s big enough that you can actually see fickle cocoa prices wrenching Hershey’s stock up and down:

Cocoa Takes HSY for a Ride

Soaring cocoa is one reason why HSY is trailing the market this year, down about 1.4% as I write this, compared to about a 4.4% gain for the S&P 500.

Soaring cocoa is one reason why HSY is trailing the market this year, down about 1.4% as I write this, compared to about a 4.4% gain for the S&P 500.

But our “Hershey bears” are thinking too short term: First, despite cocoa’s longer-term rise, it’s well off its peak—down double-digits so far this year. Second, while cocoa prices are forecast to stay strong in 2025, the World Bank forecasts a 13% drop in 2026.

What could cause that? I don’t know about you, but when I hit the grocery store, I’m cutting back. And with chocolate on the rise, more people (like my family of four) are likely to opt for cheaper snacks. The cure for high prices is, after all, high prices!

Candymakers are ahead of this shift. Hershey, for example, launched its crunchy waffle cone bar last summer, with, as the name says, waffle-cone bits that displace some chocolate.

That’s a small example; the company’s real secret weapon is Reese, its biggest sales generator, which is synonymous with peanut butter.

That gives it lots of leeway to roll out new non-chocolate products, like its new Reese peanut-butter-filled pretzels, launched in April. Other, similar things are happening in the background, too, like Hershey’s 2023 purchase of two plants from Weaver Popcorn Manufacturing, as well as its 2022 buy of Pretzels, Inc. These moves let Hershey sidestep shifting cocoa and meet shoppers where they are.

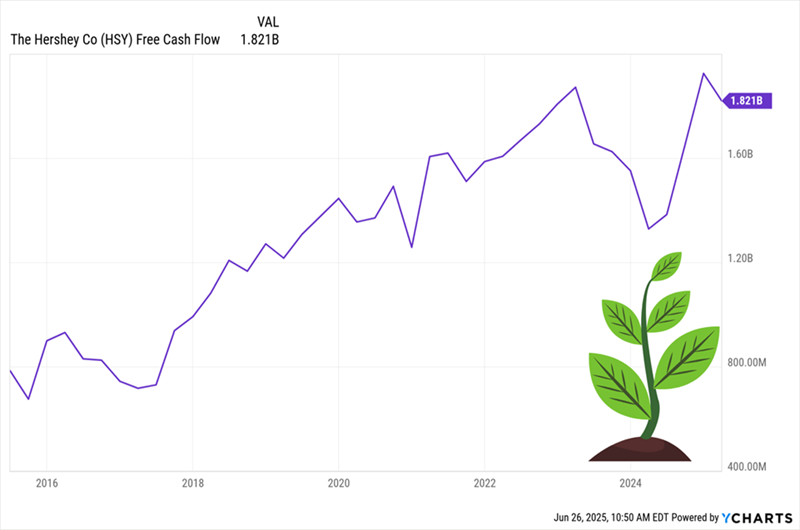

Meantime, management has embarked on a two-year restructuring plan, with the goal of saving $300 million through automation and streamlined production. That’s helped push up Hershey’s free cash flow (FCF), despite pricey cocoa:

Free Cash Flow Shakes Off Rising Cocoa, Bolts Higher

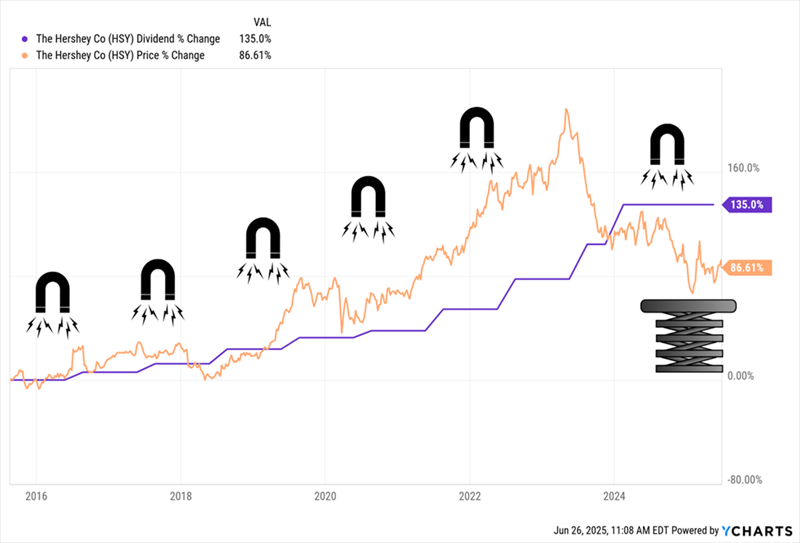

That rise in FCF helped power a 32% boost to HSY’s dividend in 2024. This is where the “Dividend Magnet” comes in, telling us this one really is an overlooked bargain. As you can see below, the stock price has tracked the payout higher in the long run—even running ahead of it in the pandemic, as lockdowns boosted snack sales.

That rise in FCF helped power a 32% boost to HSY’s dividend in 2024. This is where the “Dividend Magnet” comes in, telling us this one really is an overlooked bargain. As you can see below, the stock price has tracked the payout higher in the long run—even running ahead of it in the pandemic, as lockdowns boosted snack sales.

Until early last year, that is.

Hershey’s Stock Falls Behind Its Payout—Setting It Up to Bounce

To be sure, the stock’s 3.3% yield doesn’t really get our blood sugar up, but it is more than double the S&P 500 average. What we’re really focused on here is payout growth—and, more important, the fact that the stock has fallen off the dividend’s pace. That sets us up for “snap back” upside in the coming months.

To be sure, the stock’s 3.3% yield doesn’t really get our blood sugar up, but it is more than double the S&P 500 average. What we’re really focused on here is payout growth—and, more important, the fact that the stock has fallen off the dividend’s pace. That sets us up for “snap back” upside in the coming months.

Moreover, as Hershey cuts costs and cocoa prices retreat, the company could surprise with another big payout hike—and we want to be in when that happens.

One last thing: This stock is a standout for its low-volatility, with a five-year beta rating of 0.28, meaning it’s less than a third as volatile as the S&P 500. That’s the kind of tranquility we love in a market like this.

— Brett Owens

Start With Hershey—Then BUY These 5 Dividends for 15%+ Yearly Gains (Bull or Bear) [sponsor]

No matter what happens on July 9 (or anytime, really), here’s what Hershey is likely to do:

Shrug it off and keep growing its dividend.

The stock is battle-tested, with the company founded back in 1894—another time when tariffs were running high.

That’s why Hershey is one of my top buys now. But it’s far from the only one.

I’ve zeroed in on 4 other winners I’ve “stress tested” eight ways from Sunday. And I’ve got each of them pegged for 15%+ annualized returns, driven by their dividends—payouts that rise year after year, with growth that’s actually accelerating.

Click here and I’ll walk you through all 5 of these “recession-resistant” picks. You’ll also get a free Special Report with their names and tickers. Plus I’ll give you a risk-free invitation to try my premium dividend-growth service, Hidden Yields.

It’s a wealth-building package tailor-made for right now. Don’t miss it.

Source: Contrarian Outlook