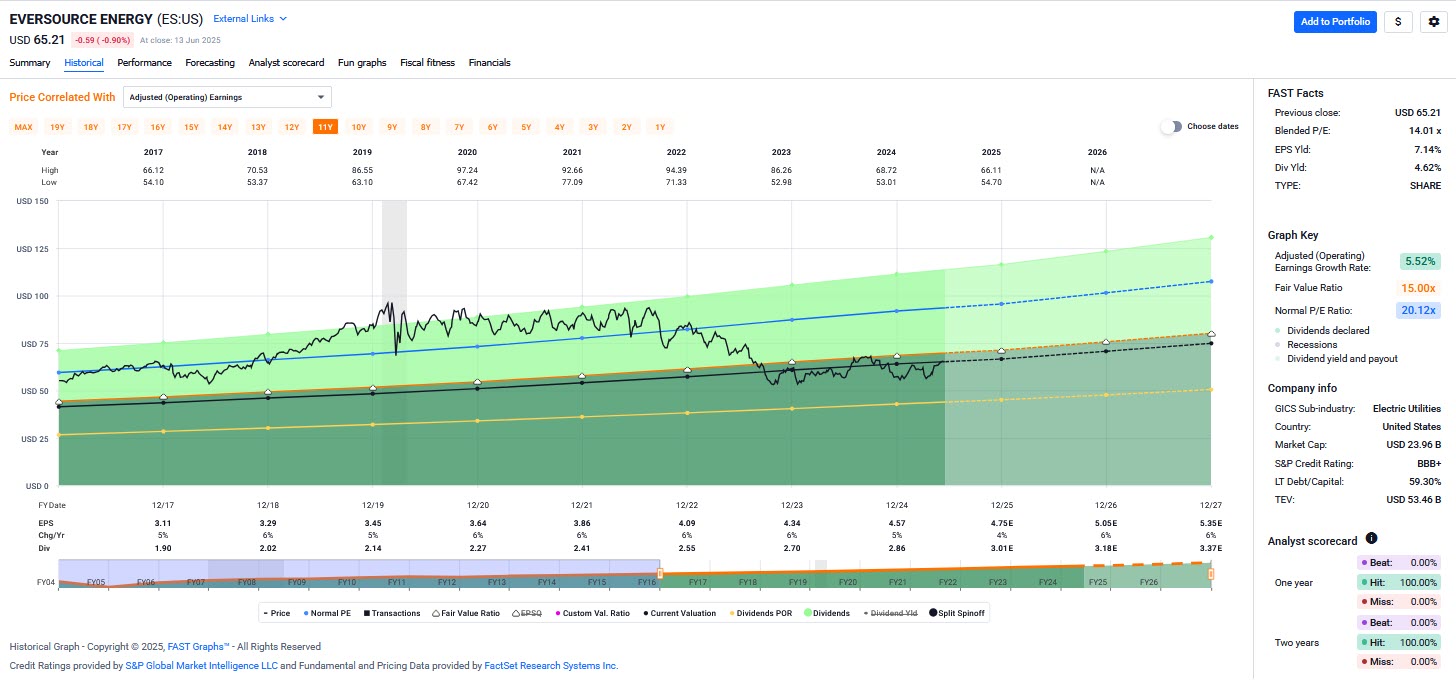

Income and Total Return

In this video, Chuck Carnevale, co-founder of FAST Graphs, aka Mr. Valuation analyzes Eversource Energy (ES), for Income and Total Return, a New England-based utility known for its consistent earnings and dividend growth. With a dividend increasing at nearly 8% annually and a current yield of 4.6%, the stock offers strong income potential. Historically valued at premium P/E ratios (~18), Eversource now trades at a lower P/E (~14), presenting a rare value opportunity.

Despite some temporary earnings pressure from investments in renewable energy and high capital expenditures, core fundamentals remain strong. The company has delivered steady 5–6% earnings growth since 2006, with forecasts expecting more of the same. Its analyst scorecard shows 100% accuracy on 1- and 2-year estimates, reinforcing its predictability.

Despite some temporary earnings pressure from investments in renewable energy and high capital expenditures, core fundamentals remain strong. The company has delivered steady 5–6% earnings growth since 2006, with forecasts expecting more of the same. Its analyst scorecard shows 100% accuracy on 1- and 2-year estimates, reinforcing its predictability.

While return on equity temporarily turned negative in 2023 due to one-time charges, cash flow remains healthy and covers dividends comfortably. If the stock returns to fair value or regains its premium valuation, investors could see total returns of 12–25% annually over the next few years. Chuck positions Eversource as a high-quality, income-focused investment with upside potential, especially appealing for long-term, conservative investors.

— Chuck Carnevale

The Original Magnificent Seven Produced 16,894% Average Returns Over 20 Years. But the Man Who Called Nvidia at $1.10 Says "AI's Next Magnificent Seven Could Do It Even Faster." See His Breakdown of the Seven Stocks You Should Own Here.

Source: FAST Graphs

Disclosure: Long ES