Let me start with a prediction: the S&P 500 will gain about 5% this year—not great, but not bad, either.

This isn’t really a Nostradamus-level call: I’m simply annualizing the gain the market has posted so far in 2025, as of this writing.

We can think of this year as the middle stage of the business cycle—where inflation is cooling, the labor market is softening, and consumer spending is starting to slow (emphasis on starting to).

In other words, it’s the perfect setup for us to make sure we’re well diversified by looking at assets beyond stocks. At the top of our list? Corporate bonds.

This Unloved 14% Bond Dividend Is the Perfect “Mid-Cycle” Buy

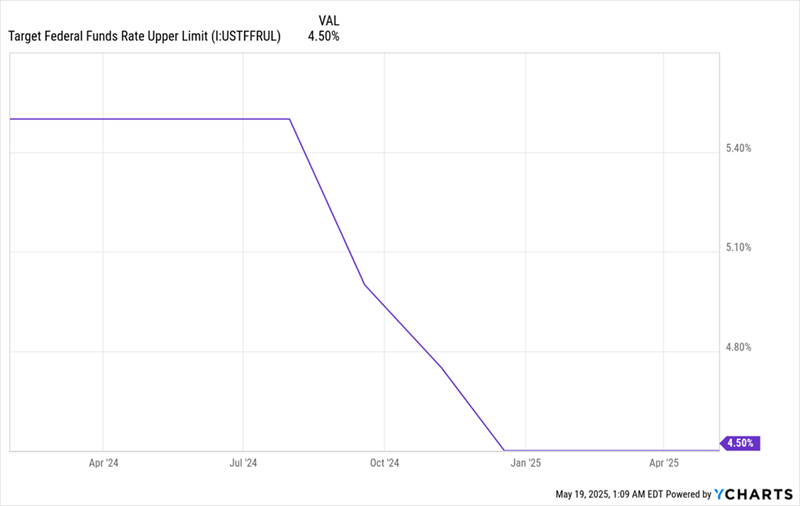

Why are we looking at corporate bonds now? Two words: the Fed. The central bank has been expected to cut rates aggressively for a long time now, and while it did cut twice in 2024, the story was how those cuts were fewer than expected.

Two Cuts So Far

That story has repeated itself this year, with the Fed continuing to hold back on rate cuts, even though investors have consistently expected more.

That story has repeated itself this year, with the Fed continuing to hold back on rate cuts, even though investors have consistently expected more.

To take advantage of the Fed’s slow-walk on cuts, we’re targeting closed-end funds (CEFs) that focus on corporate bonds. That’s because the bonds these funds own were issued when yields were high, and a shift toward later rate cuts gives them more time to buy said bonds—and most important, keep maintaining high payouts to us.

And the truth is, rates will move lower, either due to a shakeup of investor confidence resulting from the recent US government-debt downgrade or, more likely, the natural progression of the business cycle, under which the economy would continue to slow.

Then, when rates do come down and investors go looking for higher income, the value of these funds’ bonds—and indeed the value of these funds themselves—should rise.

So to sum up, we’ve got a chance to buy in now, while yields are high, and front-run the income-seeking crowd set to pile in later.

One fund is quietly positioning itself to capitalize on this setup right now—and paying a rare 14% income stream while flying under most investors’ radar: the Nuveen Core Plus Impact Fund (NPCT), a holding of my CEF Insider service.

Consider what this low-profile bond CEF offers us:

- That incredible 14% payout, which actually rose in June 2024. The dividend also comes our way monthly.

- An 8.4% discount to net asset value (NAV, or the value of its underlying portfolio). This essentially means we’re getting the chance to buy its bond portfolio for less than 92 cents on the dollar. For a hint of the upside on offer here, consider that this markdown is far below the 3.9% discount the typical bond CEF sports.

- The fund has returned a strong 11% in the past year, despite its bigger-than-average discount. That’s the ultimate indicator that this fund is (for now!) overlooked.

The thing to keep in mind most about the fund’s recent and future returns is that, due to its outsized yield, a huge slice of its gains come our way as dividends. So we’re talking about liquid profits here: real, spendable income we can use however we like.

The cause of that discount is worth considering, too. Note the name: This fund focuses on corporate bonds issued by companies that comply with environmental, social and governance (ESG) benchmarks. I think you’ll agree that ESG has fallen out of favor with investors on both Wall Street and Main Street.

That sounds like a negative, but it’s actually an opportunity for us, since it’s a big part of the reason for that 8.4% discount—many investors simply hear “ESG” and pass this fund by without taking a look under the hood.

Source: Nuveen

Source: Nuveen

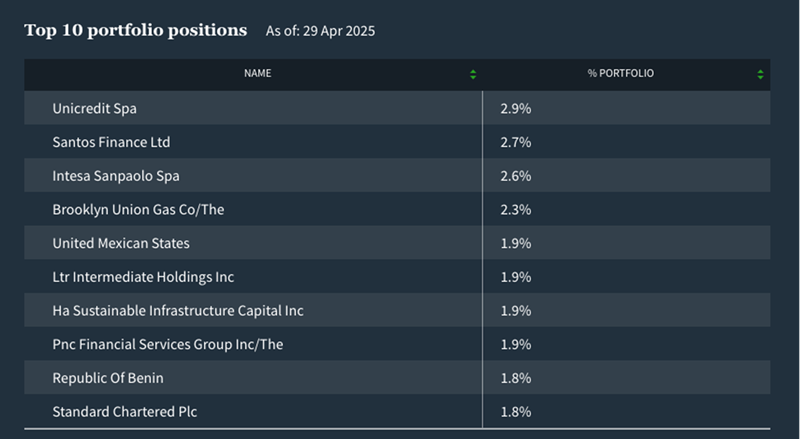

That’s causing them to walk right past a smartly run fund with a well-built portfolio. Bonds issued by regional-bank powerhouses with decades of stability, like PNC, and large international banks, like Standard Chartered, have been delivering reliable income that NPCT’s managers have handed over to investors.

Meanwhile, NPCT, and its shareholders, have quietly collected that huge income stream throughout this “mid-cycle” period. Eventually, the fund will either change its ESG mandate or investors will simply ignore that mandate and take note of the fund’s top-quality bond portfolio. That’s especially likely if we see rate cuts accelerate.

NPCT’s discount, then, is entirely due to investors misunderstanding how reliable and enduring the fund’s dividend is. And misunderstandings like that are perfect for us contrarians to exploit.

— Michael Foster

Yours Now: An 11.6%-Paying (and Cheap!) Portfolio Stocked With Monthly Payers [sponsor]

As we just discussed, most folks wouldn’t touch NPCT with a 10-foot pole—and that’s exactly why we love it! It throws off a massive 14% yield, pays us monthly, and trades at a big discount—all because of one misunderstood detail.

The best part? It’s one of several high-paying CEFs in our Monthly Dividend Portfolio—which I’ve specifically built to deliver steady income through any market cycle.

Now I want to share the names of ALL the investments in this “battleship” monthly paying portfolio with you. Between them, they kick out a huge 11.6% average dividend and they’re all overlooked bargains now. That won’t last

Source: Contrarian Outlook