Unfortunately, I see a lot of people out there struggling.

YouTube is filled with videos of people living out on the streets or in their cars.

Not a nice way to end up.

As someone who grew up in abject poverty, I empathize with these people.

And I can tell you from firsthand experience, there’s a way to insure against ending up in such a situation later in life.

It’s saving and investing as much as we possibly can, whenever we can.

If you can live below your means and intelligently invest your excess savings for the long term, that nearly guarantees you won’t end up in dire straits later on in life.

This is due to the effects of compounding, where money makes more money all by itself exponentially.

This is due to the effects of compounding, where money makes more money all by itself exponentially.

Perhaps the best way to tap into this power is via dividend growth investing.

This is a long-term investment strategy that involves buying and holding shares in world-class businesses that reward their shareholders with safe, growing dividends.

You can find many examples of such businesses by pulling up the Dividend Champions, Contenders, and Challengers list – a compilation of data on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

The reason why I’m such a fan (and practitioner) of dividend growth investing is because it tends to funnel an investor right into some of the world’s best businesses, and this happens by virtue of how growing profits are necessary to fund growing dividends.

Most businesses which are started up fail rather quickly.

To be able to not only survive but thrive and actually afford to pay out growing dividends requires a special kind of enterprise.

It’s this specialness that attracted me to the strategy, which resulted in my building of the FIRE Fund over the last 15 years.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

To be able to live off of dividends after growing up extremely poor is something that amazes me and never escapes my gratitude.

In fact, I’ve been able to live off of dividends since I quit my job and retired in my early 30s.

That said, even with a special business in your sights, there’s still the matter of valuation at the time of investment.

Whereas price is what you pay, it’s value that you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Living below your means and using your savings to buy undervalued high-quality dividend growth stocks is a fantastic way to build significant wealth and passive dividend income over time, which can prevent undesirable outcomes later in life.

Now, being able to recognize undervaluation first requires one to understand how valuation works.

If that understanding isn’t already in place, make sure to read Lesson 11: Valuation.

Written by fellow contributor Dave Van Knapp, it deftly explains valuation using simple terminology and even provides an easy-to-use valuation system you can utilize on your own.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Lockheed Martin Corp. (LMT)

Lockheed Martin Corp. (LMT)

Lockheed Martin Corp. (LMT) is an American defense and aerospace company.

Founded in 1912, Lockheed Martin is now a $104 billion (by market cap) defense giant that employs approximately 120,000 people.

This is the largest (by revenue) defense contractor in the world.

The company reports results across four segments: Aeronautics, 40% of FY 2024 revenue; Rotary and Mission Systems, 24%; Space, 18%; and Missiles & Fire Control, 18%.

Lockheed Martin derives nearly 75% of its revenue from the US government (primarily through the the US Department of Defense), and the rest of revenue is mainly sourced from foreign governments (commercial revenue is minimal).

The company is responsible for manufacturing a host of critical and large military aircraft platforms, including the F-35 Lightning II, the F-22 Raptor, the F-16 Fighting Falcon, and the SH-60 Seahawk.

The F-35, a fifth-generation combat aircraft, is the largest and most expensive military weapons system in the world.

In addition, the company’s various missile programs are vital for both offensive and defensive capabilities.

And this brings me to the crux of the matter.

Why are offensive and defensive capabilities so important?

Well, the reasoning is the same as it was at the dawn of civilization: Conflict is part of the human condition.

Societies are often belligerent, and the only effective deterrent for a sovereign nation is military capabilities that offer offensive and defensive options in order to maintain peace and prosperity (and avoid being taken over by a hostile outside force).

This was true when small collections of humans were fighting each other with projectile rocks; it’s still true today now that we’re fighting with advanced missiles.

I wish we operated differently as a species, but we must live and invest in the reality we have.

This reality nearly guarantees Lockheed Martin ongoing business.

Moreover, because of the way in which military systems are constantly advancing and becoming more expensive over time (we’re certainly no longer throwing rocks at each other), revenue naturally escalates over time.

It’s inherent progression layered onto built-in demand.

As the world’s largest defense contractor headquartered in the world’s largest spender on defense products and service, Lockheed Martin almost can’t help but to rake in growing revenue and profit, leading to a growing dividend.

Dividend Growth, Growth Rate, Payout Ratio and Yield

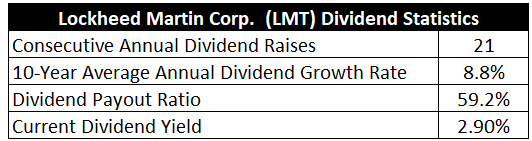

To this point, the company has increased its dividend for 21 consecutive years, coming up on Dividend Aristocrat candidacy.

Its 10-year dividend growth rate of 8.8% is very solid and easily beats inflation (under ordinary circumstances), although more recent dividend raises have been in a mid-single-digit range.

Lockheed Martin has been facing execution issues around certain programs (primarily the F-35), which has caused bumpy results over the last couple of years and bled down into bumpy dividend growth.

Still, Lockheed Martin is a world-class, industry-leading business which continues to grow its dividend at a respectable clip right through the challenges.

I think that speaks volumes.

I think that speaks volumes.

Meantime, the stock offers a 2.9% yield.

That’s 30 basis points higher than its own five-year average, so what may only be a temporary dip in dividend growth has been offset by a higher starting yield which can be permanently locked in.

Not a bad trade-off.

And with a payout ratio of 59.2%, which is pretty appropriate for a large and mature business well into its life cycle, the dividend is healthy and easily supported by earnings.

Lockheed Martin’s dividend metrics check the right boxes, in my view.

You get a nice (and higher-than-usual) yield, solid dividend growth, an unsurprising payout ratio, and a clear commitment to the dividend and the continued growth of it.

It’s a nice balance for almost any long-term dividend growth investor to get behind.

Revenue and Earnings Growth

As balanced as these metrics may be, though, many of them are based on what’s happened in the past.

However, investors must always be investing with the future in mind, as today’s capital gets risked for tomorrow’s rewards.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will be extremely useful when the time comes to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this manner should give us the material we need to confidently gauge where the business could be going from here.

Lockheed Martin advanced its revenue from $40.5 billion in FY 2015 to $71 billion in FY 2024.

That’s a compound annual growth rate of 6.4%.

For what is a large, mature business, this is impressive top-line growth.

I’d expect (or like) to see something in a mid-single-digit area, and Lockheed Martin more than delivered.

Earnings per share grew from $11.46 to $22.31 over this period, which is a CAGR of 7.7%.

This is good.

It’s not outstanding, but it’s far from bad.

Excess bottom-line growth was driven by substantial buybacks which reduced the outstanding share count by nearly 25% over the last decade.

Now, Lockheed Martin has seen its results harmed in recent years by execution issues (mainly around the F-35); absent this, I believe we’d be looking at even better EPS growth (likely around 10% or so).

Looking forward, CFRA forecasts a 5% compound annual growth rate for Lockheed Martin’s EPS over the next three years.

CFRA’s cautious approach, which doesn’t seem unwarranted to me, seems to orbit around near-term execution issues.

Lockheed Martin’s F-35 has faced cost inflation/overruns, readiness concerns, and reliability questions.

This has been a big overhang, clouding what’s otherwise a nice, sunny picture.

However, there are plenty of silver linings.

CFRA highlights some of them: “We see a healthy long-term outlook for U.S. and allied defense spending, an attractive dividend, and a track record for share count reductions via buybacks.”

Speaking more on that backlog, it finished last year at a record $176 billion (representing more than two years of revenue and eclipsing the company’s entire market cap).

I think that short passage from CFRA, when juxtaposed against the 5% forecast, does a good job of contrasting the investment time frames.

If one is in it for the next year or two, Lockheed Martin may have a tough slog.

However, if one is truly a long-term investor, it’s difficult to imagine a scenario where the company doesn’t do well, grow at a rate roughly in line with its historical norm, and continue to fund and grow its dividend.

And when it comes to that dividend growth, I anticipate it to closely mirror EPS growth on a go-forward basis (based on the payout ratio being fairly full).

If one can get 7%+ EPS and dividend growth on top of a ~3% starting yield, that sets up a long-term dividend growth investor for a ~10% annualized rate of return (assuming a static valuation).

Plus, there’s some possible additional upside from multiple expansion.

That can get one to double-digit annual returns on a blue-chip, industry-leading business poised to hit Dividend Aristocrat status in a few years.

Awfully tough to complain about that.

Financial Position

Moving over to the balance sheet, the company has a good financial position.

The long-term debt/equity ratio is 3.1, while the interest coverage ratio is 7.

That former number is looks high, but that’s because common equity is low.

To put things in perspective, Lockheed Martin’s total long-term debt load of $19.6 billion is not overwhelming at all for a company of its size (again, the market cap is over $100 billion).

There has been some balance sheet deterioration over the last decade, and I’d like to see the financial position improve, but I see nothing immediately concerning at all here.

Profitability is strong.

Return on equity has averaged 89.5% over the last five years, while net margin has averaged 9.2%.

ROE is juiced by the structure of the balance sheet, but even ROIC is often over 30%, so there are high returns on capital being generated here.

As the world’s largest defense contractor headquartered in the world’s largest spender on defense products and services, it’s tough to imagine any reality in which Lockheed Martin doesn’t do well over time.

And with economies of scale, high barriers to entry, long-term contracts, unique government relationships, R&D, IP, and technological know-how, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

Only a few prime defense contractors exist in the US, creating an industry oligopoly which limits competition, but there are a handful of private defense contractors that are coming up and shaping into serious competitors.

The direct and somewhat symbiotic government relationships can lead to more oversight and regulatory risk than the average business, and the current administration’s aims to reduce government spending is an additional near-term headwind for Lockheed Martin.

The very nature of the business model means there’s a high degree of geopolitical risk here.

Execution risks have been clear of late, with cost overruns on the F-35 program being a prime example, and Lockheed Martin must execute properly in order to maintain credibility and leadership.

The company is somewhat linked to the overall health of the US economy, as a stronger economy creates more leeway for defense spending, although defense spending has historically been resilient and resistant to reductions – particularly when it comes to the mission-critical programs that Lockheed Martin specializes in.

Being an international company, there’s some exposure to currency exchange rates.

I certainly see some risks around the business, but most of them are fairly standard for a defense contractor.

And with the valuation being as undemanding as it is, a lot of risk is already being priced in…

Valuation

The stock is trading hands for a P/E ratio of 20.4.

That’s a below-market multiple on an industry-leading business manufacturing mission-critical defense products and services the US government would be hard-pressed to do without.

And this multiple is on depressed earnings, as recent results have not been strong.

If results were normalized, the P/E ratio would be closer to 15.

If we assume Lockheed Martin is capable of growing its EPS at 10% or so per year, that puts us at a PEG ratio below 2.

These are not heroic assumptions or multiples.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

This dividend growth rate is one I’ve almost always used when valuing Lockheed Martin.

It just strikes me as very appropriate for a business that’s grown its EPS at a high-single-digit rate during a tougher-than-usual period.

The demonstrated dividend growth over the last decade eclipses my mark.

And with the payout ratio being where it’s at, I’d expect the dividend to grow in a way that pretty closely tracks EPS growth on a go-forward basis.

Again, circling back around to what I touched on earlier, Lockheed Martin seems more than capable of growing its EPS at a 7%+ annual rate.

There would have to be something really wrong with the business to fall far short of this level over the coming years.

The DDM analysis gives me a fair value of $470.80.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

In my eyes, the stock appears to be modestly undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates LMT as a 4-star stock, with a fair value estimate of $530.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates LMT as a 3-star “HOLD”, with a 12-month target price of $488.00.

Although I came out the lowest, we have a fairly tight range here. Averaging the three numbers out gives us a final valuation of $496.27, which would indicate the stock is possibly 8% undervalued.

Bottom line: Lockheed Martin Corp. (LMT) is the world’s largest defense contractor headquartered in the world’s largest spender of defense products and services. A natural necessity for what it sells, based on human nature and a desire for countries to retain safety and sovereignty, means the company almost can’t lose over the long run. With a market-beating yield, a reasonable payout ratio, high-single-digit dividend growth, more than 20 consecutive years of dividend increases, and the potential that shares are 8% undervalued, long-term dividend growth investors looking for safety and security in an uncertain world should have their eyes on this name.

Bottom line: Lockheed Martin Corp. (LMT) is the world’s largest defense contractor headquartered in the world’s largest spender of defense products and services. A natural necessity for what it sells, based on human nature and a desire for countries to retain safety and sovereignty, means the company almost can’t lose over the long run. With a market-beating yield, a reasonable payout ratio, high-single-digit dividend growth, more than 20 consecutive years of dividend increases, and the potential that shares are 8% undervalued, long-term dividend growth investors looking for safety and security in an uncertain world should have their eyes on this name.

-Jason Fieber

Note from D&I: How safe is LMT’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 80. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, LMT’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Source: Dividends & Income

Disclosure: I’m long LMT.