Investing is so simple.

Yet, it’s so difficult.

Why is this?

Well, a lot of the basic principles that underpin what successful investing is all about are quite simple in nature.

All the same, though, these principles can be excruciatingly difficult to actually apply in a consistent manner in real life.

I’ll give you an example.

Focusing on the fundamentals of what you’re investing in is a simple idea that is effective and timeless.

But when you’ve got craziness in the market and speculative assets with no fundamentals at all are making your neighbors rich, it’s suddenly not so easy to stick to that wise guidance.

This is why I take great solace in the dividend growth investing strategy.

This strategy, which advocates buying and holding shares in great businesses that pay safe, growing dividends to shareholders, forces me to always focus on the fundamentals.

The fundamentals are front and center when one is employing the strategy, as one is trying to find those terrific businesses that can sustain rising dividends for decades on end.

A business can’t pay growing dividends for years on end – and continue to do so indefinitely – without doing a lot of things right, and doing those right things shows up in the fundamentals.

To get a glimpse of what I mean, check out the Dividend Champions, Contenders, and Challengers list.

This list has compiled invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

You’ll notice a lot of household names on the list.

You’ll notice a lot of household names on the list.

And for good reason.

It tends to require a certain amount of greatness for a company to even qualify for this strategy, which gives me great comfort.

Offering even more comfort and solace is that steadily rising dividend income.

It’s easy to avoid FOMO when you’ve got growing cash flow coming in, and the five-figure passive dividend income I collect is now actually enough to pay for my bills.

Actually, it’s been enough for me since I quit my job and retired in my early 30s.

My Early Retirement Blueprint recounts how I was able to do that.

A large part of my success has come down to living below my means and intelligently investing my savings into those great businesses – again, simple ideas here.

And that repeated behavior has culminated in the FIRE Fund, which is my real-money dividend growth stock portfolio.

Another simple, timeless idea?

Another simple, timeless idea?

Valuation always matters.

Price is what you pay, but value is what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Sticking to simplicity by buying high-quality dividend growth stocks when they’re undervalued is an effective way to build serious wealth and passive income over one’s lifetime – if they can avoid the pitfalls that life throws at them along the way.

Now, the whole concept of valuation also has some duality in it – simple at its core, but it can be difficult.

Well, this is where Lesson 11: Valuation comes in handy.

Put together by fellow contributor Dave Van Knapp as part of an overarching series of “lessons” designed to teach dividend growth investing, it spells out valuation using plain terminology and even provides an easy-to-use template.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Merck & Co., Inc. (MRK)

Merck & Co., Inc. (MRK)

Merck & Co., Inc. (MRK) is a leading global pharmaceutical company that produces a range of medicines, vaccines, and animal healthcare products.

Founded in 1891, Merck is now a $258 billion (by market cap) healthcare behemoth that employs more than 70,000 people.

The company operates across two reportable segments: Pharmaceutical, 89% of FY 2023 sales; and Animal Health, 9%. Insignificant sales occur as Other Revenue.

Their core areas of focus are: diabetes, infectious diseases, oncology, vaccines, and animal health.

The US is the company’s largest market, accounting for approximately 47% of worldwide sales.

Some of the company’s key drugs include Keytruda, Januvia, Gardasil, and ProQuad.

Keytruda, their triumphant cancer drug, is the company’s most important product and by far the top-selling drug across the portfolio.

This single drug comprised roughly 42% of the company’s worldwide sales for FY 2023.

That’s up from nearly 30% of company revenues for FY 2020, despite Merck’s overall revenue being up significantly since then.

Keytruda has become a larger piece of a growing pie and now dominates the firm’s sales.

With over $25 billion in sales for FY 2023, Keytruda is the best-selling drug in the world.

However, this is a double-edged sword.

Merck has been able to ride Keytruda to incredible heights, but the ride won’t last forever.

Once Keytruda starts rolling over its patent protection, competition will come on strong and eat away at the drug’s sales (and, thus, Merck’s sales).

Notably, this drug is on patent through 2028 in the US and EU, so Merck does have time to prepare for what will almost certainly be slowing/reversing growth as we enter the 2030s.

Merck continues to extend Keytruda’s runway by pursuing new clinical trials and treatment pathways for different types of cancers.

The company is also busy developing new compounds, with 60+ programs in Phase 2 and 30+ programs in Phase 3.

Merck has plenty of opportunities for growth ahead, even with a Keytruda that starts to become a victim of its own success.

Being at the front line of cutting-edge medication places the company in a very exciting area of the global economy, as global demographics (the world continues to grow larger, older, and wealthier) portends rising demand for high-quality healthcare.

Merck has all the tools it needs to do well over the coming years, all while Keytruda is still in its prime, setting up shareholders to benefit from growing revenue, profit, and dividends.

Dividend Growth, Growth Rate, Payout Ratio and Yield

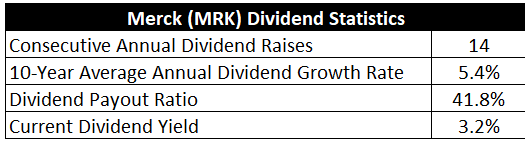

Already, Merck has increased its dividend for 14 consecutive years.

The 10-year dividend growth rate is a decent 5.4%, but the five-year dividend growth rate of 8.7% looks even better.

While Merck is decidedly not some high-growth machine (nor should one expect a mature pharmaceutical company to be one), the stock’s market-beating yield of 3.2% offers plenty of current income and offsets the adequate (but not amazing) dividend growth.

This yield, by the way, is 30 basis points higher than its own five-year average.

This yield, by the way, is 30 basis points higher than its own five-year average.

The stock tends to offer a nice yield, but the yield right now is especially nice.

A payout ratio of 41.8%, based on midpoint guidance for this year’s adjusted EPS, shows us a healthy dividend poised for more growth ahead.

This is a very balanced dividend profile.

Merck doesn’t “wow” me in any one area; instead, there’s a great mix of yield, growth, and safety here.

Revenue and Earnings Growth

As great as this might be, though, many of these metrics are based on what’s happened in the past.

However, investors must always be looking out into the future, as today’s capital gets risked for tomorrow’s rewards.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will come in handy when the time comes later to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this way should give us the information necessary to make an educated judgment call on where the business may be going from here.

Merck moved its revenue from $42.2 billion in FY 2014 to $60.1 billion in FY 2023.

That’s a compound annual growth rate of 4%.

Not bad at all.

I like to see a mid-single-digit (or better) top-line growth rate from a mature business like this.

Merck is getting it done.

Meanwhile, earnings per share grew from $4.07 to $6.35 (adjusted) over this period, which is a CAGR of 5.1%.

I used adjusted EPS for FY 2023, due to the fact that Merck had $6.21 per share in charges for certain transactions that do not accurately reflect the company’s ongoing earnings power.

So what we’re seeing here is mid-single-digit business growth, lining up well with the mid-single-digit dividend growth.

If that’s all there were, I’m not sure that Merck would be a super compelling idea.

But I think there’s more than that.

And that primarily comes down to the fact that the company’s flagship oncology drug Keytruda has only started hitting its stride in the last few years (after initially being approved by the FDA in 2014 and growing its treatment applications thereafter).

If we zoom back to before FY 2019, growth was spotty.

But Merck has started showing signs of sustained growth starting from right about FY 2020, as Keytruda is growing way faster than 5% annually.

And with Keytruda still in its prime, Merck can soak up those sales while also being financially able to build out its pipeline through organic development and acquisitions (in order to prepare for the next stage of the company’s evolution, after Keytruda peaks and starts to decline).

Looking forward, CFRA believes that Merck will compound its EPS at an annual rate of 9% over the next three years.

This jibes with what I was just discussing.

A mid-single-digit growth rate is not bad at all, but Merck appears poised to do quite a bit better than this over the foreseeable future.

CFRA highlights continued strong growth from Keytruda (sales up 17% YOY for the most recent quarter), as well as encouraging movement on the pipeline (such as FDA approval on hypertension drug Winrevair earlier this year).

And I think that’s the one-two punch that gives Merck so much promise over the next few years or so.

I’m willing to assume CFRA’s forecast as a near-term base case for Merck’s growth.

Seeing as how the payout ratio is as low as it is, that would set up the dividend to grow at least as fast – perhaps faster.

Meantime, those buying in now get to kick things off with an atypical 3%+ yield.

If you’re following along, you’re already piecing together a picture that shows faster growth than usual and a yield that’s higher than usual.

Hard to not be excited about that kind of setup.

Financial Position

Moving over to the balance sheet, Merck has a good financial position.

The long-term debt/equity ratio is 0.9, while the interest coverage ratio is nearly 12.

That latter number is artificially and temporarily low, impacted by noted charges.

Merck finished last fiscal year with about $25 billion in net long-term debt, which is not egregious at all for a company of this size.

It’s not a bulletproof balance sheet, but Merck has no issues here whatsoever.

Profitability is great.

Return on equity has averaged 28.3% over the last five years, while net margin has averaged 18.8%.

These are outstanding numbers, despite both being negatively affected by FY 2023’s downturn in GAAP results.

Both ROE and ROIC are routinely over 20% for Merck in normal years, indicating high returns on capital and an ability to generate excess returns well over its WACC.

With its blockbuster drug Keytruda still in its prime and growing apace, Merck is sitting pretty and, arguably, in its best position ever.

And with economies of scale, a global distribution network, patents, IP, and R&D, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

All three of these risks are elevated for this particular industry, in my view, especially regulation.

Patent cliffs are one of the biggest issues for any pharmaceutical company, but Merck has a large pipeline to develop while its most important drug is still under patent protection for a number of years yet.

Speaking further on this point, Keytruda’s status as a linchpin for the business, as well as the fact that patents will not protect it forever, puts a lot of pressure on Merck to work its pipeline and release new blockbuster drugs within the next few years in order to reduce dependency on Keytruda and shepherd in a new era of growth.

Any changes to the complex US healthcare system, which is not popular in its current form, would likely impact Merck directly.

The company’s international footprint exposes it to geopolitics and currency exchange rates.

There is execution risk present, as Merck (like many companies of its ilk) likes to buy growth through bolt-on deals.

While I think these risks are worth carefully thinking over, Merck’s quality and market positioning should also be considered.

And with the stock down nearly 30% from its recent high, the valuation, which looks appealing, should be strongly considered…

Valuation

This stock’s forward P/E ratio, based on midpoint guidance for this year’s adjusted EPS, is just 12.7.

That’s absurdly low for a world-class healthcare business.

If we move past that earnings multiple, because of the adjusted nature it, all basic multiples that I look at are lower than usual.

For example, the P/S ratio of 4 is well below its own five-year average of 4.5.

And the yield, as noted earlier, is higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 7%.

What I’m doing here is, I’m roughly splitting the difference between the 10-year dividend growth rate (~5%) and the near-term forecast for EPS growth (9%).

I think that down-the-middle approach makes sense here.

The prior decade was hampered by quite a bit of time spent without Keytruda fully ramped up.

With that drug now at unexplored heights, Merck has every chance to shine.

All the same, though, I wouldn’t expect dividend growth to be in a double-digit range, even if that 9% mark on EPS growth is reached.

And that’s because the pipeline has to be developed, there’s still a decent chunk of debt to handle, and Keytruda’s patent protection will start to roll off in a few years.

All in all, I don’t see something in the 7% area to be an unreasonable expectation from Merck over the coming years.

The DDM analysis gives me a fair value of $115.56.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

My view is that the stock is priced quite a bit lower than it ought to be.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates MRK as a 4-star stock, with a fair value estimate of $120.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates MRK as a 3-star “HOLD”, with a 12-month target price of $106.00.

I’m right about in the middle this time around. Averaging the three numbers out gives us a final valuation of $113.85, which would indicate the stock is possibly 14% undervalued.

Bottom line: Merck & Co., Inc. (MRK) is a high-quality healthcare business with the world’s best-selling drug under its umbrella. Merck has, in many ways, never looked better. It’s set up for a golden era. With a market-beating yield, a low payout ratio, inflation-beating dividend growth, nearly 15 consecutive years of dividend increases, and the potential that shares are 14% undervalued, dividend growth investors looking for more healthcare exposure have low-hanging fruit to pick from here.

Bottom line: Merck & Co., Inc. (MRK) is a high-quality healthcare business with the world’s best-selling drug under its umbrella. Merck has, in many ways, never looked better. It’s set up for a golden era. With a market-beating yield, a low payout ratio, inflation-beating dividend growth, nearly 15 consecutive years of dividend increases, and the potential that shares are 14% undervalued, dividend growth investors looking for more healthcare exposure have low-hanging fruit to pick from here.

-Jason Fieber

Note from D&I: How safe is MRK’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 90. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, MRK’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Source: Dividends & Income

Disclosure: I’m long MRK.