With more volatility likely as we move past the election and into late 2024, retirement planning might not be top of mind for you right now.

I get it.

But with investing—income investing, especially—it’s critical to keep the long term in focus. And over the long term, the direction of the markets is up.

When we invest in closed-end funds (CEFs), we get an extra advantage: High income, which often comes our way monthly. The average CEF yields 8% now. That’s roughly the long-term average annualized price gain of the S&P 500, depending on the timeframe you look at, delivered to us in dividend cash every year.

And that’s before we even talk about CEFs’ price gains.

That added certainty of getting most of our returns in safe dividend cash is why we love CEFs, especially in times like these. And despite the gains we’ve seen across asset classes this year, there are still CEFs available at a bargain, like the three we’ll discuss in a moment.

An “Instant” 3-Fund Portfolio Yielding Over 8%

In fact, we’re going to do more than just reveal these CEFs; we’re going to combine them to build ourselves a “mini-portfolio” that delivers an outsized income stream, to the tune of 8% yearly.

Investing simply doesn’t get much simpler than that!

You’ll also get strong diversification—another bit of reassurance in uncertain times: The three funds we’re about to uncover hold stocks, bonds and real estate. Combined, they give you exposure to thousands of assets across the country.

Maximizing Your Savings Potential

Before we go further, let’s put an 8% payout in perspective: If you have $1 million saved, it translates to $80,000 annually, or over $6,600 per month—a substantial amount that could either supplement or even replace your current income.

If you have a million saved and don’t think you can quit working, I wonder if you’ve looked closely at your options. I know many people who have retired on less and are doing great.

Replacing the Average American Income

Consider the average American’s income from a job: about $60,000 yearly. You’d need $750,000 in these three funds to match this solely through dividends.

This calculation underscores the accessibility of income investing: you don’t necessarily need a million dollars to generate a significant income stream, and depending on how much income you need, you might already have enough to clock out.

Now, I realize I’ve made some bold claims here, so let me back them up with a closer look at our three funds—closed-end fund (CEFs), to be precise.

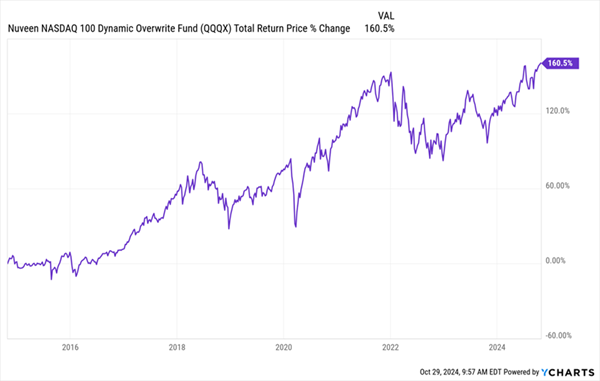

Early-Retirement Pick No. 1: Nuveen Nasdaq 100 Dynamic Overwrite Fund (QQQX)

We’ll start with 6.6%-yielding QQQX, which trades at a 10.8% discount to net asset value (NAV, or the value of the stocks it holds). These discounts are only available with CEFs.

QQQX is known for its focus on US stocks, as it closely tracks the NASDAQ 100. That’s helped it provide stable growth and relatively consistent dividends for a long time—although the stock market hit a bit of a ceiling for a while, causing the fund’s total return to remain channel-bound between 80% and 140% for the last few years, until very recently.

Low-Volatility Payouts and a Long-Term Buying Opportunity

So how does QQQX pay that big dividend if it simply holds NASDAQ 100 stocks? One way is by selling call options on its portfolio. That’s smart because QQQX collects fees from option buyers, no matter if they exercise their right to buy the fund’s stocks.

So how does QQQX pay that big dividend if it simply holds NASDAQ 100 stocks? One way is by selling call options on its portfolio. That’s smart because QQQX collects fees from option buyers, no matter if they exercise their right to buy the fund’s stocks.

That strategy can cap upside as QQQX’s best stocks are sold, or “called away.” But the benefits are the high dividend and additional stability the fund gets as more of its returns come as cash. And with a volatile year-end likely coming our way, that’s something we can all appreciate.

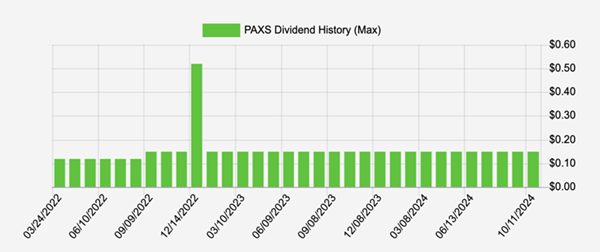

Early-Retirement Pick No. 2: PIMCO Access Income Fund (PAXS)

Next, we’re going to pick up the 11.5%-yielding (not a typo!) PAXS, which holds 325 bonds. That’s a lot of diversification by any measure, but it’s not surprising considering this is a PIMCO fund. The firm is known for its active management, effectively navigating interest-rate changes and seeking out undervalued bonds.

A Steady—and Monthly—Income Stream

Source: Income Calendar

Source: Income Calendar

PAXS has only been around since January 2022, which was lousy timing for the fund to hit the market, given the hit that bonds took as interest rates rose that year. But it’s still returned around 8.2% in that time. Its dividend has also risen, with a special payout in late 2022, as you can see in the chart above.

While PAXS trades at around par in relation to its NAV, that’s not unusual for PIMCO funds, which often trade at bigger premiums due to PIMCO’s strong record. And this one has traded at premiums as high as 9% in recent months, a good sign for future gains.

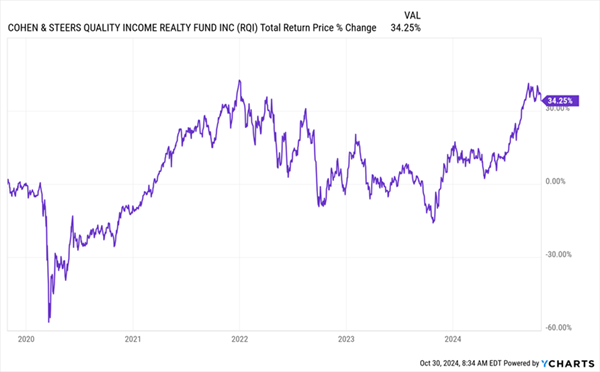

Early-Retirement Pick No. 3: Cohen & Steers Quality Income Realty Fund (RQI)

Let’s top off our three-fund portfolio with RQI, which owns shares of over 100 companies that themselves own thousands of properties between them.

A real estate fund investing in high-quality assets, RQI offers real estate exposure, which of course is a source of steady income. The main benefit is its 7.1% yield, its track record of maintaining payouts and the fact that RQI makes you a part-landlord of thousands of properties, but you never have to deal with a single tenant.

In the top chart below, you can see that the fund has returned 34% in the last five years. Sure, the S&P 500 has posted a total return north of 100% in that time, but that just shows the real estate investment trusts (REITs) that RQI holds remain undervalued, as we discussed last week.

Steady Gains, and Great Value, From “Hands-Off” Real Estate

“Bundling” Our Trio for Income and Growth

“Bundling” Our Trio for Income and Growth

Put it all together and you’ve got an 8.4%-yielding portfolio of diversified high-quality assets.

That puts us on track to replace the average American’s salary with this portfolio with $750,000, and then some, as our three funds generate some $63,000. That’s proof positive that retirement could be closer than you realize.

— Michael Foster

5 Big Monthly Dividends to Buy Now (and How We’ll Profit as Volatility Spikes) [sponsor]

We income investors know that there’s a lot to be said for high, steady 8%+ income streams when uncertainty is everywhere, as it is today.

With the equivalent of the market’s historic annual return coming our way in dividends alone, we get an extra layer of safety that folks who limit themselves to S&P 500 stocks just don’t have.

Even better if we can get those rich dividends to roll our way monthly.

Monthly dividends save us having to manage “lumpy” quarterly payouts, sure. But they also let us reinvest our dividends faster. And you and I both know that every volatile period gives us opportunities to buy our favorite stocks (and funds) cheap.

With monthly dividends, we’ll be ready to deploy our dividends to maximum effect when those opportunities show up.

PAXS and RQI are monthly payers, but there are plenty more like them in CEF-land, with higher yields, too.

Source: Contrarian Outlook