One of the best things about investing is its customizability.

Investors aren’t a gigantic monolith.

We’re all individuals with different lives and different goals.

And that’s why there’s no one “right” way to invest (even though there are some “bad” ways to approach investing).

Individuals can invest in ways that allow them to create portfolios that work for them and their specific goals.

That said, a common goal among investors is the ability to be financially independent.

This is why I’m such an ardent fan of dividend growth investing – a long-term investment strategy that champions the idea of buying and holding shares in high-quality businesses that reward shareholders with safe, growing dividends.

It tends to work out that only great businesses can afford to consistently pay out growing dividends, as that practically requires generating consistently rising profits (which, in turn, requires those businesses to do a lot of things right).

You can see what I mean by perusing the Dividend Champions, Contenders, and Challengers list.

This list has rich data on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

Some of the world’s best businesses are on this list, and rightly so.

Some of the world’s best businesses are on this list, and rightly so.

I’ve been employing this strategy for more than a decade now.

It’s greatly aided me as I’ve gone about building the FIRE Fund, which is my real-money portfolio that throws off enough five-figure passive dividend income for me to live off of.

That circles me back to my original point.

This strategy is inherently effective at guiding investors toward the promised land of financial independence.

It was so effective for me, in fact, that it allowed me to quit my job and retire in my early 30s.

My Early Retirement Blueprint goes over exactly how that played out.

Now, this strategy is effective, but it has to be used correctly.

And a major component of the strategy revolves around valuation.

That’s because price only tells you what you pay, but value tells you what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Repeatedly buying undervalued high-quality dividend growth stocks, and building a large and diversified portfolio of them, is a highly effective way to build wealth, generate passive income, and become financially independent over time.

Of course, all of what I just laid out does assume that one already understands how valuation works.

If you don’t already understand the ins and outs of valuation, make sure to give Lesson 11: Valuation a read.

Written by fellow contributor Dave Van Knapp, it’s a guide that explains valuation in very simple terminology and even provides an easy-to-follow valuation template that can be applied to almost any dividend growth stock out there.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Xylem Inc. (XYL)

Xylem Inc. (XYL)

Xylem Inc. (XYL) is a water technology company.

Founded in 2011, Xylem is now a $32 billion (by market cap) major player in water technology that employs approximately 23,000 people.

Xylem was technically founded in 2011 after being spun out from former parent company ITT Inc. (ITT), but its roots (under ITT) actually date back decades.

As an independent business, Xylem now focuses on providing water technology solutions for commercial and residential customers.

These solutions include the transport, treatment, testing, and more efficient usage of water.

FY 2023 revenue can be broken down across four business segments: Water Infrastructure, 40%; Applied Water, 25%; Measurement & Control Solutions, 24%; and Integrated Solutions & Services, 11%.

Xylem derived 53% of FY 2023 revenue from the US, 23% from Western Europe, 16% from emerging markets, and 8% from other geographies.

Water Infrastructure, the largest segment by revenue, is where a range of Xylem products, such as wastewater pumps, filtration, treatment equipment, and controls are designed to help with the transportation and treatment of water.

The Applied Water segment is where products including pumps and valves are instituted to increase water efficiency for customers.

Measurement & Control Solutions is where products, such as meters and sensors, are used to help with testing.

The Integrated Solutions & Services segment, which was created recently after Xylem acquired Evoqua Water Technologies Corp., a leader in mission-critical water treatment solutions and services, in 2023 for $7.5 billion, specializes in mission-critical water treatment solutions and services.

The transportation, treatment, testing, and more efficient usage of water might seem like a boring business model at first glance.

I’d argue it’s all quite exciting.

Xylem is in the right place at the right time.

Why do I say that?

Well, it’s because water is becoming the “liquid gold” of the 21st century, just as oil was for the last century.

Water scarcity is starting to become a thing.

In the first place, water is a finite resource.

Furthermore, due to a variety of reasons, reliably accessing clean water is becoming increasingly costly and challenging – even though we human beings literally cannot live without clean water.

Against this supply backdrop, urbanization, an increasing global population, and rising global wealth all push demand for clean water (and the necessary infrastructure) higher.

On top of those basic factors, new technologies (such as semiconductor manufacturing and data centers) are extremely thirsty for efficient, clean water.

This is an extremely favorable supply-demand setup for Xylem and its roster of products designed to help with these water-related issues.

Aging water infrastructure in developed countries will need to continually be updated, and new water infrastructure in developing countries will need to be continuously built out.

This is a nearly-guaranteed eventuality.

Water is our most precious resource, and proper management of it is essential.

Since we cannot survive without clean water, all futures point to civilization’s collective demand for it.

This is a secular growth opportunity for Xylem.

With long-term tailwinds strongly blowing its way, this company’s revenue, profit, and dividend should continue to grow briskly over the coming years.

Dividend Growth, Growth Rate, Payout Ratio and Yield

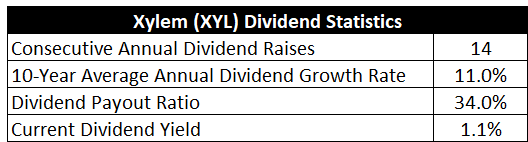

Already, Xylem has increased its dividend for 14 consecutive years.

The 10-year dividend growth rate is 11%, which is strong.

Gotta love double-digit dividend growth, but the stock’s lowish 1.1% yield is the trade-off that one must accept in order to get that higher growth rate.

It’s worth noting this yield is right in line with its own five-year average, so this is a yield level the market has been typically willing to accept from this stock.

This also gives some initial indication of a fairish price on the stock (since the yield is currently neither higher nor lower than it usually is).

A payout ratio of 34%, based on midpoint guidance for this year’s adjusted EPS, shows a very healthy dividend with plenty of headroom to head higher and continue its fast-growth ways.

A payout ratio of 34%, based on midpoint guidance for this year’s adjusted EPS, shows a very healthy dividend with plenty of headroom to head higher and continue its fast-growth ways.

For younger dividend growth investors who like high-quality compounders, or even for those looking to take advantage the secular demand for clean water, Xylem could make a lot of sense.

These are great dividend metrics, especially if one isn’t in need of current income.

Revenue and Earnings Growth

As great as the numbers may be, though, many of them are looking backward.

However, investors must always be looking forward, as the capital of today gets risked for the rewards of tomorrow.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will be instrumental when the time comes to estimate fair value.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Blending the proven past with a future forecast in this manner should give us enough detail to roughly gauge where the business might be going from here.

Xylem moved its revenue from $3.9 billion in FY 2014 to $7.4 billion in FY 2023.

That’s a compound annual growth rate of 7.4%.

Very solid.

But misleading.

Much of this was inorganically helped by a big jump in FY 2023 revenue (because of the aforementioned Evoqua Water Technologies acquisition).

If we back up to FY 2022 and do a nine-year CAGR of revenue, it’s 4.4% – quite good, but this is obviously short of what we see above.

Meanwhile, EPS grew from $1.83 to $3.78 (adjusted) over the last decade, which is a CAGR of 8.4%.

Due to messy FY 2023 GAAP numbers (from acquisition-related special charges), I used adjusted EPS for this year.

Overall, it’s very nice bottom-line growth.

The dividend has been growing slightly faster than EPS, but the payout ratio remains comfortably low.

The outstanding share count did grow during FY 2023 (Xylem equity funded the acquisition), serving as a headwind for per-share profit growth.

Recent numbers have been messy, but it’s hard to doubt that Xylem is now anything but a large, world-class, water infrastructure business.

Looking forward, CFRA is forecasting that Xylem will grow its EPS at a 12% CAGR over the next three years.

See, that’s more like it!

With the acquisition behind the company, it’s off to the races.

CFRA sums up its enthusiasm by noting “…strong demand in utility end markets and multiyear tailwinds stemming from federal infrastructure stimulus, with recovered component and chip availability facilitating [Xylem]’s ability to capitalize on rising orders.”

Also, nearly half of Xylem’s revenue is recurring.

Sticky, recurring revenue stems from inevitable parts and service for the installed base of water infrastructure, as well as the fact that the company has many long-term contracts in place with high (90%+) renewal rates.

I just see so many ways for Xylem to win over the long run.

There is no future in which demand for clean water will suddenly disappear.

With so many levers to pull (infrastructure, data centers, chip fabs, etc.), Xylem almost can’t lose.

A 12% bottom-line growth rate would be this business living up to its potential, and that could easily fuel similar dividend growth.

Assuming no major changes in the valuation, it’s a straightforward path to a low-double-digit annualized total return over the coming years.

Again, the somewhat low yield is a bit of a bummer for income-oriented investors out there, but the compounding possibilities on the back of very necessary water infrastructure are highly appealing.

Financial Position

Moving over to the balance sheet, Xylem has a very solid financial position.

The long-term debt/equity ratio is 0.2, while the interest coverage ratio is nearly 17.

I actually think the balance sheet is even better than these numbers would indicate, as GAAP numbers are temporarily depressed and resulting in a lower interest coverage ratio.

Moreover, net long-term debt (after accounting for cash) is barely over $1 billion, which is relatively immaterial for a company of this size.

Profitability is good, but I’d like to see higher returns on capital.

Return on equity has averaged 11.1% over the last five years, while net margin has averaged 7.2%.

Skewed GAAP numbers are causing issues with returns on capital, but ROE for Xylem has historically (before the pandemic and the big acquisition) been in the 15% range – more than acceptable.

With the acquisition now under Xylem’s belt, I suspect we’ll see dramatic improvements across the board for the combined enterprise over the coming years.

The world’s increasing thirst (pun intended) for access to clean water plays right into Xylem’s strengths as a leading company that caters to the world’s most precious resource.

And with economies of scale, industry know-how, switching costs, IP, R&D, brand power, and an installed base that’s entrenched, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Litigation, regulation, and competition are omnipresent risks in every industry.

I view litigation and regulation as somewhat muted relative to a lot of other business models, but competition across solutions for water is fierce.

Xylem has exposure to geopolitics, currency exchange rates, and sovereign debt loads, as large infrastructure projects (water or otherwise) often emanate from government entities and public spending.

Xylem recently completed its biggest acquisition ever (Evoqua Water Technologies), which introduces integration and execution risks.

Input costs can be volatile, and recent inflationary pressures could be a near-term headwind.

In my view, this business model just isn’t loaded up with risk.

Combining a relatively modest risk profile with enduring demand and lots of recurring revenue helps to explain why this stock is never really cheap, but the current valuation is also not unreasonable…

Valuation

The stock is trading hands for a forward P/E ratio of 30.8, based on midpoint guidance for this year’s adjusted EPS.

Again, far from “cheap”, but this stock’s own five-year average P/E ratio is 46 (although this is affected and skewed by fluctuating GAAP results).

The current P/CF ratio of 23.8 is also not particularly low, but it is slightly lower than its own five-year average of 24.5.

This is a stock that often commands healthy premiums in the marketplace (and unsurprisingly so), but the current level of valuation is, in some ways, in the relative sense, a bit lower than it usually is.

And the yield, as noted earlier, is in line with its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 15-year dividend growth rate of 12%, and a long-term dividend growth rate of 8%.

Xylem’s 10-year demonstrated dividend growth rate of 11% is just slightly lower than what I’m modeling in over the nearer term, but this isn’t at all inconsistent with CFRA’s forecast for EPS growth acceleration.

If EPS growth accelerates meaningfully, it’s not irrational to assume that some of that bleeds down into dividend growth acceleration.

With a high degree of recurring revenue, long-term contracts in place, infrastructure spending up, and enduring demand for clean water, I believe Xylem’s growth visibility extends out further into the future than the average company I look at, which is why I modeled in a somewhat longer stretch of above-average dividend growth.

The DDM analysis gives me a fair value of $126.92.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

This is a stock that looks right about fairly priced to me, which jibes with where its yield is at.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates XYL as a 2-star stock, with a fair value estimate of $114.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates XYL as a 5-star “STRONG BUY”, with a 12-month target price of $155.00.

I came out roughly in the middle here. Averaging the three numbers out gives us a final valuation of $131.97, which would indicate the stock is possibly 3% undervalued.

Bottom line: Xylem Inc. (XYL) is a compelling investment opportunity in water technology and infrastructure, and it’s in a prime position to take advantage of the world’s increasing thirst for access to clean water. A high degree of recurring revenue and lots of levers to pull. There are so many ways for Xylem to win. With a market-like yield, double-digit dividend growth, a low payout ratio, nearly 15 consecutive years of dividend increases, and the potential that shares are 3% undervalued, this could be one of the best ways for long-term dividend growth investors to tap into the the 21st century’s “liquid gold”.

Bottom line: Xylem Inc. (XYL) is a compelling investment opportunity in water technology and infrastructure, and it’s in a prime position to take advantage of the world’s increasing thirst for access to clean water. A high degree of recurring revenue and lots of levers to pull. There are so many ways for Xylem to win. With a market-like yield, double-digit dividend growth, a low payout ratio, nearly 15 consecutive years of dividend increases, and the potential that shares are 3% undervalued, this could be one of the best ways for long-term dividend growth investors to tap into the the 21st century’s “liquid gold”.

-Jason Fieber

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Note from D&I: How safe is XYL’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 66. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, XYL’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

Source: Dividends & Income

Disclosure: I have no position in XYL.