Let’s be honest: after the year we’ve just put in, we’re all exhausted. But we can’t let our guard down. Because at times like these, it’s easy to let alarmist headlines skew our buy and sell decisions.

Worse, the clamor, and almost always incorrect market predictions that dominate the news these days, can lure you away from the reliable dividend payers you need to fund your retirement.

I hate to see that happen to investors—especially when they could easily use high-yield closed-end funds (CEFs) to retire on dividends alone. I’ve got three “low-drama” CEFs that can get you there, thanks to their outsized 8.1% average yield. All three also boast strong dividend growth and price upside, too. More on this high-yield trio shortly.

There’s Only One Retirement “Rule” You Need to Know

It seems that when most investors do pay attention to retirement planning, they obsess over a random sum advisors or pundits say they need to retire: $1 million, $2 million or whatever. Then they quickly get discouraged.

That’s understandable, but the truth is, everyone’s situation is different, and there’s really only one “rule” that matters: your income in retirement has to exceed your spending. This is where CEFs give you a big advantage.

Source: CEF Insider

Source: CEF Insider

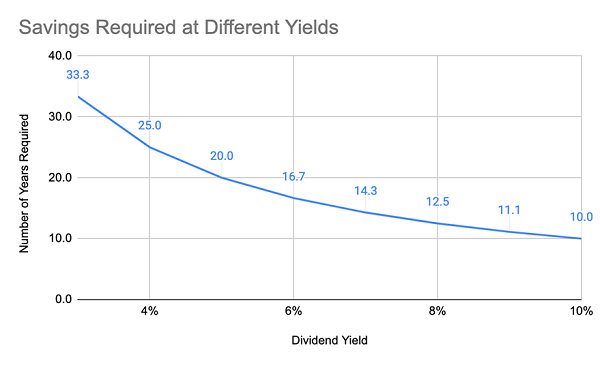

In the above chart, we see how much the average American must save to pull $30,000 a year in dividend income from their portfolio at different yields. At a 3% yield, for example, they’d need to save around a million dollars, or a whopping 33.3 years’ worth of their planned yearly retirement spending, to get that $30K in yearly income. If they plan to spend $60,000 a year, they’d need at least $2 million.

Of course, the higher your yield, the less you need to save. On a 6% yield, the amount you’d need to save drops in half—so you’d require $1 million for $60,000 in yearly dividend income.

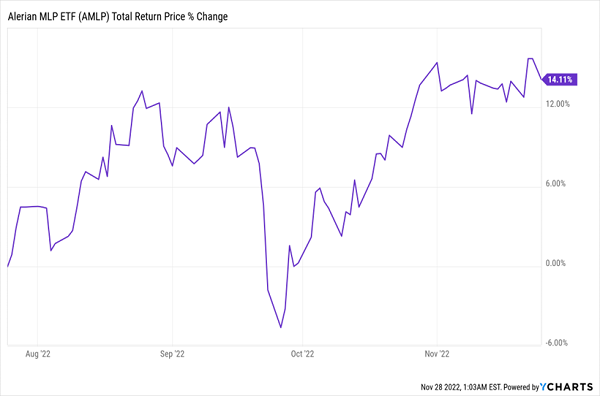

There’s just one problem: the higher your yield, the more risk you tend to take on. I remember, for example, oil bulls pushing the Alerian MLP ETF (AMLP) and similar high-yield energy investments back in 2014. (AMLP is a passive ETF that holds master limited partnerships, or MLPs, which mainly own oil and gas pipelines and storage facilities.)

AMLP’s 7% yield didn’t seem overly risky at the time, but then oil demand and prices fell, taking AMLP down with them.

Even so, it has been possible to play AMLP for short-term bounces. Buying in July 2022, for example, paid off nicely.

AMLP’s Short-Term Recovery

The takeaway? Buying based solely on a high yield, like those AMLP buyers of seven years ago, can produce price losses that quickly overrun your high income stream. The better play? Set ourselves up with a strong chance of price upside to go along with our rich payouts.

The takeaway? Buying based solely on a high yield, like those AMLP buyers of seven years ago, can produce price losses that quickly overrun your high income stream. The better play? Set ourselves up with a strong chance of price upside to go along with our rich payouts.

Actively managed CEFs, as members of my CEF Insider service know, can give us high yields and the kind of price upside you’d expect from stocks.

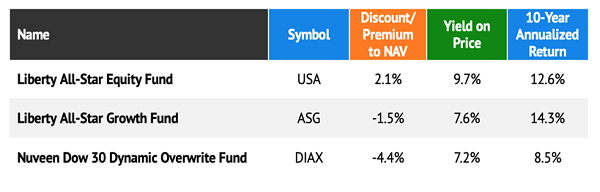

3 Great Equity CEFs to Consider Now

The simple three-CEF portfolio below soars above most other income options because it boasts three key strengths:

- It gives you strong US blue chip stocks for less than you’d pay if you bought them directly.

- It pays an average dividend yield of 8.1% (cutting our required savings to 12.5 years’ worth from the 33 years our typical investor would need).

- Broad diversification across the US economy.

Each of the three funds above, the Liberty All-Star Equity Fund (USA), the Liberty All-Star Growth Fund (ASG) and the Nuveen Dow 30 Dynamic Overwrite Fund (DIAX), focus on high-quality US equities, which have performed well over the last decade. That’s helped these CEFs maintain their high dividends as their management teams take profits in bull markets, hand those gains to their shareholders as payouts, then go bargain hunting during pullbacks.

Each of the three funds above, the Liberty All-Star Equity Fund (USA), the Liberty All-Star Growth Fund (ASG) and the Nuveen Dow 30 Dynamic Overwrite Fund (DIAX), focus on high-quality US equities, which have performed well over the last decade. That’s helped these CEFs maintain their high dividends as their management teams take profits in bull markets, hand those gains to their shareholders as payouts, then go bargain hunting during pullbacks.

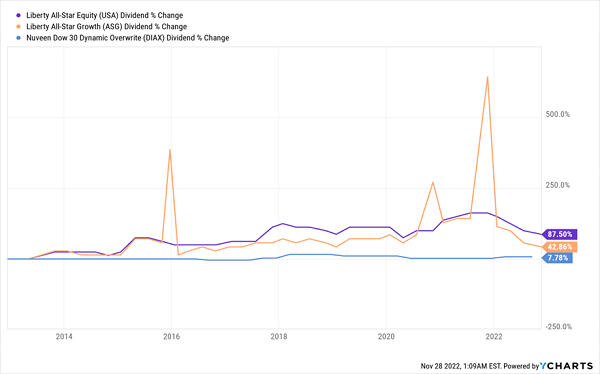

This explains why dividends for this three-CEF portfolio have risen in the last decade, with USA and ASG doing most of the heavy lifting. (ASG has offered periodic special dividends, as well, which are visible as the three orange spikes below):

Growing High Yields

You’ll also notice that dividend payouts for ASG and USA (in orange and purple above) tend to fluctuate. This is because these funds commit to paying out a percentage of their net asset value (NAV, or the value of their portfolios) in dividends every year: 10% in the case of USA and 8.1% for ASG.

You’ll also notice that dividend payouts for ASG and USA (in orange and purple above) tend to fluctuate. This is because these funds commit to paying out a percentage of their net asset value (NAV, or the value of their portfolios) in dividends every year: 10% in the case of USA and 8.1% for ASG.

This approach is especially timely now, as the 2022 decline has set up these funds with opportunities to pick up bargains they should be able to sell for higher prices down the road. That would translate into further dividend growth for their shareholders.

Low Leverage, Option Strategy Add Appeal

Finally, these three funds use basically no leverage, which is a plus in today’s rising-rate environment (though it should be noted that most CEFs, including those I recommend in CEF Insider, have access to much cheaper credit than pretty well any consumer could get).

In addition, DIAX gets extra income from its covered-call strategy, under which it sells the option to buy its holdings to investors at a fixed price and a fixed date in the future. The company keeps the fees it charges for these options, whether the investor ends up buying the stock or not.

And what about those holdings? As mentioned, USA, ASG and DIAX all own high-quality large-cap US firms with strong cash flows—companies like Microsoft (MSFT), Apple (AAPL), UnitedHealth Group (UNH) and Goldman Sachs (GS). The strong performance of US large caps like these over the last decade has meant that investors who bought these three CEFs back then are thriving—an outcome I expect for today’s buyers 10 years from now.

Yours in profits and safety,

Michael Foster

4 MORE Perfect Retirement CEFs Yielding 9.5% [sponsor]

DIAX, ASG and USA are “cornerstone” CEFs—they’ve been around so long that folks who invest in these funds know their tickers by heart!

They’d make solid additions to any portfolio. But if you go just one step further, you can get even higher CEF dividends, with greater stability. And you can get your payouts monthly, too.

That’s what you get with the four CEFs I’ve recently uncovered. They yield an incredible 9.5%, pay you every single month (in line with your bills) and trade at such deep discounts that I’m calling for 20%+ price upside in the next 12 months!

Click here and I’ll tell you how to get all of my research on these 4 retirement lifesavers, with their huge monthly dividends, in a free Special Report. It includes names, tickers, current yields and a full breakdown of each fund’s holdings. Don’t miss your chance to pick up these reliable income plays while they’re still bargains.

Source: Contrarian Outlook