The media is filled with articles regarding companies that writers tout as solid investments, but there aren’t nearly as many discussing which stocks the writers think would be best left untouched. Yet avoiding bad stocks is just as important to your long-term returns as buying the great ones.

In my view, there are pretty clear reasons to steer clear of Space Exploration Technologies (SPCX), Palantir (PLTR), and AMD (AMD), and they all boil down to one issue: valuation. Regardless of the health of the underlying businesses behind them, all three of these stocks’ run-ups have significantly outpaced their actual financial results.

1. SpaceX

Although SpaceX is the new hotness on the market, I think it’s a stock investors should steer clear of. The reality is quite simple: SpaceX doesn’t have the financials to justify a trillion-dollar market cap, let alone its current $2.1 trillion valuation. In 2025, it generated $18.7 billion in revenue.

That indicates a price-to-sales ratio of 112. Generally, a stock trading at 20 to 30 times sales is viewed as overvalued. When one reaches 100 times sales, alarms should be sounding in investors’ heads.

Very few companies maintain valuations above 100 times sales for long, as stocks normally correct to more closely align with actual business results. I think such a correction could be coming for SpaceX in the months ahead, as the combination of IPO hype and an extremely small public float was bound to boost the stock during its first trading days.

Very few companies maintain valuations above 100 times sales for long, as stocks normally correct to more closely align with actual business results. I think such a correction could be coming for SpaceX in the months ahead, as the combination of IPO hype and an extremely small public float was bound to boost the stock during its first trading days.

As lock-up periods expire in the weeks and months ahead and insiders are allowed to sell, the market will be flooded with more and more shares. That increased supply in the face of static demand could cause the stock to tumble.

SpaceX’s businesses may have a bright future ahead, but far too much of that hoped-for future is already baked into the stock price.

2. Palantir

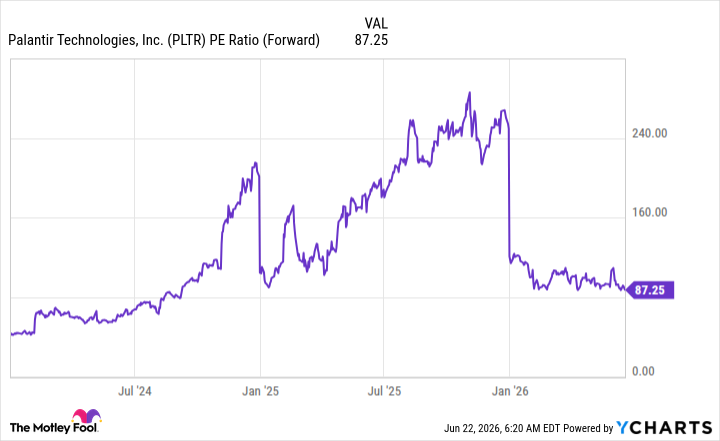

Palantir has been a market darling since the artificial intelligence trend kicked off in 2023. However, over the last few months, its performance has been a bit rocky. The stock is down nearly 40% from its all-time high, and even that sell-off may not be enough to bring its valuation into alignment with its results.

Palantir is generating real profits (unlike SpaceX), but it’s not generating enough of them to justify its share price. It trades at 87 times forward expected earnings. That may be more reasonable than SpaceX, but it’s still expensive.

The company has solid AI-powered data analytics software and an impressive 85% revenue growth rate going for it. However, Palantir’s stock could continue to face downward pressure because there is just too much possibly future growth priced into the stock. That makes for a dangerous investment, and I am steering clear of it as a result.

The company has solid AI-powered data analytics software and an impressive 85% revenue growth rate going for it. However, Palantir’s stock could continue to face downward pressure because there is just too much possibly future growth priced into the stock. That makes for a dangerous investment, and I am steering clear of it as a result.

3. AMD

AMD falls into the same category as Palantir; it’s a solid company with a good product, but the financials and the stock price just don’t match up. AMD’s stock trades at 73 times forward earnings — a slightly less lofty ratio than Palantir. But its growth rate isn’t better, as its revenue rose by 38% year over year during Q1.

Wall Street analysts expect some improvement, with revenue growth projections for 2026 and 2027 of 43% and 54%, respectively. However, why would you buy AMD over its chief rival, Nvidia (NVDA), when Nvidia is growing much faster?

Wall Street analysts expect some improvement, with revenue growth projections for 2026 and 2027 of 43% and 54%, respectively. However, why would you buy AMD over its chief rival, Nvidia (NVDA), when Nvidia is growing much faster?

Its top line increased by 85% in Q1. Nvidia also trades at a far cheaper 23.5 times forward earnings. Lastly, AMD’s product lineup is inferior to Nvidia’s, and Nvidia has a much larger market share in the key AI accelerator market.

With all that in mind, I think AMD is a stock to avoid. There are far better AI stock options out there.

— Keithen Drury

Motley Fool Stock Advisor's average stock pick is up over 350%*, beating the market by an incredible 4-1 margin. Here’s what you get if you join up with us today: Two new stock recommendations each month. A short list of Best Buys Now. Stocks we feel present the most timely buying opportunity, so you know what to focus on today. There's so much more, including a membership-fee-back guarantee. New members can join today for only $99/year.

Source: The Motley Fool