This Iran deal adds one more tailwind to our (already surging) 8%+ paying closed-end funds (CEFs).

It’s just one more “boost,” on top of many others, that point to more upside ahead for these proven income plays.

Why do I say that? Because if the agreement holds up (and that’s still uncertain at this point), oil will likely continue its retreat. That, in turn, sets the stage for lower inflation—and falling interest rates, too.

And the lower rates go, the better CEFs tend to perform.

That makes now, while rates remain elevated, the time to make our move. And the Neuberger Berman Next Generation Connectivity Fund (NBXG), a recent addition to the CEF Insider portfolio, is a solid option that’s clinging to an undeserved double-digit discount.

The fund is a strong play on continued AI growth, as it holds top tech names like NVIDIA (NVDA) and Amazon.com (AMZN), as well as smaller, private IT firms.

The dividend? A rich 8.7%. And even though tech has been driving the market for years now, NBXG trades at that discount to net asset value (NAV) I just mentioned: 14.4%, to be exact. So we can essentially pick this one up for less than 86 cents on the dollar.

I’m bullish on NBXG because tech stocks are rate-sensitive, and as rates fall, the value of their future earnings rises.

Moreover, as oil retreats, companies across the economy will have more cash freed up for capital expenses. And AI, with its promise of higher productivity, will likely be among their top investment priorities. That’s particularly true of the nation’s smaller businesses, which are already among AI’s fastest adopters.

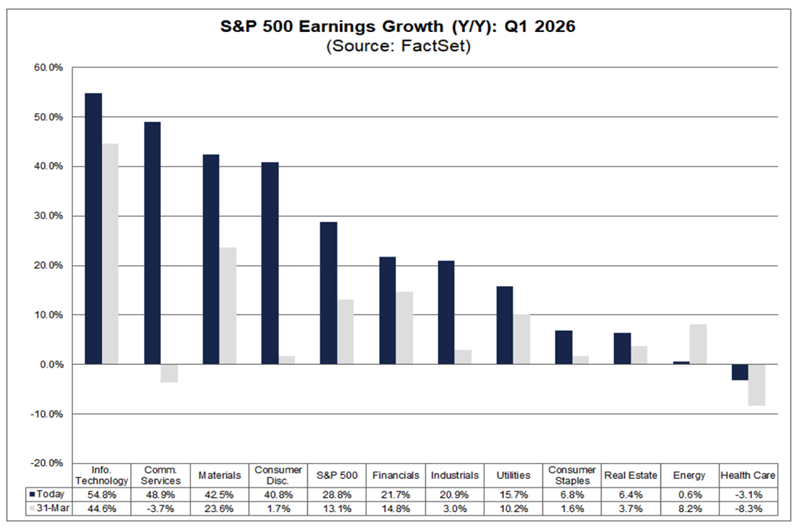

Those potential gains come on top of fundamentals—by that we mean growth in corporate sales and earnings—that are already surging across the economy, according to the latest data from FactSet:

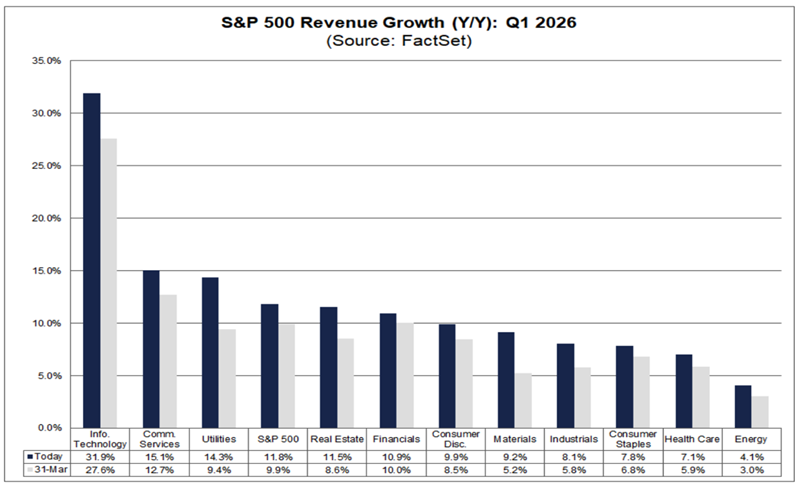

As of the end of the first quarter, S&P 500 earnings are growing 28.8% year-over-year. That figure omits seasonal variation, so it’s a reliable growth indicator. The sales backstopping those profits are also rising sharply:

With 11.8% year-over-year revenue-growth across the S&P 500, we can see that sales are growing much faster than inflation, indicating that consumer spending is not only holding up, but growing.

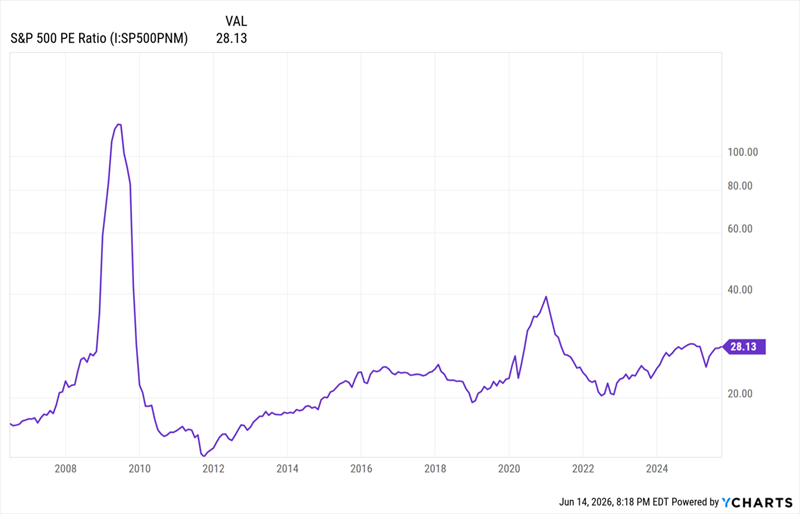

This data justifies more stock gains on its own. But we do have to take the market’s valuation into account, so let’s do that:

“High” P/E Reflects the Market’s Earnings Growth

With a P/E ratio of 28.1, the index is far above its average of around 16.2. In fact, it’s nearly double. That sounds bearish on the surface, but let’s dig a bit deeper.

First, today’s levels are far below the near-40 the index’s P/E ratio hit in 2021. And that ratio was hit because earnings weren’t growing enough to match the price gains in stocks. Today it’s the opposite, with earnings growth of 28.8% on a year-over-year basis outpacing the 26% price gains in stocks over the last year.

Second, that long-term average of 16.2 includes data going back to the 1800s, when margins were smaller and growth was meager compared to today’s fast-paced economy. With earnings growing as fast as they are, prices need to grow to catch up—and then some, to pay sellers of stocks a premium due to the fact that stock earnings growth is accelerating at a historically high clip.

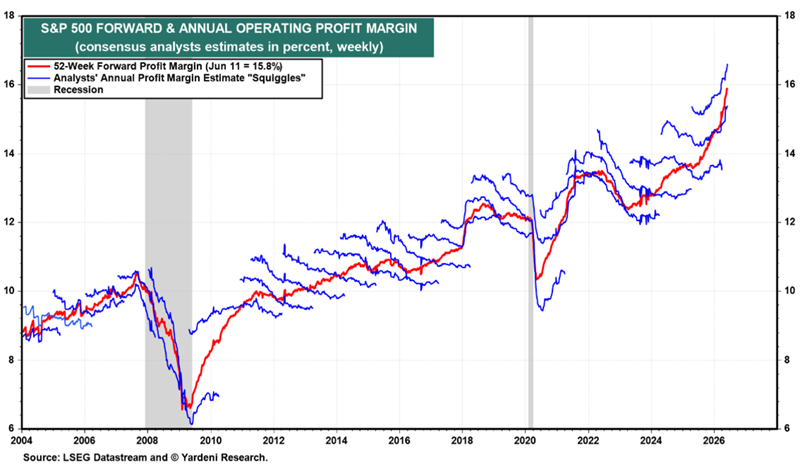

Third, and more important, remember that operating margins are rising, which is key here.

Note how in this chart, from Yardeni Research, profit margins (the red line) are heading almost straight up after recovering in 2024. This shows, in stark terms, the effect of AI making the economy more efficient and, by extension, sending profits on that double-digit ride we just talked about.

Higher profit margins are worth more to investors, so when you measure the stock market on a price-to-earnings ratio, you should expect that ratio to naturally rise as people pay more for more profitable companies.

An 8.7% Tech Dividend That Grows

There are plenty of equity-focused CEFs in our CEF Insider portfolio that are nicely positioned to profit from a continued market run-up while delivering high yields: The average CEF tracked by CEF Insider now yields 8.7%, while having an average 6% discount to NAV. That discount was much higher at the start of the year, but bullish appetites are driving prices higher.

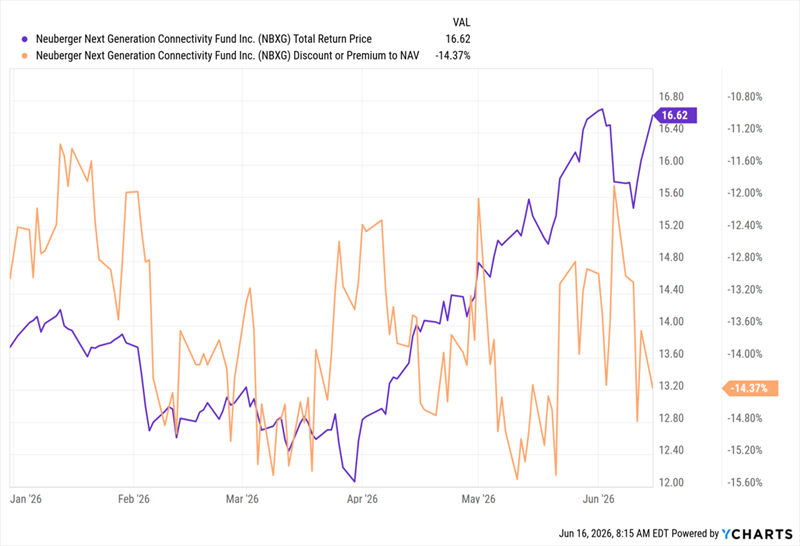

That bullish trend looks set to continue, which brings me back to NBXG, whose 13.7% discount is a real standout. And, as we can see in orange below, that discount is nearing lows reached in March, when NBXG’s total return on the year (in purple) was much lower than it is now.

NBXG Goes On Sale, Despite Its Gains

NBXG has also booked a 21% total return on the year, far above the market’s 9.1% return, so it should be getting more bids. Meantime, its underlying NAV has risen 22% on the year so far, much more than management would need to fund the next year of payouts on its own, at the current distribution rate.

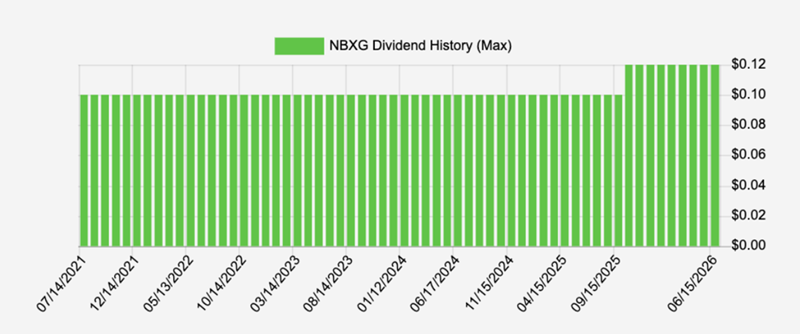

The fund’s strong performance in recent years prompted management to hike the already healthy payout last year, and more hikes are likely as economic growth continues and rates move lower:

Source: Income Calendar

Put it all together and we’ve got a strong, reliable income stream we can collect while we wait for NBXG’s discount to close, propelling the fund’s price higher as it does.

— Michael Foster

4 Huge Dividends (10% on Average) Built for the Critical “Pivot Point” Ahead

NBXG is a great play on the productivity surge AI is unleashing. And we’re going to go one step further, balancing the fund’s tech holdings with shares of companies from across the economy using AI to supercharge their profits.

I’m talking insurance firms, banks and pharmaceutical makers. Thanks to AI, they’re slashing costs, making better decisions and, in the case of pharma stocks, bringing new treatments to market faster than ever before.

The 4 other CEFs I’m urgently recommending now cover all these areas. They’re cheap today, but I don’t expect that to last as rates move lower. And they kick out an outsized 10% dividend, too.

Source: Contrarian Outlook