Zacks Rank #3 (Hold) stock Arm Holdings (ARM) is a British software design company that is a foundational architect for the modern technological era. Unlike traditional semiconductor stocks like NVIDIA (NVDA) or Advanced Micro Devices (AMD), which design physical chips, ARM’s business focuses on designing the blueprints (processor architecture).

Then, rather than producing the chips themselves, ARM licenses its architecture to major technology companies, including NVIDIA, Apple (AAPL), and Qualcomm (QCOM). ARM’s RISC-based (Reduced Instruction Set Computing) processor is known for producing some of the most energy-efficient technology and is used in most of the world’s most popular consumer electronic devices, such as the Apple iPhone.

ARM Holdings: A High Margin, Asset-Light Business

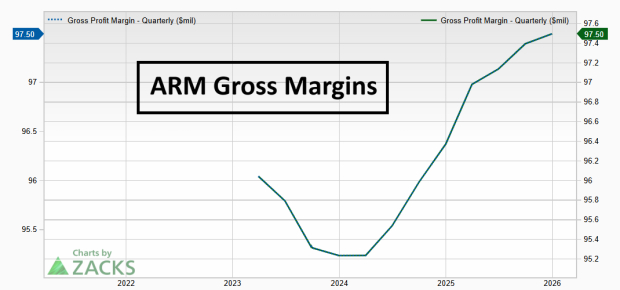

Because of ARM’s unique, asset light business model, the company enjoys a high-margin business. ARM collects upfront fees and royalties on every chip containing its technology. In other words, ARM has the holy grail for a fundamentally strong company – low costs and a recurring revenue stream that is independent of manufacturing expenses. ARM’s 97.5% gross margin (total revenue – cost of goods sold) is exceptional.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Meanwhile, the company’s margins are likely to only expand from here. ARM’s latest Armv9 architecture is experiencing heavy demand and higher royalty rates per chip, especially in the booming premium smartphone and data center businesses.

ARM Announces First In-house AI-Focused Chip

Although ARM’s business is already strong, the company announced Tuesday that it will be releasing its own AI-focused data center chip. The chip will focus on powering Agentic AI in data centers. Agentic AI is currently the fastest-growing area of the AI industry.

Adding credence to the new chip’s potential is the fact that Meta Platforms (META) has agreed to be the “anchor customer” for the new chip. CEO Rene Haas indicated that the new data center chip will ignite revenue growth. In fact, Haas predicts that the new data center chip business could generate ~$15 billion in annual revenue in “about five years.”

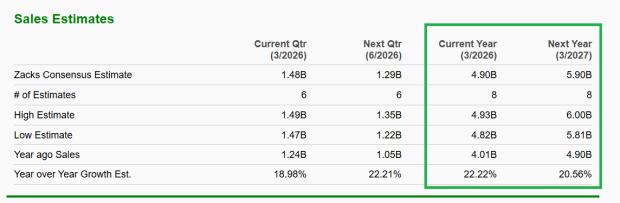

Considering that ARM’s 2025 annual revenue was roughly $4 billion, any revenue performance near the CEO’s prediction would be spectacular. Zacks Consensus Estimates suggest that ARM will grow revenue by ~20% over the next few years. However, I expect that Wall Street will be forced to raise forward estimates in the coming months as they factor in the large potential of an in-house chip.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

ARM News Produces Episodic Pivot

An episodic pivot is a technical analysis pattern that occurs when a stock gaps up significantly on heavy trading volume in response to a major fundamental catalyst. ARM’s 15% gap on massive volume (5x the norm), coupled with the new chip catalyst, means that Wednesday’s gap up is buyable.

Image Source: TradingView

Image Source: TradingView

— Andrew Rocco

Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report.

Source: Zacks