Anything worth building is worth building right.

That couldn’t be more true than when it comes to financial independence.

If you’re going to seek financial independence out, it should be sought after in a way that nearly guarantees long-term sustainability as it’s being achieved.

The last thing anyone would want is to reach the mountaintop only to come crashing back down because the foundation they stood upon wasn’t built to last.

This is why I’m such a fan of dividend growth investing.

This is a long-term investment strategy involving the buying and holding of shares in high-quality businesses paying out reliable, rising cash dividends to shareholders.

It’s nearly a perfect strategy as it pertains to creating lasting financial independence.

It’s nearly a perfect strategy as it pertains to creating lasting financial independence.

And that’s because it tends to funnel investors right into some of the world’s best businesses.

You’ll see what I mean by taking a look at the Dividend Champions, Contenders, and Challengers list.

That list has invaluable information on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

There’s a circular relationship at play.

It takes profit that consistently grows in order to afford steadily rising cash dividend payouts, and it takes a great business to be able to generate profit that consistently grows.

Well, great businesses built to last are the sturdy investment foundation upon which one can confidently stand, and reliable dividend income that’s steadily growing is the lifespring upon which financial independence can flow.

This thought process is what I’ve used to build the FIRE Fund – that’s my real-money portfolio generating enough five-figure passive dividend income for me to live off of – become financially independent myself, and even retire in my early 30s.

My Early Retirement Blueprint details how such an early retirement is possible.

My Early Retirement Blueprint details how such an early retirement is possible.

As important as it is to invest in great businesses, investing at great valuations might be just as important.

While price is what you pay, value is what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Steadily buying undervalued high-quality dividend growth stocks is a great way to slowly build a portfolio that can become the sturdy foundation for durable financial independence.

Now, taking advantage of undervaluation first requires one to know what to look for.

That’s where Lesson 11: Valuation comes in.

Written by fellow contributor Dave Van Knapp, it describes the ins and outs of valuation using simple terminology and even provides an easy-to-use valuation template that you can apply on your own.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Abbott Laboratories (ABT)

Abbott Laboratories (ABT)

Abbott Laboratories (ABT) is a US-based multinational medical devices and health care company.

Founded in 1888, Abbott Laboratories is now a $187 billion (by market cap) healthcare colossus that employs nearly 115,000 people.

The company reports results across four segments: Medical Devices, 48% of FY 2025 revenue; Diagnostics, 20%; Nutrition, 19%; and Established Pharmaceuticals, 12%.

Approximately 40% of the company’s revenue comes from the US, the remainder is derived internationally.

Whereas a lot of healthcare companies are laser focused on one particular area, Abbott Laboratories has taken a broad approach.

With global healthcare facing secular growth from a worldwide population continuing to grow larger, older, and wealthier – simultaneously – companies that can cater to various aspects of healthcare are positioned to ride that wave.

After all, if we have more humans who need quality healthcare from greater aging and have the means to afford quality healthcare, it stands to reason that demand for all kinds of healthcare products and services will rise over time.

Abbott Laboratories is in a fantastic position to capture a large portion of that rising demand, as its products run the gamut of healthcare.

We’re talking monitoring devices, pharmaceuticals, stents, etc.

In fact, this company covers the lifespan of a human being, offering everything from infant formula to pacemakers.

Abbott Laboratories takes a diversified, almost can’t-miss approach to secular growth across global healthcare, promoting steady revenue, profit, and dividend growth.

Dividend Growth, Growth Rate, Payout Ratio and Yield

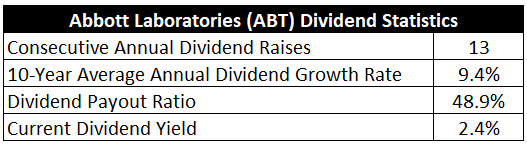

Indeed, Abbott Laboratories has increased its dividend for 13 consecutive years.

However, that’s merely based on a technicality.

In reality, Abbott Laboratories is actually a Dividend Aristocrat – a vaunted status reserved for companies that have increased dividends for at least 25 consecutive years.

This strange discrepancy exists because Abbott Laboratories spun out certain pharmaceutical assets by creating AbbVie Inc. (ABBV) back in 2013.

This move split the dividend into two and “reset” the dividend from Abbott Laboratories alone, but shareholders of Abbott Laboratories who kept their new AbbVie shares were made whole and saw their dividend income continue to rise straight through this process.

Putting that aside, Abbott Laboratories has increased its dividend for 54 consecutive years, putting it in elite territory as a Dividend King.

Its 10-year dividend growth rate is 9.4%, which is strong.

Its 10-year dividend growth rate is 9.4%, which is strong.

And you pair that high-single-digit dividend growth with the stock’s market-beating yield of 2.4%.

That yield is 70 basis points higher than its own five-year average, giving us an early sign that there might be something opportunistic occurring here.

And with the payout ratio sitting at 48.9%, based on adjusted EPS, the dividend looks about as healthy as ever.

This Dividend King offers a nice, safe yield backed by growth nearly in the double digits.

It’s exceptional.

Revenue and Earnings Growth

As exceptional as it may be, though, that stems largely from prior events.

However, investors must always be thinking about what’s yet to come, as the capital of today gets risked for the rewards of tomorrow.

Thus, I’ll now build out a forward-looking growth trajectory for the business, which will be of use when running the valuation model.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

And I’ll then reveal a professional prognostication for near-term profit growth.

Lining up the proven past with a future forecast in this manner should allow us to confidently judge where the business could be going from here.

Abbott Laboratories grew its revenue from $20.8 billion in FY 2016 to $44.3 billion in FY 2025.

That’s a compound annual growth rate of 8.8%.

Solid, solid top-line growth out of a mature healthcare business, especially considering that Abbott Laboratories has not been particularly active around acquisitions over this period.

That said, Abbott Laboratories did announce in November a deal to acquire cancer test maker Exact Sciences Corporation (EXAS) for approximately $21 billion, a move which will add about $3 billion to the top line right from the start.

Meanwhile, earnings per share increased from $0.94 to $3.72 over this period, which is a CAGR of 16.5%.

This is outstanding performance, but it should be noted the company experienced tailwinds over the last several years from an explosion in demand for testing devices stemming from the pandemic.

Still, if we zoom into recent results out of Abbott Laboratories, its Q4 FY 2025 report showed 12% YOY adjusted EPS growth – and this is with the pandemic well behind us.

Plus, the Exact Sciences acquisition is expected to be EPS accretive by 2028, which is something for shareholders to be excited about.

Looking forward, CFRA projects that Abbott Laboratories will compound its EPS at an annual rate of 10% over the next three years.

This would actually line up precisely with full-year adjusted EPS growth for FY 2025.

Moreover, Abbott Laboratories is guiding for $5.68 in adjusted EPS at the midpoint for FY 2026, which would represent 10.3% YOY growth.

A trend is clear.

CFRA cites strong positions in key healthcare product categories, a focus on high-margin medical devices, and the company’s expansion into oncology as reasons to be enthusiastic.

On the flip side, Abbott Laboratories has been facing issues in Nutrition, mainly via infant formula.

Balancing everything out, seeing as how Abbott Laboratories is consistently putting out 10% or better EPS growth, I think CFRA’s forecast is reasonable.

That sets up the company for like dividend growth over the coming years, which means that 9%+ proven 10-year dividend growth rate is positioned to continue.

It’s status quo, and the status quo is great.

Putting that 9% to 10% dividend growth on top of the starting yield adds up to a low-double-digit annualized total return, assuming a static valuation.

On a reliable Dividend King, I think that’s terrific.

Financial Position

Moving over to the balance sheet, Abbott Laboratories has a great financial position.

The long-term debt/equity ratio is 0.3, while the interest coverage ratio is 17.

Abbott Laboratories has credit ratings well into investment-grade territory: Aa3, Moody’s; AA-, S&P.

Also, contrary to a lot of companies I cover, long-term debt has been steadily decreasing over the last decade.

The balance sheet has been managed extremely well and continuously improving, which is what set up the ability to pounce on the Exact Sciences acquisition (an event that will temporarily weigh on the balance sheet).

Profitability is robust.

Return on equity has averaged 23.4% over the last five years, while net margin has averaged 18.3%.

ROIC is routinely in the mid-teens area.

Abbott Laboratories is generating high returns on capital – a hallmark of a high-quality business – without a lot of leverage, which is impressive.

From top to bottom, this is a high-caliber business perfectly positioned to capture a large portion of the secular growth to come from a global population growing larger, older, and wealthier.

And with economies of scale, IP, R&D, entrenched sales relationships, technological know-how, regulatory expertise, and barriers to entry, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

In my view, all three of these risks are relatively high for this particular business model.

Litigation, in particular, has been a rising risk, as evidenced by judgments related to the company’s baby formula.

On the other hand, regulatory hurdles, especially around medical devices, are barriers to entry that stave off new competition.

Product recalls are a consistent risk in this industry.

The Exact Sciences acquisition introduces near-term execution risk.

Being an international company, it’s exposed to geopolitics and exchange rates.

The company has had issues with formula in recent years, indicating intermittent shortcomings around quality and manufacturing.

A proliferation of GLP-1s may reduce demand for some of the company’s various products.

The company’s medical devices are exposed to technological obsolescence risk.

While there are certainly some risks to be aware of, it’s also important to be aware of the company’s quality, performance, and positioning.

Also worth having top of mind is the valuation, which looks attractive after an inexplicable 20%+ slide in the stock’s price…

Valuation

The P/E ratio has compressed to 20.6, based on adjusted EPS for FY 2025.

That compares quite well to its own five-year average P/E ratio of 26.6.

If we take midpoint guidance for this year’s adjusted EPS, the forward P/E ratio drops to 18.7.

These are reasonable, if not downright compelling, multiples for a business of this caliber and reliability.

The sales multiple of 4.2 is well below its own five-year average of 4.9.

And the yield, as noted earlier, is significantly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a dividend discount model analysis.

I factored in a 10% discount rate and a long-term dividend growth rate of 8%.

That long-term growth rate is as high as I’ll allow for in the model, but I think Abbott Laboratories deserves the benefit of the doubt.

This is a Dividend King that has demonstrated a rare level of consistency and staying power.

More than 50 years into its dividend growth journey, the dividend is still growing at a high-single-digit rate.

And based on recent EPS growth, along with near-term expectations, there’s no reason to believe that high-single-digit dividend growth won’t continue.

The DDM analysis gives me a fair value of $136.08.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

From my viewpoint, this Dividend King looks downright cheap after the pullback.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates ABT as a 3-star stock, with a fair value estimate of $115.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates ABT as a 3-star “HOLD”, with a 12-month target price of $122.00.

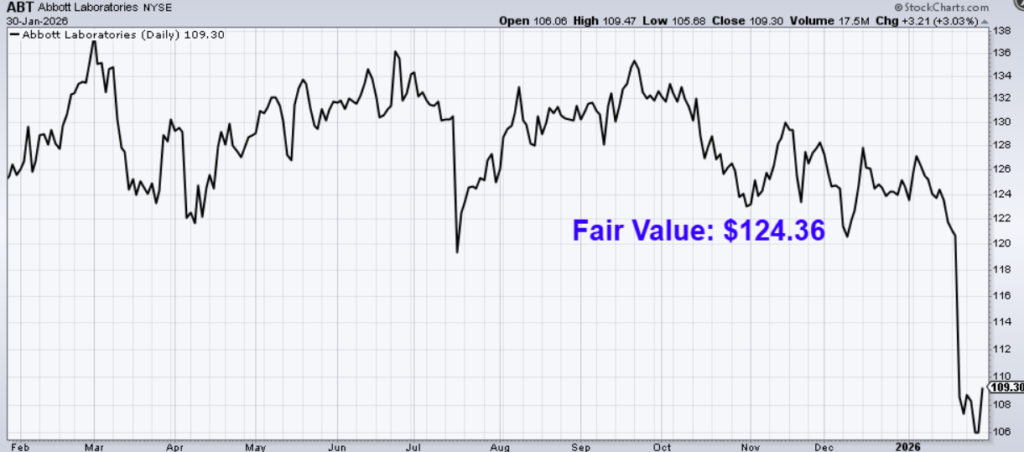

We have a small spread, but we all agree a discount appears to be present. Averaging the three numbers out gives us a final valuation of $124.36, which would indicate the stock is possibly 15% undervalued.

Bottom line: Abbott Laboratories (ABT) is a world-class healthcare company positioned extremely well within the secular growth wave coming from a global population that’s becoming larger, older, and wealthier – all leading to rising healthcare demand and spending. With a market-beating yield, a balanced payout ratio, high-single-digit dividend growth, more than 50 consecutive years of dividend increases, and the potential that shares are 15% undervalued, this Dividend King looks like a fantastic long-term investment opportunity for dividend growth investors.

Bottom line: Abbott Laboratories (ABT) is a world-class healthcare company positioned extremely well within the secular growth wave coming from a global population that’s becoming larger, older, and wealthier – all leading to rising healthcare demand and spending. With a market-beating yield, a balanced payout ratio, high-single-digit dividend growth, more than 50 consecutive years of dividend increases, and the potential that shares are 15% undervalued, this Dividend King looks like a fantastic long-term investment opportunity for dividend growth investors.

-Jason Fieber

Note from D&I: How safe is ABT’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 90. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, ABT’s dividend appears Very Safe with a very unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Source: Dividends & Income

Disclosure: I’m long ABT.