Let’s talk about a terrific 12.2% dividend that is paid monthly.

The source of this income? Safe US Treasuries and a methodical scraping of option premiums for additional yield.

We’ll talk about this monthly payer—including fund name and ticker—in a moment. First, let’s get caught up on the Treasury market.

You may have tuned out Treasuries as a potential investment when DOGE austerity efforts gave way to the Big Beautiful Bill. Uncle Sam, already a $36 trillion debtor, dug himself deeper into financial quicksand.

Who wants to lend to that guy? Certainly not bond investors, who demand higher compensation—higher percentage payouts—to offset the credit risk posed by Sam’s ugly balance sheet.

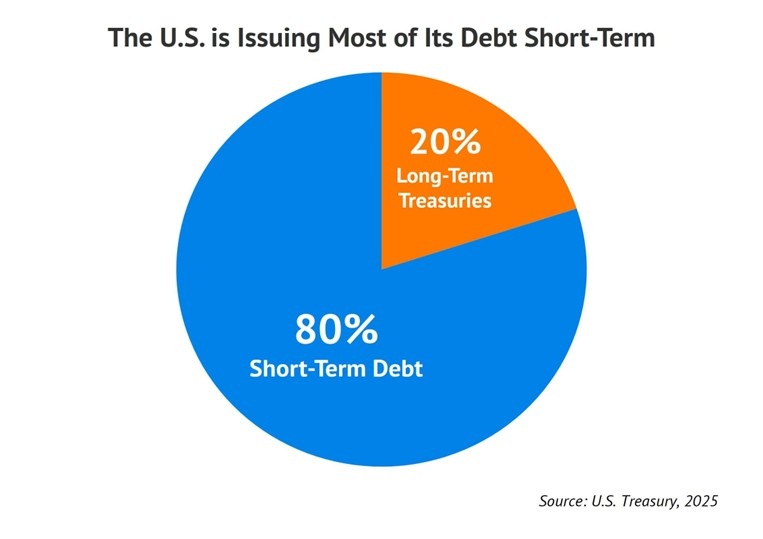

The bond market specifically demands higher yields at the long-end of the bond curve, bonds that mature 10 or more years ahead. Traditionally the majority of US marketable debt (85%+) has consisted of these longer-dated bonds, which are purchased by pension funds and sovereigns.

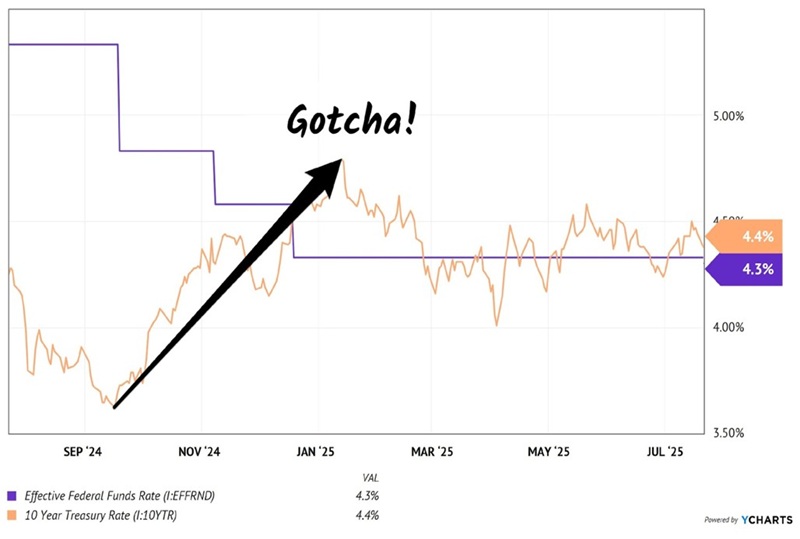

Yet here we are today with the 10-year Treasury yielding just 4.3%. Yes, borrowers are lending to Uncle Sam and asking for a mere 4.3% per year over the next 10 years. In a perfectly free market this yield would likely be 5% or more but policymaker “wizardry” has secured a borrowing discount for ol’ Sam.

(Remember, bonds are loans from the buyer to the issuer. When the Treasury issues bonds, it’s essentially Uncle Sam asking for loans. No one is obligated to make these loans, however! So, Ol’ Sam has no choice but to pay whatever yield the market demands. Which is why the market has been, ahem, massaged in recent years.)

Who is the man behind the curtain pulling these strings? Currently it’s Treasury Secretary Scott Bessent, who took over the controls from predecessor Janet Yellen.

Yellen subtly influenced the bond market by issuing primarily short-term debt rather than long-dated Treasuries. This reduced long-term bond supply and suppressed long-term yields (demand exceeds supply and the issuer—the US government—can offer lower yields). I called this “Quiet QE” because it was not widely reported but it likely held long yields 0.5% lower than they would have been otherwise.

By 2024, Yellen had funded a whopping 75% of the deficit at the short end of the curve—up from just 15% five years earlier. Current Secretary Bessent publicly criticized this tactic but quietly continued it (“watch what I do, not what I say”), but at an astonishing 80% versus Yellen’s 75%!

This stealthy switch to short-term debt puts a ceiling on long-term yields. Bessent clearly won’t tolerate a higher 10-year yield because it inflates interest payments on federal debt. He wants long-term rates capped, providing a sturdy floor beneath the bond market—and he’s doing it by limiting the supply of long-dated bonds. (Aside: mortgage rates follow the 10-year, and this administration will do anything to lower those!)

This stealthy switch to short-term debt puts a ceiling on long-term yields. Bessent clearly won’t tolerate a higher 10-year yield because it inflates interest payments on federal debt. He wants long-term rates capped, providing a sturdy floor beneath the bond market—and he’s doing it by limiting the supply of long-dated bonds. (Aside: mortgage rates follow the 10-year, and this administration will do anything to lower those!)

Bessent’s sleight of hand makes Treasury bond funds like the iShares 20+ Year Treasury Bond ETF (TLT) attractive. TLT currently yields 4.6%. Not bad.

TLT should hold its yield when the Federal Reserve eases. The Fed lowering rates will reduce yields on money market funds and short-term bonds instantly, but the “long end” of the curve won’t be directly affected.

So, vanilla investors assume that long-term yields will drop as the Fed lowers. We say, “not necessarily.”

When the Fed began cutting rates last September, it ironically sparked a serious rally in long yields! The 10-year rate soared from 3.6% to 4.8% within three months. That was a 33% move!

The Fed Cut, But Long Rates… Spiked?!

Long rates rose because inflation expectations increased. Bond buyers worried that Powell was cutting too fast, too soon. Investors bid up the yields on long bonds (which are more sensitive to inflation because of their length).

Long rates rose because inflation expectations increased. Bond buyers worried that Powell was cutting too fast, too soon. Investors bid up the yields on long bonds (which are more sensitive to inflation because of their length).

I don’t anticipate a long rate move as extreme this time around. But it is possible that long rates will slowly grind higher as the Fed lowers. Which will weigh on long-dated bond prices and funds such as TLT.

For a 4.6% yield we’re going to “pass” on TLT itself. Even a 1% or 2% price decline will crimp our returns. Given our “retire on dividends” mandate of 8% returns per year or better, we need some upside from here.

Or we can boost TLT’s yield to a terrific 12.2% and call it a day! And we can do this without having to fiddle with options such as selling puts or writing covered calls.

A newer ETF does this all for us.

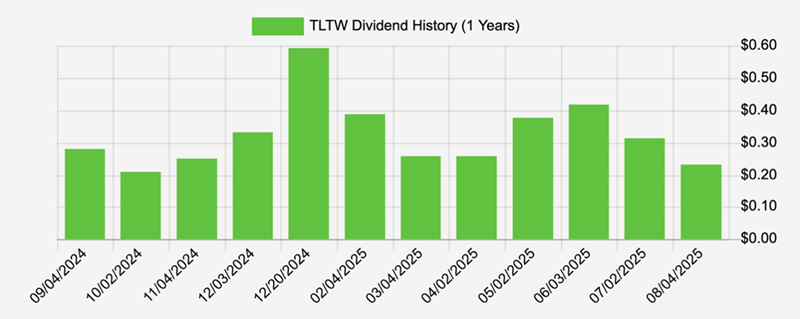

iShares 20+ Year Treasury Bond BuyWrite Strategy ETF (TLTW) buys TLT and then enhances returns by selling covered calls. It generates a terrific 12.2% yield via a dividend that is paid monthly:

TLTW Pays a Big Monthly Dividend

Plunk $100,000 into TLT today and we clear $4,600 per year. Shift it into TLTW and that income vaults to $12,200.

Plunk $100,000 into TLT today and we clear $4,600 per year. Shift it into TLTW and that income vaults to $12,200.

TLTW holds 100% TLT shares and sells monthly covered call options. TLTW pockets the options income, plus a bit of potential appreciation (up to 2% per month) if TLT rallies.

The result? A dynamic monthly dividend currently annualizing to a terrific 12.2%.

Next time you see suits on TV hyperventilating about bonds, just sit back and smile. Their persistent worries only pump up TLTW’s premium income!

— Brett Owens

Sponsored Link: Whether you believe in Treasuries or want to stick with more traditional 8%+ monthly payers, the strategy is the same—let your portfolio replace your paycheck and cover your monthly bills.

Contrary to vanilla Wall Street opinion, it is possible to find elite 8% payouts that are delivered monthly. Here are my favorite 8%+ monthly payers for retiring on dividends.

Source: Contrarian Outlook