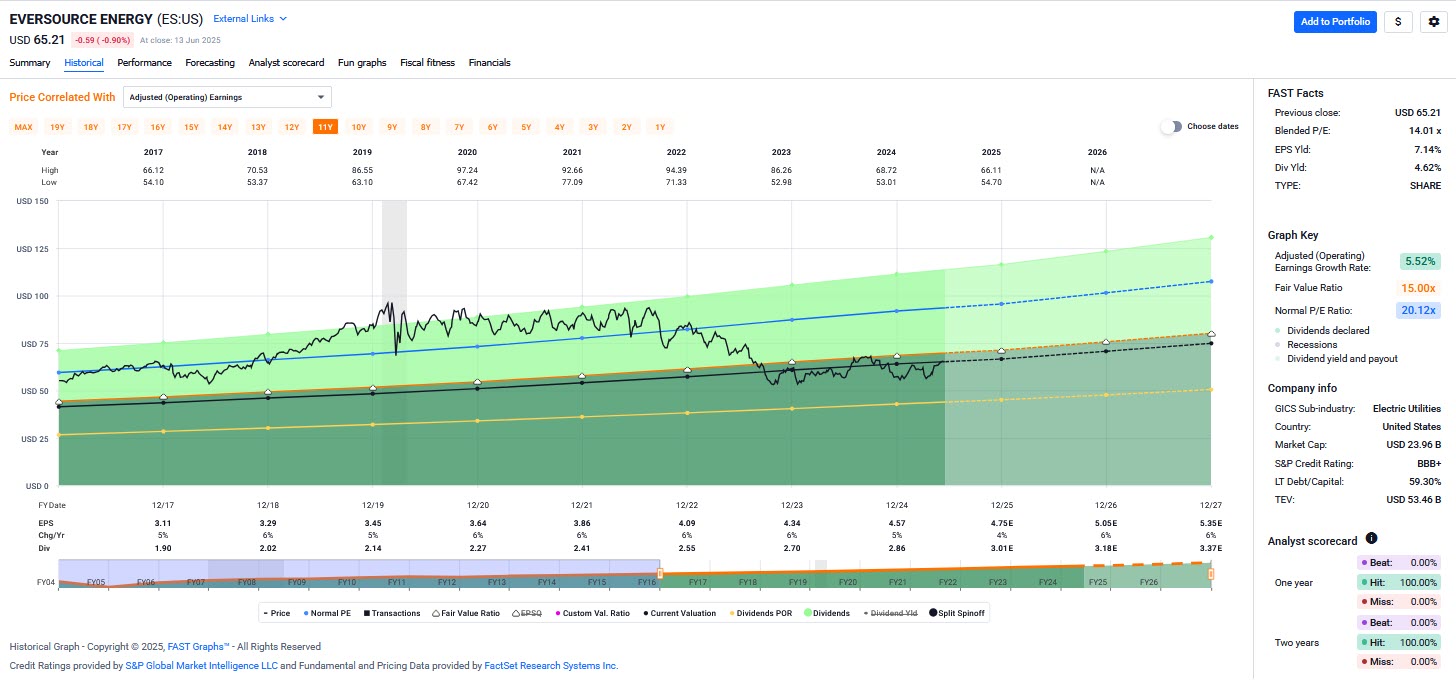

Income and Total Return

In this video, Chuck Carnevale, co-founder of FAST Graphs, aka Mr. Valuation analyzes Eversource Energy (ES), for Income and Total Return, a New England-based utility known for its consistent earnings and dividend growth. With a dividend increasing at nearly 8% annually and a current yield of 4.6%, the stock offers strong income potential. Historically valued at premium P/E ratios (~18), Eversource now trades at a lower P/E (~14), presenting a rare value opportunity.

Despite some temporary earnings pressure from investments in renewable energy and high capital expenditures, core fundamentals remain strong. The company has delivered steady 5–6% earnings growth since 2006, with forecasts expecting more of the same. Its analyst scorecard shows 100% accuracy on 1- and 2-year estimates, reinforcing its predictability.

Despite some temporary earnings pressure from investments in renewable energy and high capital expenditures, core fundamentals remain strong. The company has delivered steady 5–6% earnings growth since 2006, with forecasts expecting more of the same. Its analyst scorecard shows 100% accuracy on 1- and 2-year estimates, reinforcing its predictability.

While return on equity temporarily turned negative in 2023 due to one-time charges, cash flow remains healthy and covers dividends comfortably. If the stock returns to fair value or regains its premium valuation, investors could see total returns of 12–25% annually over the next few years. Chuck positions Eversource as a high-quality, income-focused investment with upside potential, especially appealing for long-term, conservative investors.

— Chuck Carnevale

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: FAST Graphs

Disclosure: Long ES