Okta (OKTA) [was] under heavy selling pressure [Wednesday]—down more than 12%—despite delivering a solid Q1 beat. [The] move is clearly a reaction to overly bullish sentiment ahead of the company’s report. But for long-term investors, this may shape up to be a well-timed “buy the dip” opportunity. Here’s why.

Okta is a pure play in the software security space, with a focus on identity and access management, one of the most critical layers of cybersecurity today. Its cloud platform helps businesses control who gets access to what, whether it’s employees logging into internal systems or customers accessing apps. The company’s core strengths lie in Single Sign-On (SSO), Multi-Factor Authentication (MFA), and Zero Trust security.

Consider it the digital gatekeeper for a growing number of companies—making Okta essential to the internet infrastructure stack.

Okta’s Earnings Results Hit the Mark

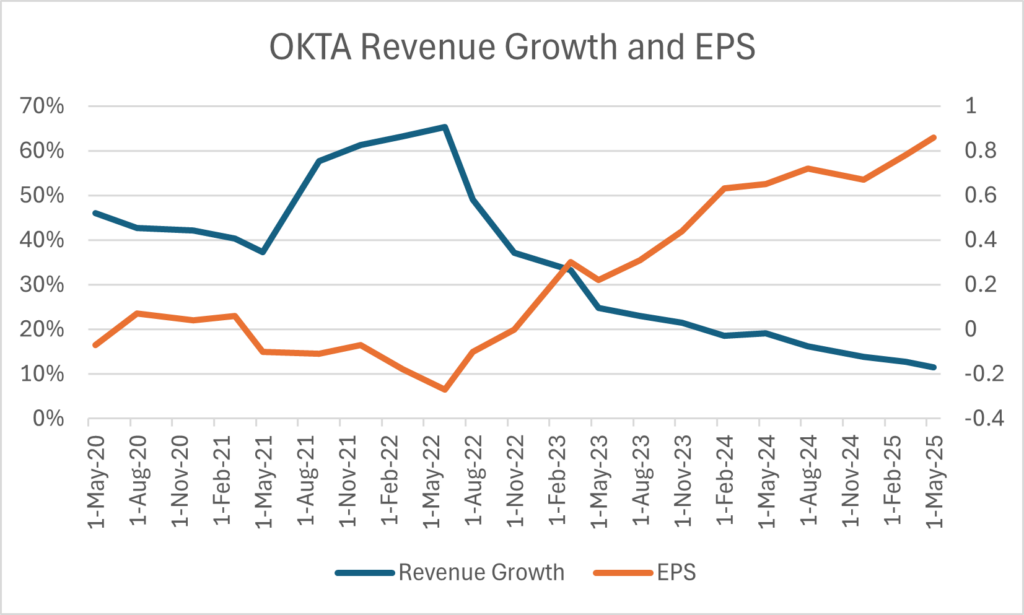

Revenue for the quarter came in at $688 million, up 11.5% year-over-year and ahead of expectations. While growth is slowing, earnings per share beat by $0.09, continuing a two-year trend of consistent outperformance versus Wall Street targets.

The source of [yesterday’s] 15% drop? Guidance.

The source of [yesterday’s] 15% drop? Guidance.

Despite not seeing any macro weakness in Q1, management commented it had heard enough feedback – from customer conversations, sales teams, and headlines – to warrant a more cautious tone for the next quarter.

In short, Okta is guiding conservatively because the tone of the market feels different, not because the company’s numbers are breaking. The choice not to raise guidance has sparked a short-term pullback that should be met with technical support.

Pre-Earnings Rally Set Okta Up for a Correction

Okta was added to the S&P MidCap 400 in late April, triggering a fast 20%+ rally in under a month as institutions repositioned to match the index rebalance. That move pushed shares to their highest level in over two years.

In hindsight, it looks like a classic “buy the rumor” rally heading into earnings, and now we’re seeing the “sell the news” phase unfold.

Wall Street Sentiment Still Supports a Bottom

58% of analysts currently rate Okta a “Buy,” with 40% at “Hold.” This tells us the stock isn’t overcrowded like NVIDIA and other stretched large-cap tech names. With [yesterday’s] sharp drop, expect to see bullish upgrades as firms reposition this selloff as a buying opportunity.

Technicals in Play for Support

Technicals in Play for Support

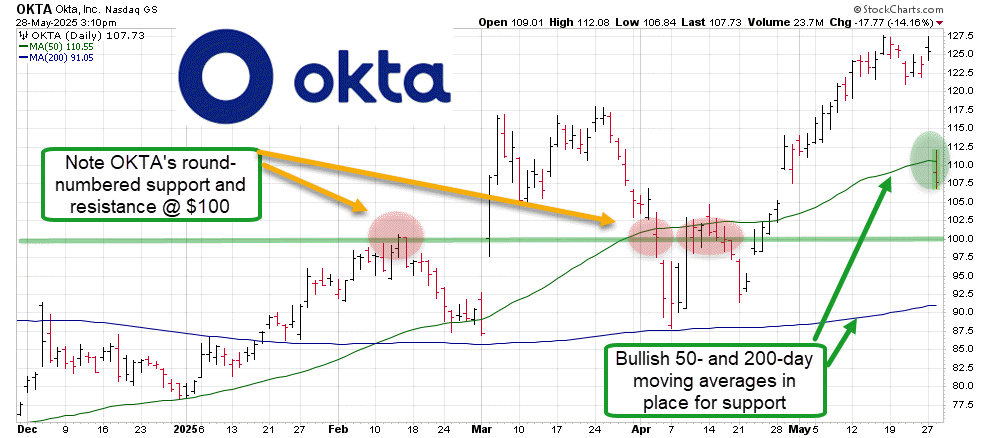

Okta is emerging from a volatility-charged two-month stretch with key trendline support still intact.

The stock’s 50-day moving average has been in a bullish trend since November 2024, putting Okta in an elite group of stocks that avoided a breakdown during the March and April correction. Its 200-day moving average is also trending higher, reinforcing the bullish case.

Both trendlines are now positioned to provide support if [yesterday’s] selling continues. Key levels to watch: $110 (broken [Wednesday]), $100 psychological support, and $90 in the case of a deeper decline.

Bottom Line

Okta’s Q1 wasn’t bad—but after a sharp run-up, the expectations bar was high. The lack of a guidance raise and signs of slowing growth triggered a reset that should be taken in stride. With shares still up 36% year-to-date and key technical levels in place, this looks like a sentiment-driven shakeout, not a fundamental breakdown.

OKTA’s Long-term outlook remains bullish with a price target of $150.

— Chris Johnson

Karim Rahemtulla, the trader behind a 400% gain in 24-months on Rolls-Royce, has uncovered another potential multi-bagger. This under-$20 stock gives you exposure to over 1-oz of gold with the lowest production costs in the industry. And an upcoming announcement could send this stock soaring. Get Karim's urgent briefing - click here now.

Source: Money Morning