The late, great Charlie Munger gave the world countless pieces of timeless advice.

I think his greatest “mental model” was inversion.

Basically, if you’re looking for a favorable outcome, simply doing what’s necessary to avoid the bad outcomes is a fine way to solve for the result you’re looking for.

Inversion can be applied to almost anything in life.

Inversion can be applied to almost anything in life.

But it is an especially powerful trick when it comes to investing.

There are all kinds of ways to invest.

But being a successful investor can be as easy as not being a terrible investor.

And being a terrible investor would involve things like investing in bad businesses, use of too much leverage, trying to time the market, paying too much for stock, paying high fees, not staying patient, avoiding fundamental analysis of what you’re investing in, etc.

When I think of the inverse of all of this, my mind goes right to dividend growth investing.

This is a long-term investment strategy that tends to almost automatically avoid bad businesses and bad outcomes, as the strategy limits one to only those businesses which are able to pay and sustain safe, growing dividends to shareholders.

Growing dividends can only be sustained when there’s underlying growing profit, and growing profit can only be sustained when you’re running a great business.

To see what I mean, take a look at the Dividend Champions, Contenders, and Challengers list.

This list has data on hundreds of US-listed stocks that have raised dividends each year for at least the last five consecutive years.

You’d be hard-pressed to find any terrible businesses on this list; to the contrary, this list contains some of the world’s best-known businesses.

This inversion (i.e,, avoiding terrible businesses) via dividend growth investing has helped me to build the FIRE Fund.

That’s my real-money portfolio, and it generates enough five-figure passive dividend income for me to live off of.

I’ve actually been able to live off of dividends since I retired in my early 30s.

My Early Retirement Blueprint explains how that was accomplished.

My Early Retirement Blueprint explains how that was accomplished.

Of course, another aspect of avoiding bad investment outcomes is avoiding overpaying.

And that comes down to valuation at the time of investment.

Whereas price represents what you pay, value represents what you get.

An undervalued dividend growth stock should provide a higher yield, greater long-term total return potential, and reduced risk.

This is relative to what the same stock might otherwise provide if it were fairly valued or overvalued.

Price and yield are inversely correlated. All else equal, a lower price will result in a higher yield.

That higher yield correlates to greater long-term total return potential.

This is because total return is simply the total income earned from an investment – capital gain plus investment income – over a period of time.

Prospective investment income is boosted by the higher yield.

But capital gain is also given a possible boost via the “upside” between a lower price paid and higher estimated intrinsic value.

And that’s on top of whatever capital gain would ordinarily come about as a quality company naturally becomes worth more over time.

These dynamics should reduce risk.

These dynamics should reduce risk.

Undervaluation introduces a margin of safety.

This is a “buffer” that protects the investor against unforeseen issues that could detrimentally lessen a company’s fair value.

It’s protection against the possible downside.

Buying undervalued high-quality dividend growth stocks is a great way to heed Charlie Munger’s advice and build significant wealth, passive dividend income, and freedom along the way.

The preceding passage is really only useful if one already understand how valuation works.

If you need some help here, no worries.

Fellow contributor Dave Van Knapp’s Lesson 11: Valuation, which is part of an overarching series of “lessons” designed to teach dividend growth investing, articulates the ins and outs of valuation using simple terminology and even provides an easy-to-use valuation template.

With all of this in mind, let’s take a look at a high-quality dividend growth stock that appears to be undervalued right now…

Toll Brothers Inc. (TOL)

Toll Brothers Inc. (TOL)

Toll Brothers Inc. (TOL) is an American luxury homebuilder.

Founded in 1967, Toll Brothers is now a $9 billion (by market cap) homebuilding giant that employs approximately 5,000 people.

The company’s footprint extends across 24 states, primarily along both US coasts and the US Sun Belt.

Toll Brothers is the leading builder of luxury homes in the US, catering to affluent customers, including move-up buyers, empty nesters, and second-homebuyers.

Its name is synonymous with luxury living.

For perspective on the affluence of its client base, the company’s most recent quarter (Q1 FY 2025) revealed that Toll Brothers delivered just under 2,000 homes at an average price of approximately $925,000.

This is an important distinction.

Because these are not entry-level homes targeted to price-sensitive buyers, Toll Brothers is somewhat insulated from the vagaries of the economy.

Toll Brothers has a client base which skews wealthy, meaning the company as a whole is not as economically sensitive as some of the other American homebuilders.

Moreover, these homes are luxurious and desirable.

When affluent customers desire what you’re selling and have both the willingness and wherewithal to purchase it, this creates a smoother business model (relative to homebuilders which may be more exposed to the cycles) with more visibility and resilience.

In addition, there’s a massive and well-known housing shortage in the US, where supply is woefully short of meeting demand.

The US is short millions of homes, so it’s not like buyers have a plethora of choices.

Further fortifying Toll Brothers is its strategic risk management, whereby it purchases and controls land in prime locations and starts construction after sales agreements are already executed.

This is a well-run company with a favorable supply-demand backdrop and an affluent customer base.

It also has a sizable backlog (now standing at almost $7 billion, which is nearing the company’s entire market cap) to work through.

It is strength after strength.

It’s hard to find any area of weakness, which is why Toll Brothers should be able to continually grow its revenue, profit, and dividend over the coming years.

Dividend Growth, Growth Rate, Payout Ratio and Yield

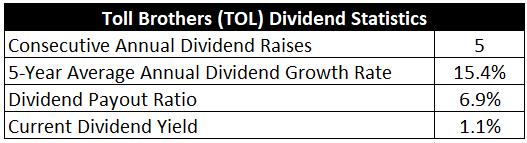

Already, Toll Brothers has increased its dividend for five consecutive years.

A short track record, sure, but the five-year dividend growth rate of 15.4% shows what a start the company is off to.

Plus, with a payout ratio of only 6.9%, which is one of the lowest I’ve come across, along with the fast business growth (which I’ll delve into soon), Toll Brothers is easily capable of continuing its double-digit dividend growth ways.

I think the fact that the payout ratio is below 10%, despite growing the dividend at 15%+ year, gives one an early indication of just how fast the business is growing.

And it also shows how much of a dividend growth runway is still out in front of us.

And it also shows how much of a dividend growth runway is still out in front of us.

However, there is one big-trade off here: yield.

Yielding only 1.1%, the stock is clearly not suitable to those who are looking for current income right now.

That said, this yield is 10 basis points higher than its own five-year average, so there’s a bit more income juice to squeeze here than usual (albeit with the caveat that the five-year average is limited in its usefulness by the short dividend growth history).

Again, this lowish yield will not entice income investors.

On the other hand, for those with a long-term time horizon seeking a high-quality compounder, this idea could make a lot of sense.

Revenue and Earnings Growth

As much sense at it may make, though, one has to remember that these dividend metrics are mostly based on what’s happened over the past.

However, investors must always be looking toward the future, as today’s capital gets put on the line and risked for tomorrow’s rewards.

As such, I’ll now build out a forward-looking growth trajectory for the business, which will come in handy during the valuation process.

I’ll first show you what the business has done over the last decade in terms of its top-line and bottom-line growth.

I’ll then reveal a professional prognostication for near-term profit growth.

Amalgamating the proven past with a future forecast in this manner should give us what we need to estimate where the business might be going from here.

Toll Brothers increased its revenue from $4.2 billion in FY 2015 to $10.8 billion in FY 2024.

That’s a compound annual growth rate of 11.1%.

Strong top-line growth.

I’m usually looking for a mid-single-digit (or better) top-line growth rate out of a mature company like this, and I think the double-digit result here underscores the kind of growth US homebuilders are capable of in this environment.

Meanwhile, earnings per share grew from $1.97 to $15.01 over this period, which is a CAGR of 25.3%.

Phenomenal stuff.

I’d expect to see 25%+ EPS growth out of a tech company, not a homebuilder.

But that’s the world we’re living in.

Besides the favorable supply-demand backdrop, which has served to boost profitability over this period, share buybacks have been a big part of the excess bottom-line growth story.

Toll Brothers reduced its outstanding share count by 43% over the last decade, which is a material float reduction.

Looking forward, CFRA believes that Toll Brothers will compound its EPS at an annual rate of 8% over the next three years.

While 8% bottom-line growth would still represent a pretty picture – a lot of companies out there would love to post 8% EPS growth – this would be a steep drop from what Toll Brothers did over the last decade.

If CFRA’s forecast is anywhere near accurate, we’re looking at a bottom-line growth rate that’s only 1/3 of what transpired over the last 10 years.

What gives?

Well, it’s a combination of factors conspiring to slow homebuilders.

We have higher interest rates putting downward pressure on home/mortgage demand, labor shortages, high home prices, broad economic uncertainty, and recent equity market weakness which can impact affluent homebuyers relying on equity wealth to purchase high-end homes.

However, Toll Brothers does have a number of shields protecting the business.

Because it doesn’t cater to entry-level homebuyers, higher rates don’t impact Toll Brothers quite as hard/directly as some of the other US homebuilders.

That’s because a large cohort of its buyers purchase homes via all-cash deals.

In addition, the company has a sizable backlog to work through while it navigates economic uncertainty.

CFRA touches on some of this: “[Toll Brothers]’s target demographic of affluent buyers positions [Toll Brothers] to deliver on its 2025 guidance. While the broader housing market faces headwinds from high interest rates, [Toll Brothers]’s wealthy customer base (evidenced by 26% all-cash purchases and 68% average LTVs) provides some insulation from rate sensitivity. The current environment presents a nuanced picture, with robust demand in luxury and move-up segments (70% of business) counterbalanced by affordability pressures in entry-level luxury (25-30%).”

I think that sums it up quite well.

While it seems unlikely that Toll Brothers will put up anywhere near 25%+ EPS growth over the next few years (those days are probably gone, at least for now), I don’t see 8% EPS growth as a bad outcome at all.

By virtue of the payout ratio being so low, that would still allow Toll Brothers to grow its dividend at a low-double-digit rate over the next few years or so, with some possible acceleration back into a mid-teens rate once things normalize.

Even during an unusually tough stretch for the company, the dividend was raised by 8.7% just last month, which is emblematic of what I’m laying out here.

I think that’s about as bad as it gets for this name; yet, that would be a welcome dividend raise by shareholders of most other companies out there.

Said another way, a bad day for Toll Brothers is probably a pretty good day for a lot of other companies.

As long as one doesn’t hold this investment to a totally different standard and come in with unrealistic expectations, shareholders willing to hold for the long term and let Toll Brothers do its magic over time should be handsomely rewarded.

Moving over to the balance sheet, the company has a solid financial position.

Financial Position

The long-term debt/equity ratio is 0.4.

Net long-term debt of ~$1.5 billion is not egregious for a company of this size.

The company also commands investment-grade credit ratings: BBB, Fitch; Baa2, Moody’s; BBB-, S&P.

Although this balance sheet isn’t quite as strong as those I’ve seen among some other homebuilders, Toll Brothers has no financial issues whatsoever.

Profitability is fantastic.

Return on equity has averaged 18.3% over the last five years, while net margin has averaged 11.3%.

Terrific numbers, especially from a capital-intensive homebuilder.

The last few years have been exceptional for Toll Brothers (and homebuilders, in general), so I’d take some of this with a grain of salt.

However, much of this has been building since the bottoming out during the Great Recession – it’s been, essentially, 15 years of steady, incremental improvement culminating in what we see now.

And with the housing supply shortage backdrop still in place, Toll Brothers should continue to generate high returns on capital.

There’s really a lot to like about Toll Brothers – both in terms of the industry and the specific business.

And with economies of scale, brand recognition, market leadership, a built-up land bank in desirable locations, and a large backlog, the company does benefit from durable competitive advantages.

Of course, there are risks to consider.

Regulation, litigation, and competition are omnipresent risks in every industry.

The industry is extremely competitive, but Toll Brothers lacks a direct competitor in the luxury space.

The very business model is a risk unto itself: This is a capital-intensive, asset-heavy business model exposed to the cycles, although its market positioning and clientele insulates it somewhat.

Labor shortages in construction have been an issue.

There is exposure to interest rates, and the current situation involving elevated rates is a headwind.

Although its client base skews wealthy and often purchases homes with cash, pervasive weakness in the economy and/or financial markets would almost certainly impact Toll Brothers.

Home prices are currently high, curbing demand; lower prices would stoke demand, but this would open up resales and hurt margins.

Overall, I think the risk profile is very acceptable, particularly when weighed against the quality of the franchise.

The valuation, which is extremely undemanding, also has to be weighed…

Valuation

The stock is available for a lowly P/E ratio of only 6.5.

I get that Toll Brothers isn’t putting up the blistering growth of yesteryear, and I understand that rate and prices are high, but there’s an awful lot of negativity and pessimism being priced in at these levels.

The PEG ratio is well below 1.

Now, to be fair, this stock is almost always valued lowly (due to concerns such as capital intensity).

However, this is unusually low, and we are way off of the stock’s own five-year average P/E ratio of 8.

The P/CF ratio of 5.7, which is absurdly low, is also lower than its own five-year average of 6.7.

And the yield, as noted earlier, is slightly higher than its own recent historical average.

So the stock looks cheap when looking at basic valuation metrics. But how cheap might it be? What would a rational estimate of intrinsic value look like?

I valued shares using a two-stage dividend discount model analysis.

I factored in a 10% discount rate, a 10-year dividend growth rate of 15%, and a long-term dividend growth rate of 8%.

I’m basically extrapolating the demonstrated dividend growth over the last five years into the next decade.

While I acknowledge that the next year or two could result in below-trend dividend growth, the extremely low payout ratio and high growth rate of the business itself portends a continuation of the mid-teens dividend growth that shareholders have become accustomed to.

I see a temporary deceleration followed by a nice acceleration thereafter and well out into the years ahead.

The payout ratio is too low, and the business is too good, to expect anything less than strong dividend raises over the next decade or so.

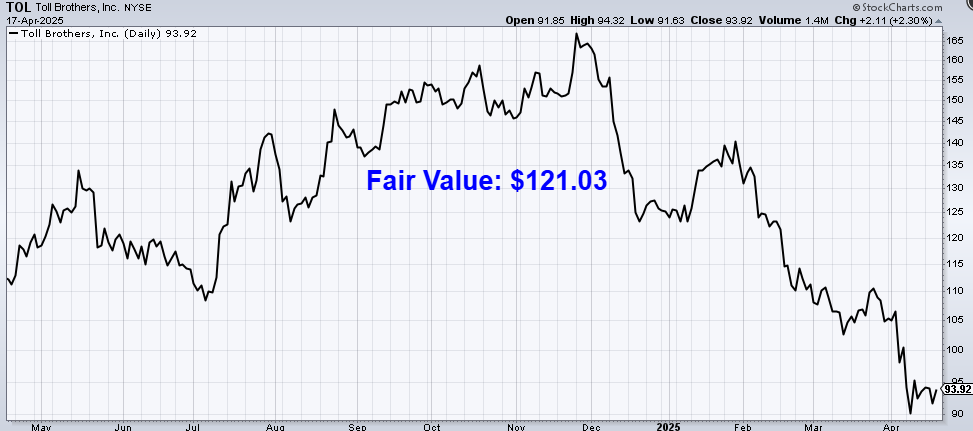

The DDM analysis gives me a fair value of $97.10.

The reason I use a dividend discount model analysis is because a business is ultimately equal to the sum of all the future cash flow it can provide.

The DDM analysis is a tailored version of the discounted cash flow model analysis, as it simply substitutes dividends and dividend growth for cash flow and growth.

It then discounts those future dividends back to the present day, to account for the time value of money since a dollar tomorrow is not worth the same amount as a dollar today.

I find it to be a fairly accurate way to value dividend growth stocks.

My model shows a stock that looks modestly undervalued.

But we’ll now compare that valuation with where two professional stock analysis firms have come out at.

This adds balance, depth, and perspective to our conclusion.

Morningstar, a leading and well-respected stock analysis firm, rates stocks on a 5-star system.

1 star would mean a stock is substantially overvalued; 5 stars would mean a stock is substantially undervalued. 3 stars would indicate roughly fair value.

Morningstar rates TOL as a 4-star stock, with a fair value estimate of $140.00.

CFRA is another professional analysis firm, and I like to compare my valuation opinion to theirs to see if I’m out of line.

They similarly rate stocks on a 1-5 star scale, with 1 star meaning a stock is a strong sell and 5 stars meaning a stock is a strong buy. 3 stars is a hold.

CFRA rates TOL 3-star “HOLD”, with a 12-month target price of $126.00.

I don’t think my model was overly cautious, but I still came out very light in comparison to these two firms. Averaging the three numbers out gives us a final valuation of $121.03, which would indicate the stock is possibly 22% undervalued.

Bottom line: Toll Brothers Inc. (TOL) is a high-quality company with market leadership, brand recognition, and a wealthy clientele that insulates the firm from many of the industry’s challenges. Its name is synonymous with luxury living, and its huge backlog offers excellent revenue visibility. With a market-like yield, double-digit dividend growth, an extremely low payout ratio, five consecutive years of dividend increases, and the potential that shares are 22% undervalued, this prime homebuilder with low multiples is an excellent long-term investment candidate for dividend growth investors.

Bottom line: Toll Brothers Inc. (TOL) is a high-quality company with market leadership, brand recognition, and a wealthy clientele that insulates the firm from many of the industry’s challenges. Its name is synonymous with luxury living, and its huge backlog offers excellent revenue visibility. With a market-like yield, double-digit dividend growth, an extremely low payout ratio, five consecutive years of dividend increases, and the potential that shares are 22% undervalued, this prime homebuilder with low multiples is an excellent long-term investment candidate for dividend growth investors.

-Jason Fieber

Note from D&I: How safe is TOL’s dividend? We ran the stock through Simply Safe Dividends, and as we go to press, its Dividend Safety Score is 70. Dividend Safety Scores range from 0 to 100. A score of 50 is average, 75 or higher is excellent, and 25 or lower is weak. With this in mind, TOL’s dividend appears Safe with an unlikely risk of being cut. Learn more about Dividend Safety Scores here.

P.S. If you’d like access to my entire six-figure dividend growth stock portfolio, as well as stock trades I make with my own money, I’ve made all of that available exclusively through Patreon.

Source: Dividends & Income

Disclosure: I have no position in TOL.