UnitedHealth Group (NYSE:UNH) is one of the most insulated companies from tariffs and perhaps even a recession. It is a behemoth in the healthcare sector and derives the vast majority of its revenue from U.S. healthcare services. The company has little to lose from a trade war, and even if the pharmaceutical industry hikes prices, it can easily pass those on to its customers.

Analysts project consistent growth going forward and this growth is unlikely to be knocked down even if a recession hits or tariffs stick around. As a result, the stock has performed remarkably well compared to the rest of the market.

Why UnitedHealth Is “Tariff-Proof”

Why UnitedHealth Is “Tariff-Proof”

This company has deeply entrenched domestic operations with a healthcare-focused business model. Healthcare companies have been booming, and especially so in the post-COVID era. Demographic changes are expected to keep driving growth here, and AI could supercharge that if they start meaningfully accelerating innovation for biotech companies. It also has a recession arm that provides consistent recurring revenue, so it is both tariff-proof and recession-proof.

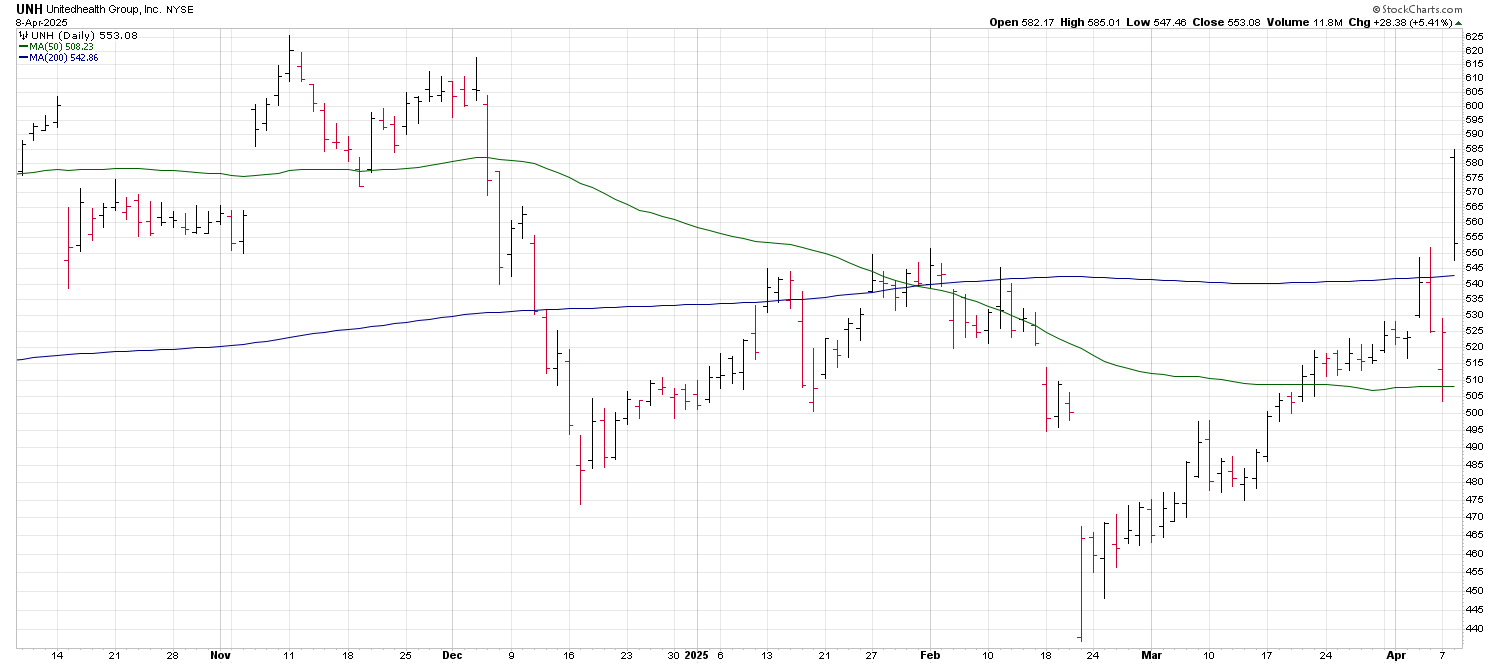

The broader market has plunged this year and both the Nasdaq and the Russell 2000 have entered bear market levels. The S&P 500 could be following suit due to the trade war accelerating. On the other hand, UNH stock is up by over 15% in the past month.

This is not only because the business itself is booming but because investors are starting to see UNH stock as the linchpin of any tariff-proof portfolio. Hedge funds are piling into defensive stocks and are offloading growth stocks, and while retail investors have been buying the dip, if tariffs keep sticking around, they too will be forced to sell and move into stocks like UNH.

Plus, it also has a 1.6% dividend yield you can sit on as the broader market stabilizes.

Is UNH Stock a Buy Now?

You should consider having at least some exposure to UNH stock. You’re paying nearly 36 times earnings due to investors piling into defensive stocks, but the stock is worth the premium due to the safety it provides in the current environment. Almost every major company has huge exposure to international markets and foreign inputs. UnitedHealth does have some exposure to the latter, but it is a healthcare company and will have little impact on margins or revenue.

Analysts expect solid EPS growth over the coming years. EPS is expected to grow to nearly $30 this year and double in around 5-6 years. Revenue is also expected to grow 13% this year to $452 billion and keep growing around 7-10% annually on average in the coming years.

Moreover, the average price target of $635 implies a solid upside from the current price of $553. I’d rate UNH a “Buy” in the current environment.

— Omor Ibne Ehsan

To carry out Trump's Executive Order #14196 initiative, the administration will have to partner with a handful of U.S. companies that control the "reserve accounts" sitting on trillions of dollars' worth of untapped natural resources. I've spent months digging into this – and I've identified three companies that have already been granted "emergency status" and fast-track approvals. I believe their shares could skyrocket once new capital starts moving into the sector. See the three stocks that I expect to be the biggest winners as this plan rolls.

Source: Money Morning