This Week’s Outlook Summary

I was reminded of the old Kenny Rogers song, “The Gambler” last night as I started putting this week’s notes together. You know the line “You’ve got to know when to hold them… know when to fold them”

When I read that, I think about the hedged positions that you and I have been talking about for the last four weeks. You’re feeling pretty good right now if you followed those strategies like I did, but you’re asking yourself “should I close my shorts?”. The answer is “no”, it’s time to hold them.

We’re seeing a lot of volatility Monday morning as the Trump Administration is playing cat and mouse with its international trading partners.

Will there be a 90-day suspension of the tariffs to allow negotiations? We all heard the President’s Cabinet and other staff emphatically say that the tariffs were not a negotiating tool, so “no” again.

Even if the tariffs were suspended, there are three things that are going to be reported on Thursday and Friday could do just as much damage as the tariffs in the market’s current condition.

No, this is a time to hold the course while the rest of the investors that have been stunned by the market moves come out of their state of shock only to start realizing that yeah, its time to sell.

It all starts with investors’ sentiment, which is far from its bottom.

Investor Sentiment is Bad, But Not Bad Enough

You read that correctly. For as much red it felt like we saw running in the streets last week, it wasn’t enough.

I mean, I think that you get it, because you’re hear with me, but most investors just don’t not yet.

Over the weekend I saw headlines on several financial websites with the term “buy the dip” blazoned across the top. Let me just tell you that this is not the market to buy the dip in until you set some sensible targets.

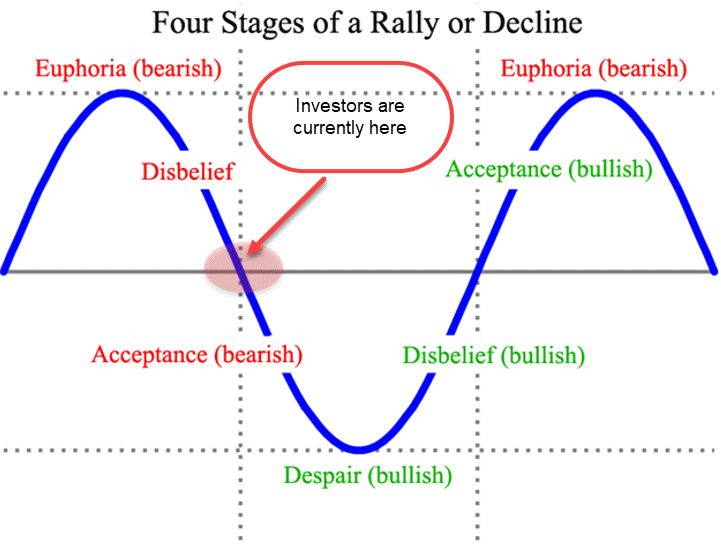

Let’s look at one of my favorite charts. This is one of those charts that you only understand when the market is doing what it has been for the last two months.

This is the Four Stages of a Market Cycle. The market moves through all four of these cycles as it moves from a bull market to bear market and then back again.

Investors came out of the elections in a strong buying mood as the market’s major indices traded to new all-time highs in December. Sentiment was optimistic, no… euphoric, as we looked forward to another bullish year in 2025. Then something happened.

Investors came out of the elections in a strong buying mood as the market’s major indices traded to new all-time highs in December. Sentiment was optimistic, no… euphoric, as we looked forward to another bullish year in 2025. Then something happened.

The Trump administration’s plans for tariffs began to move from idea to policy as Canada and Mexico were hit with early tariffs. The administration worked to delay and possibly reduce the tariffs, but a trade war was already brewing.

This is why sentiment matters.

Investors had been so focused on how well they expected their investments to do that they ignored warnings that had been in the market for weeks and even months.

Warren Buffett moving to cash, CEOs and other insiders selling shares and other signs that those in the know were preparing for something big.

Two months later investors found themselves dealing with another bout with inflation, trade wars and the growing possibility that the economy is set to move into a recession.

While all of that has reduced the optimism held by retail investors, we’re just not there yet.

[As of] Monday morning, we’re seeing investors that have been fast to start buying stocks as soon as the headlines crossed that the White House was talking about potential delays to the tariffs to allow countries to negotiate.

We’ve been through that before, remember? Just over a month ago the game was the same with Mexico and Canada, nothing changed.

The fact that investors sentiment is not reflecting a “blood in the street” situation is not surprising. It often takes months for investors to cross into the mindset that they feel absolute despair towards the market, which is the time that wise investors will be backing the truck up to buy stocks at deep discount prices.

So, here’s where we stand on sentiment.

Readings of the CBOE Volatility Index (VIX) and other short-term sentiment gauges have given us short-term “signals” that fear has reached extreme levels. [Monday] morning, The VIX tapped highs at 60. In a normal market, this would be an incredibly strong buying signal, this market is nothing like a normal market.

We’re currently moving into the “Acceptance” phase of the market’s correction cycle pictured above. This means that investors are starting to accept the fact that stocks aren’t likely to produce losses over the next 6-12 months. This means that we’ll see more selling.

Who’s doing the selling now?

First in line are the investors that are now receiving their quarterly statements that were mailed or emailed last week. The investors that hold 95% of their assets in mutual funds that only check things out when they sit down with their advisors… those are the ones selling. But its only the beginning.

First Quarter Earnings Start this Week

Investors are frightened of the tariffs for a few reasons, one being the effect on corporate earnings.

On Friday, the first of the large banks will open the earnings season with JP Morgan (JPM), Morgan Stanley (MS) and Wells Fargo (WFC) releasing their quarterly results.

There are two huge tests for each company announcing their results this quarter.

- How did the company perform last quarter: Did revenue and earnings beat expectations and by how much, you know, the simple measures.

- The second test is much more important, how will the new tariffs change the company’s outlook?

That second question is going to set the tone for the next three month, regardless of what happens with the tariffs.

Companies were already operating on thinning margins and dropping revenue as consumers have cut spending yet again. Add to that the uncertainties surrounding tariffs and we may end up with a large drop in corporate outlooks for the second quarter and 2026.

This Week’s Economic Data

This sets the stage for a massive announcements on both Wednesday and Friday this week.

- Consumer Price Index: Report after report has shown a leveling or even slight increase in inflationary pressure this month. On Thursday we’ll see the latest inflation report for the month of March. Last month’s CPI was relatively tame, but the Fed’s favorite inflation report (PCE) from just over a week ago showed a slight increase in pricing pressure.

- Producer Price Index: This week’s PPI will probably be more tame than what investors should prepare for next month following the newly added tariffs. That said, any “Upstream” inflation from the PPI report will send the market into another level of defense as economists will warn of heightened inflations/stagflation danger.

- University of Michigan Sentiment survey: The state of the consumers has been quickly eroding as uncertainty over jobs, tariffs and housing continue to sideline consumers. Remembering that the consumer drives more than 70% of the economy is important when this data hits the wire on Friday.

Finally, the Technicals

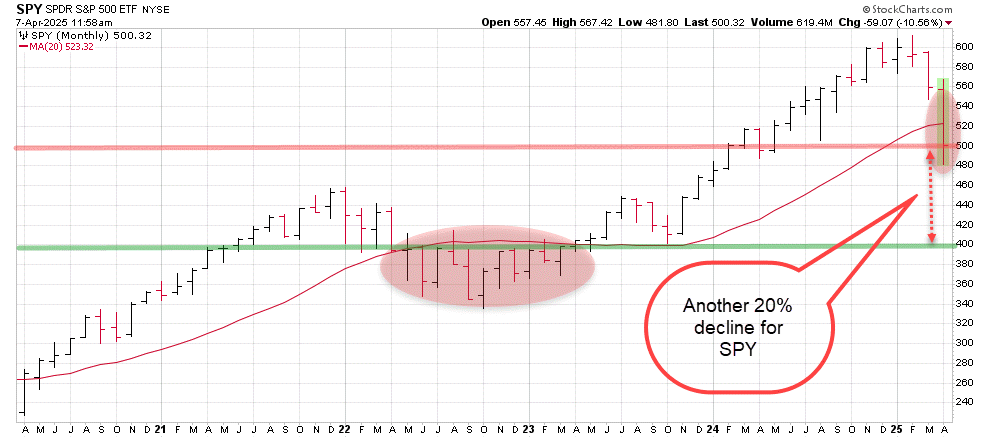

The S&P 500 and Nasdaq 100 start the week below their respective 20-month moving averages. This marks the first time that stocks have traded in a long-term bear market trend since 2022.

There are some silver linings to watch for…

There are some silver linings to watch for…

- Both major indices are trading close or in short-term oversold readings from their RSI. This means that the market is poised for a short-term bounce. It doesn’t mean that we will see one, but conditions do exist.

Any positive headlines on the tariff front are likely to be a catalyst for a fast and aggressive snap higher but be warned that those rallies will be short-lived as investors that haven’t sold stocks yet will use that strength to sell positions that aren’t at their lows. - Those spikes in prices will also give investors another opportunity to add defensive or hedged positions to their portfolios in preparation for even lower prices for stocks.

As it stands this morning, the S&P 500 is trying to maintain pricing above 5,000 – a critical psychological prices for the index – while the Nasdaq 100 (QQQ) is trying to do the same at $400.

Breaks below these large round numbered prices will open each index to further selling pressure. Put simply, the path of resistance is lower by another 10-12% over the next month for each the S&P 500 and Nasdaq 100.

— Chris Johnson

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning